Michelle Cluver

Michelle Cluver2022 is off to a rocky start with inflation, economic growth and the trajectory for higher policy interest rates remaining center stage. Russia’s invasion of Ukraine and Omicron intersecting with China’s zero-COVID policy delayed supply chain normalization while impacting inflation and economic growth expectations. Inflation expectations have kept the Federal Reserve (Fed) center stage as they commenced their interest rate rising cycle in March. Navigating elevated inflation with slowing economic growth is a difficult balancing act for central banks. In line with our outlook from Q4, this also creates a more volatile and selective market.

Fundamentals, quality, and valuations remain key considerations for portfolio positioning. The first half of the year will likely to be volatile as markets navigate commodity and economic growth shocks while simultaneously shifting to a higher yield environment. Portfolios need to balance inflation protection with the prospects of reduced economic growth, creating a framework that balances cyclical and defensive exposures while also having some balance between value and growth.

The unwinding of easy liquidity took some of the air out of both equity and fixed income markets with the S&P 500 Index and Bloomberg U.S. Aggregate Bond Index returning -4.6% and -5.9%, respectively in Q1. For major equity indexes, Q1 2022 was the worst quarter in 2 years. Risk off sentiment boosted the U.S. relative to global markets. The MSCI World ex U.S. returned -4.8%, weighed down by weakness in Europe while the MSCI Emerging Market Index returned -7.0%.

Higher Rates with Slower Growth

Aggressive Rate Rising Cycle Expected in the U.S.

The long-awaited interest rate rising cycle commenced with the Fed increasing interest rates 25 basis points (bps) at their March meeting and signaling further rate rises for 2022 and 2023. Going into 2022, we believed the Fed was likely to be a key source of market volatility as they sought to get ahead of the curve. However, Russia’s invasion of Ukraine made the market more sensitive to economic growth expectations and put the Fed in a challenging position where they’ve needed to increase transparency and reduce the potential for surprises. However, as the initial invasion shock wore off, the language from the Fed became stronger with an increased the focus on regaining control over inflation. This pushed up yield expectations during March. Currently the market has a 69.9% and 64.2% probability of a 50 basis point (bps) interest rate increase at the May and June FOMC meetings, respectively.1 Overall, we expect an aggressive Fed interest rate raising cycle, with policy rates rising to 2-3% by year end.

Expectations for higher policy yields pushed up shorter-term market yields while economic growth concerns kept a lid on longer-term economic growth and yield expectations. During March, the Fed’s real GDP growth projections for 2022 were revised down to 2.8% from December’s expectations of 4.0%, while PCE inflation expectations for the year rose from 2.6% in December to current projections of 4.3%.2 This has increased the short-end of the yield curve, while flattening the middle to longer-end of the curve. The quarter ended with almost no difference between the 10- and 2-year Treasury yield, while inverting slightly after quarter-end.3 10-year Treasury yields rose aggressively in Q1, starting the year at 1.51% while ending the quarter at 2.34%. This increase pales in comparison with the movement in 2-year Treasury yields, which started the year at 0.73% and closed the quarter at 2.33%.4

While economic growth expectations have been revised lower, the U.S. labor market remains strong. Non-farm payrolls increased 431k in March, reducing the unemployment rate from 3.8% to 3.6%. With concerns about inflation and rising wages, increased prime age labor force participation is encouraging. The prime age labor force participation rate increased to 82.5%, only marginally below its pre-pandemic level of 83.0%. This month’s improved participation was driven by a 0.7 ppt increase in the female participation rate. This may indicate reduced COVID risks, rising wages and declining savings are encouraging workers back into the labor force.5 Improved labor supply may help reduce labor shortages and inflation pressures in the U.S.

ECB Remains More Supportive

Higher yields and reduced economic growth expectations are a consideration for central banks globally. With proximity to the Russia-Ukraine conflict and dependence on Russian energy, the European Central Bank (ECB) has certainly been navigating a tightrope between elevated inflation pressures and the potential for pricing pressure to erode economic growth.

At the March 10 meeting, the ECB prioritized fighting inflation, surprising markets by announcing plans to accelerate its exit from extraordinary stimulus even as the war in Ukraine deepened. Markets currently anticipate four ECB target rate increases in 2022, starting from July and increasing rates to 0%. We expect increasing divergence between the Fed’s and the ECB’s policy stance, which would put downward pressure on the Euro while being favorable to European versus U.S. stocks.

As inflation rises, real incomes and purchasing power may decline in the eurozone, potentially dampening economic growth. Despite the war reducing real economic growth projections while pushing up inflation, the ECB currently reflects a low risk of stagflation. Markets generally align with this view, with the German yield curve remaining upward sloping. The ECB’s worst-case scenario currently projects 2.3% real GDP growth this year while their base case scenario is 3.7% real GDP growth followed by 2.8% growth in 2023. Their worst-case scenario includes suppressed supply of Russia’s oil and gas and a worsening of the war, pushing inflation to 7.1% from a base case expectation of 5.1% in 2022. The ECB expects inflation to normalize around its target of 2% in 2023.6

Higher Yields Kept the Spotlight on Valuations

The sharp increase in U.S. Treasury yields placed an even greater focus on dividends, profitability, and valuations – favoring value rather than growth while also supporting larger, more well-established companies. During Q1, the Russell 1000 Value Index and Russell 2000 Value Index took the lead with a decline of -0.7% and -2.4%, followed by the Russell 1000 Growth Index and Russell 2000 Growth Index with a decline of -9.0% and -12.6%, respectively. While the Russell 1000 Growth Index has relatively high P/E valuations, underlying profitability is less of a concern than in the small-cap space. Additionally, as inflationary pressures have risen, investors have been favoring segments that are better positioned to pass along inflation. Overall, the Russell 1000 Index (-5.1%) held up better than the Russell 2000 Index (-7.5%) during the quarter.

Ideas from Either Side of the Style Spectrum

Value was the focus of the first quarter with expectations for higher yields taking some of the shine off longer duration assets. But it remains important to maintain balance between value and growth, while tilting towards the segments that are well positioned for the current environment.

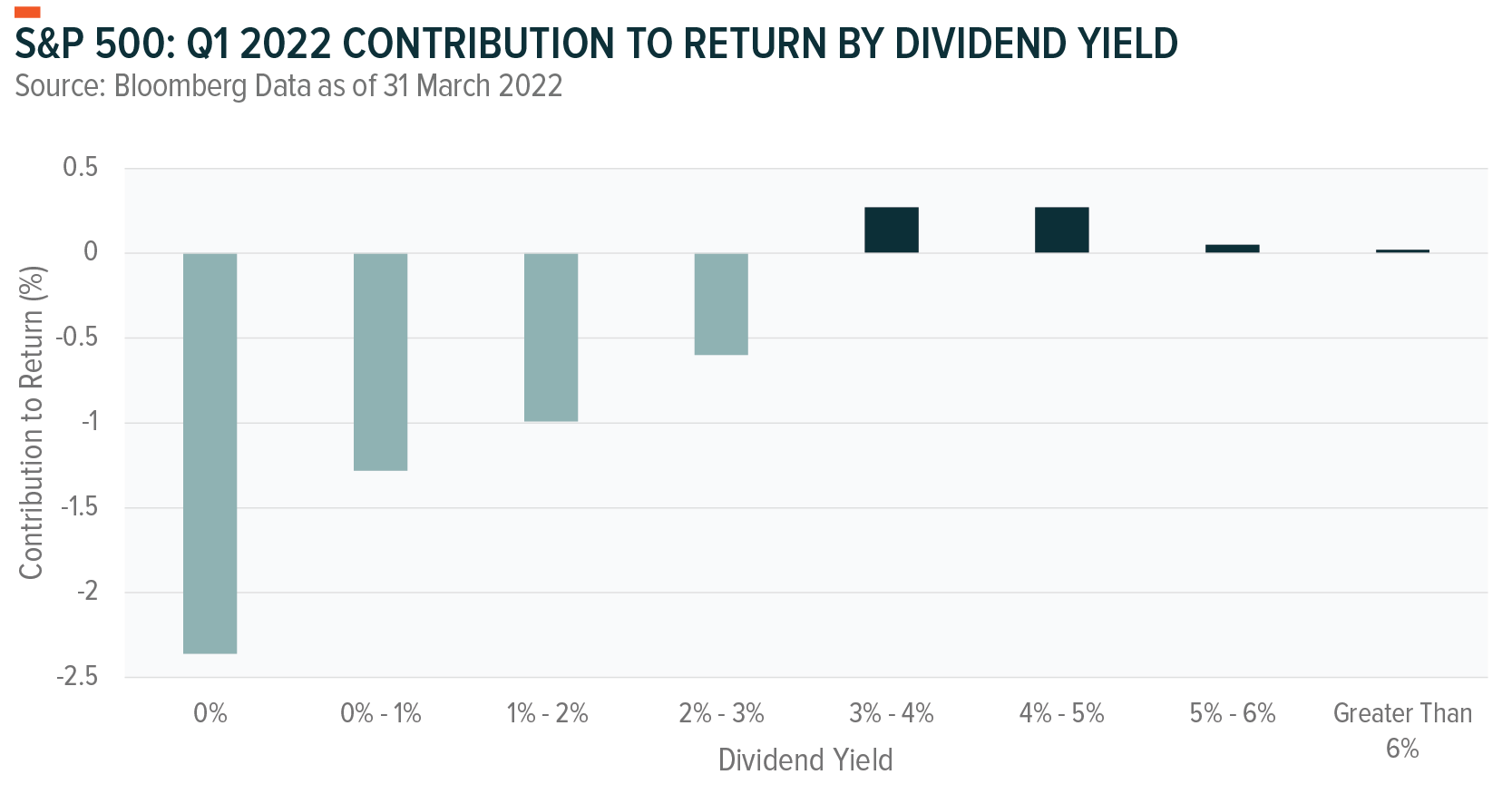

Higher yields have placed greater focus on solid cashflows and dividends, favoring equity income solutions. During Q1, there was a strong relationship between yield and return. The chart indicates that S&P 500 companies that did not pay a dividend or provided a low dividend yield drove the decline during the quarter. Conversely, higher yielding segments held up reasonably well. The strong performance from the Energy sector was particularly supportive to the 3-5% dividend yield region. Within the Energy space, MLPs provide a high yield and benefit from elevated energy demand and pricing.

On the other side of the style spectrum, cybersecurity is a high growth opportunity that remains well positioned, with the war in Ukraine focusing attention on the importance of strong cybersecurity. The White House’s new cybersecurity strategy includes government oversight and rules mandating minimum cybersecurity standards.7 Shifting cybersecurity from a voluntary investment, into a regulated investment that is necessary to do business is likely to rapidly increase adoption. The increased focus on regulating cybersecurity is also occurring in Europe.8

Energy Powers Ahead

Only two of the 11 GICS sectors had positive returns during the quarter with inflation fears and the war in Ukraine keeping the Energy sector center stage. The top performing sectors were Energy (+39.0%), Utilities (+4.8%), Consumer Staples (-1.0%) and Financials (-1.5%).

- The Energy sector is one of the few beneficiaries of WTI crude prices rising 33% year-to-date.

- Defensive sectors with reasonably strong yields held up well. The Utilities sector was the only other sector with a positive return. In the aftermath of the invasion, Utilities rallied as equity market volatility rose sharply and yield expectations were temporarily curtailed. Consumer Staples were slow and steady through the quarter. This sector was less impacted by both the invasion and changes in Treasury yields.

- The Financial sector, and banks in particular, benefit from higher long-term yields. This sector held up well as yields rose prior to the invasion. As focus shifted to economic growth concerns, this sector faced some headwinds. But stronger language from Fed and the rapid movement in Treasury yields propelled Financials to a strong end to the quarter.

Meanwhile, Communication Services (-11.9%), Consumer Discretionary (-9.0%), Information Technology (-8.4%) and Real Estate (-6.3%) were the weakest sectors.

- The sharp rise in Treasury yields detracted from all four sectors. Higher yields shifted the focus to valuations and dividends, weighing on growthier market segments.

- Weakness in the Communication Services sector was concentrated in a few large key holdings. A key streaming platform missed expectations on global membership growth while a large tech company’s privacy update adversely impacted targeted advertising for social media companies.

- Higher inflation, lower real disposable income, and concerns about real economic growth are shifting consumer choices between discretionary and staple consumption. This raises concerns about growth and margins in the Consumer Discretionary sector. This sector is one of the most labor-intensive sectors and is adversely impacted by delays and higher input and logistic costs. Subdued discretionary demand may make it harder to pass along higher prices.

- The Real Estate sector benefits from the increased focus on yields and provides a business model that can pass through inflation pressures. However, Real Estate is highly sensitive to rising yields due to its reliance on debt funding, as well as yields being a factor in property valuations.

Supply Chains Tied in a New Knot

Supply chains have been a recurring issue over the last two years. Just as markets were anticipating improvement, two new complications arose: the war in Ukraine and Omicron’s spread in China. These two factors impact inflation and supply chains differently, but both delay supply chain normalization. We currently only expect supply chain normalization in early 2023.

Starting with the war in Ukraine, this has disrupted commodity markets, shifting the sourcing of key commodities. The war has increased commodity prices and commodity price volatility while having implications for supply chains and shipping logistics. Europe’s scramble to find alternatives to Russian gas has increased the Baltic Dirty Tanker Index by 77% year-to-date.9

Rail links between China and Europe have been disrupted, forcing more goods onto ships and planes. Combined with increased shipments of liquified natural gas (LNG), this increases the logistical challenges and places greater pressure on ports globally. The increased demand for shipping comes at a time when China is undergoing its largest lockdowns since 2020 – raising concerns about the next wave of supply chain bottlenecks.

While Chinese President Xi Jinping is striving to minimize the economic impact of fighting COVID infections, China is not fully moving away from their zero-COVID policy. Currently, Chinese elderly remain at risk with only half the population over 80 being fully vaccinated.10 This reflects China’s weakness in dealing with the current Omicron wave. At the end of Q1, these lockdowns became more serious with the lockdown in Shanghai extended for a further ten days.11 This has serious implications for economic growth both in China and globally. The current Omicron wave is already dampening Chinese economic activity with manufacturing falling into contractionary territory with a PMI reading of 48.1. Output and new orders declined the most since February 2020 while export sales declined at their fastest rate since May 2020.12 These challenges will likely persist into April.

Weak manufacturing data is only half the story. While both Shanghai’s port and Pudong airport remain open, it is becoming increasingly difficult to receive passes to enter and unload cargo. Logistic companies are attempting to shift cargo to other ports to avoid a more serious logistical nightmare.13 Container throughput at eight major Chinese ports reflect that domestic trade in mid-March was 24.4% lower than the year prior while foreign trade had declined 1.2% relative to the prior year.14 This reflects the impact of Chinese versus global demand as well as the areas that were most impacted by restrictions in mid-March. Additionally, this comes at a time when there’s been greater demand for ocean shipping as rail freight from China to Europe is being redirected via the ports. These lock downs will have ripple effects globally. Global container shipping company, Maersk, has warned that there will be delays and higher costs associated with the lockdowns.15

Real Disposable Income Under Pressure

U.S. real disposable income has been declining since mid-2021 as wage growth lags inflation.16 Higher prices for essential purchases such as heating, transportation and food is likely to shift spending patterns from discretionary goods and services towards staples. Regaining control of inflation is a growing priority, particularly the highly visible aspects such as food and energy prices that are important for setting inflation expectations. While WTI crude prices increased 33% year-to-date, they ended the quarter around $100 / barrel after a volatile month where prices exceeded $125 / barrel intraday.17 Two key factors helped reduce crude prices during March:

- The U.S. will release 1 million barrels of oil a day from its strategic reserves to help improve the supply mismatch.18

- While adversely impacting global growth expectations, China’s COVID-19 lockdowns are helping to reduce commodity prices.

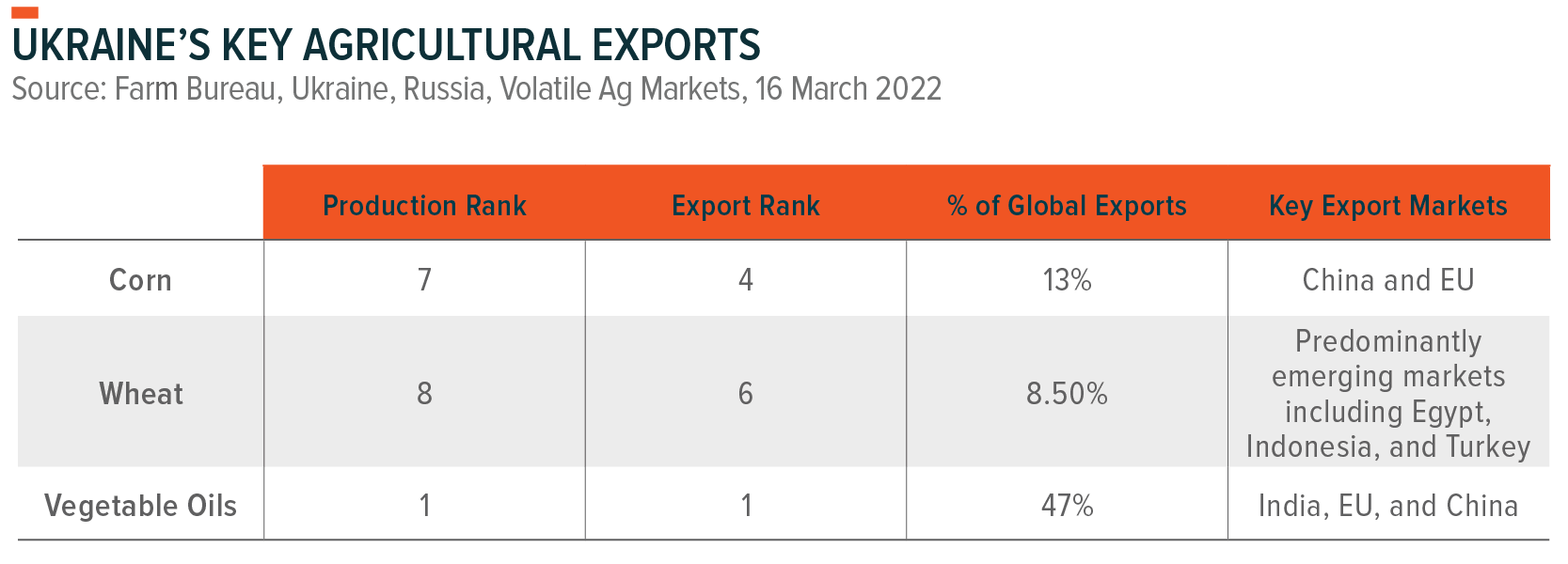

But energy is only part of the problem. Food prices remain a critical area that is likely to have longer term inflation implications. Ukraine is an important market for agricultural products including sunflower seeds and grains. Ukraine’s most productive agricultural lands are in the eastern regions that are most impacted by the war. A more drawn-out conflict is likely to have serious implications for acreage planted while potentially shifting the focus to support domestic food needs and the war effort. Ukraine’s spring planting season has commenced with sowing in late March until May determining the acreage planted for the year.19,20

These three crops represent key staple foods globally. While not all regions will be impacted by supply shortages, removing Ukrainian exports from the market will push up prices globally. This adds to inflation concerns for developed markets while potentially causing food security issues in more vulnerable emerging market. It should also be kept in mind that Russia is also a key exporter of wheat and vegetable oils. Combined, Russia and Ukraine account for around 30% of wheat exports and 76% of sunflower seed oil.21

Another complication to global food prices is fertilizer. Russia is a major global player in all three nutrients that create fertilizer: nitrogen, phosphate, and potassium. In 2021, Russia was the largest exporter of fertilizers. Russia accounts for 23% of ammonia (phosphate), 14% of urea (nitrate), 21% of potash (potassium), and 10% of processed phosphate exports.22 China, India, U.S., and Brazil are the largest importers of fertilizer products, accounting for around 57% of global fertilizer imports. While the U.S. is the third largest fertilizer importer at 10.3% of the market, they are less reliant on imports with only 9% of phosphates and 12% of nitrates being imported. However, 93% of U.S. potash is imported, with Canada and Russia being key import markets.23

Fertilizer is a global market and reduced supply from Russia will impact fertilizer pricing globally – potentially impacting the current planting seasons. Global food pricing remains a key area to watch as the war progresses. Reduced acreage and lower use of fertilizer may dampen yields and drive global food price inflation and issues of food security. These impacts will be felt over the next 12 months, potentially maintaining elevated inflation expectations for an extended period.

From an investment perspective, this focuses attention in three key areas: firstly, staples rather than discretionary consumption; secondly, innovative technological solutions to improve productivity; and thirdly, the growing importance of sustainability. We believe that AgTech and Food Innovation is likely to become a more important theme as food security and improved agricultural sustainability become a higher priority. Growth in controlled environment agriculture has the potential to improve efficiency in terms of water and nutrient use while also reducing dependence on growing seasons.24 Going beyond food security, we believe a greater focus on sustainability will be a lasting impact of both the COVID-19 crisis and the current war in Ukraine. These disruptions are changing how companies and investors prioritize items that impact both social and environmental factors.

Aspirations of Energy Independence Meet Carbon Neutral Solutions

Europe’s current energy crisis highlights the importance of energy independence. Despite the March 31 deadline for gas payments in rubles, and Europe’s rejection of this update to their supply contracts, Europe continued to receive Russian gas flows.25 But this situation remains fluid and critical as Europe relies on Russia for around 40% of its natural gas.

Given the impact on inflation and real economic growth, energy transition is a key economic priority. The EU is looking to reduce its purchases of Russian gas by about two-thirds by the end of 2022 and end purchases of Russian fuel before 2030.26 Europe’s energy transition is likely to be through a combination of renewables, liquefied natural gas (LNG), and nuclear energy. While there are opportunities in all these areas, each has short-term constraints in solving the current energy crisis.

Liquified natural gas (LNG) – Cleaner than coal, but still not green (25% of current EU electricity)27:

- The U.S. has committed to supply Europe with an additional 15 billion cubic meters (bcm) of LNG while raising this additional supply to 50 bcm by 2030. The initial commitment represents only a tenth of Europe’s 2021 natural gas imports from Russia.28

- While U.S. companies are investing in new LNG plants to meet this demand longer term, there is limited current capacity.29

- European infrastructure may be another challenge in the short term. Converting LNG back to natural gas requires facilities for regasification. While there is spare capacity in western countries such as Spain and France, poor connections make it difficult to move this natural gas to the eastern regions that are most reliant on Russian gas. Germany has promised to build two LNG facilities, but this will take several years.30

- MLPs provide some exposure to natural gas pipelines in the U.S., an area that is likely to benefit from increased export demand for LNG.

Nuclear power – Carbon neutral (25% of current EU electricity)31:

- On route to reaching their carbon targets, nuclear power has the potential to be a cleaner solution that assists with the transition to renewable energy. The European Commission has given nuclear energy the green label.32

- Nuclear power comprises 25% of current EU electricity. This only has the potential to increase slightly during 2022 as a new plant in Finland comes online and several plants are brought back online following maintenance. However, the increased power generation from these plants could be offset by four reactors that are scheduled for closure by the end of 2022. Delaying these reactor closures could reduce EU gas needs by around 1 bcm per month.33

Renewable energy (22% of current EU electricity)34:

- Renewable energy has the benefit of being a cheap, clean, and potentially endless source of energy.

- Strong market sentiment towards renewable energy strategies, notably hydrogen and solar, could indicate that investors expect a significant shift in the adoption of renewables in Europe.

- Thus far in 2022, there has been a significant increase in solar PV and wind power capacity. These additions are expected to raise EU output from these renewable sources by 15% to 100 terawatt-hours (TWh). A further 20 TWh could be added during the year through fast-track renewable capacity additions and tackling permit delays. Additionally, faster deployment of rooftop solar PV combined with short-term grants covering 20% of installation costs could double the pace of solar instalment, potentially increasing rooftop solar PV systems by 15 TWh. This combined 35 TWh increase in wind and solar power generation would reduce natural gas needs by 6 bcm (4% of Russia’s natural gas imports in 2021).35

- As part of reducing reliance of Russian gas, there is currently a push towards increasing the EU’s 2030 renewable targets to 45%, from a current target of 40%.36

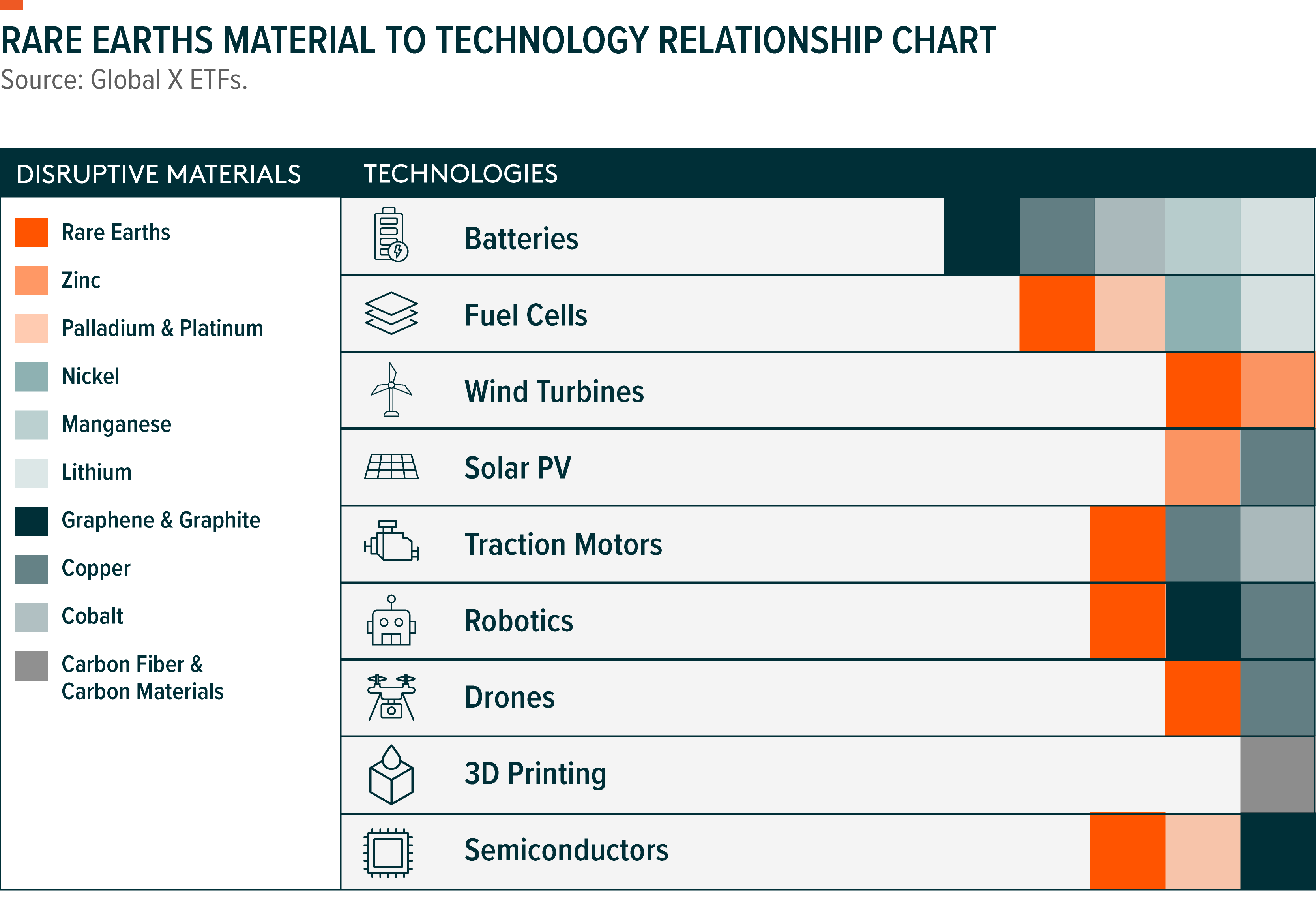

The transition to a greener future requires raw materials. Disruptive Materials are metals, minerals and elements that are used in emerging technologies and are thus expected to be highly important in the future. These raw materials are important for both the digitization of the economy and the shift towards clean energy. While the structural theme remains technological advancement, the underlying exposure is focused on material companies. In an environment focused on inflation and higher yields, this is potentially an interesting way to provide exposure to technological change.

Diversification, Balance and Quality

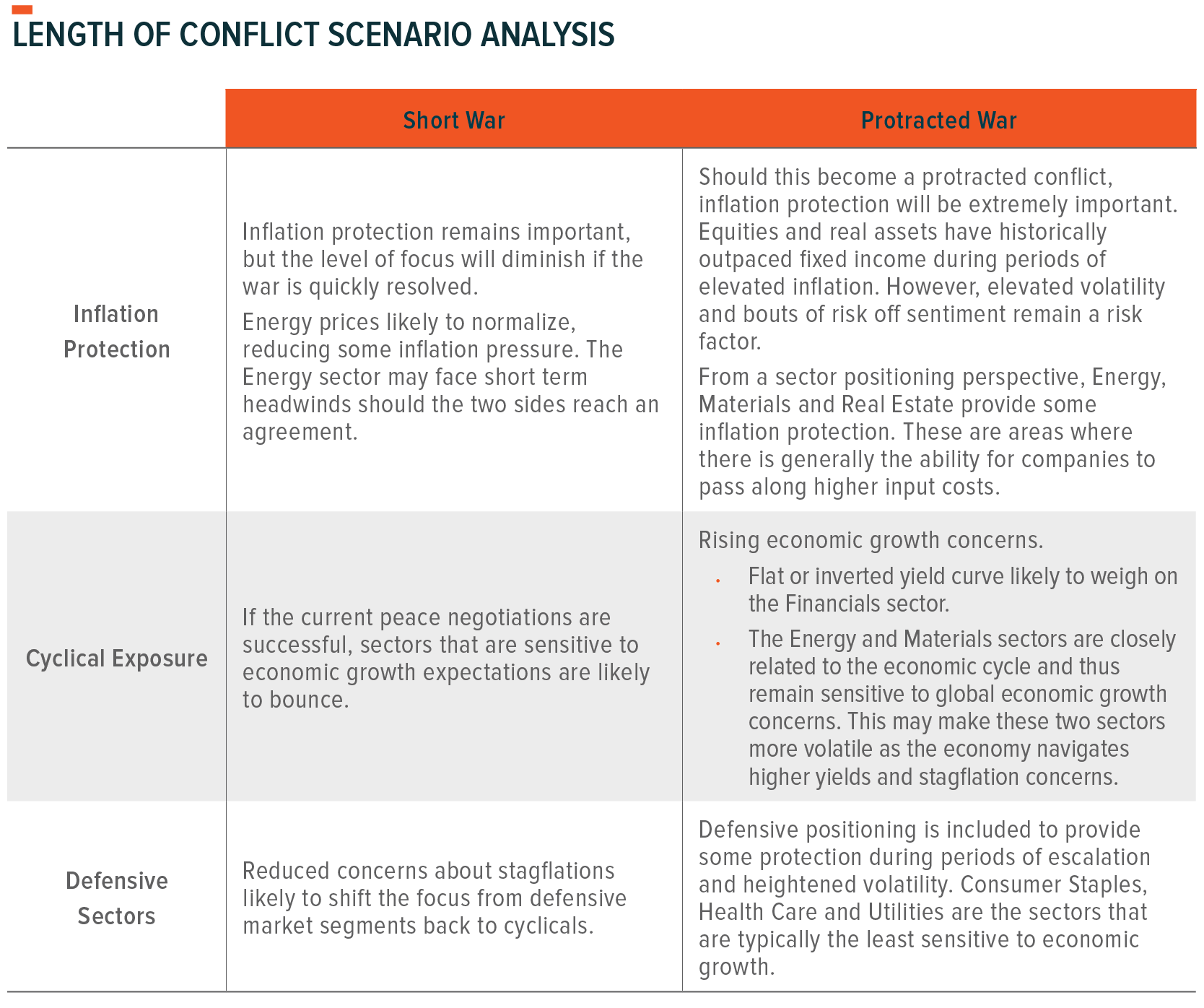

The current environment is a balancing act for investors. Concerns about elevated inflation pressures, but also slowing real economic growth. This is a time that calls for focus on inflation protection while scaling back on cyclical exposures and increasing defensive positioning. Each of these three areas are impacted differently by the length of the conflict in Ukraine. While we hope for a quick resolution, we believe it’s prudent to prepare for a more protracted war, providing some balance between these two potential outcomes.

Regardless of the war’s length, the Fed has indicated they plan to continue raising interest rates in 2022 and 2023. We believe we’re moving into a late cycle environment where quality tends to outperform. Given expectations for an aggressive rate raising cycle, fixed income is less likely to provide strong diversification benefits. This increases the importance of diversification and allocation decision within the equity sleeves.