Morgane Delledonne

Morgane DelledonneSignificant macroeconomic challenges remain, but investors may have reason to believe that Europe passed peak pessimism. Russia does not have much energy leverage left, and following the massive selloff in European assets in recent months, most of the energy supply shock looks priced in. Europe appears to be serious about curbing stubborn energy inflation, evidenced by a potential price cap on natural gas needed for electricity.

The UK government’s decision to reverse its proposed tax cuts helped assets rebound somewhat. While the Bank of England (BoE) is expected to hike by over 200 basis points (bps) before year-end, we believe there is an increasing chance that the bank postpones quantitative tightening (QT) until 2023. Reducing gilt buying by £80 billion over the next year at a time when gilt supply is expected to rise dramatically would not bode well for the BoE’s financial stability objective.1

In Italy, the electoral victory of the far-right coalition led by Giorgia Meloni resulted in a limited market reaction, with the bund/btp spreads widening by only 8bps following the results. The market reaction may be more significant come the end of October when the new government is formed and its key fiscal programs become clearer, which is important given that the country’s 150% debt-to-GDP ratio.2

Outside Europe, China’s 20th Party Congress indicated that China is preparing more aggressive easing and growth-oriented policies, even with leadership hesitant to abandon its zero-COVID policies. Recent declarations from the People’s Bank of China (PBOC) indicated a shift toward increased liberalization, pointing to greater monetary independence and an unwillingness cap the yuan’s weakness.3

It’s the opposite in the U.S., where the dollar remains strong, to the benefit of domestically oriented U.S. companies, particularly those in the middle of the Biden administration’s push to decarbonize infrastructure. The U.S. Dollar Index (DXY) could stabilize at its high in the coming weeks, but it seems poised to weaken as monetary conditions become restrictive. Neither the labor market nor inflation will derail the Fed’s tightening. We expect the Fed to remain on its tightening path and increase the fed funds rate as long as there is no sign of a marked slowdown in hiring, wage growth, and core inflation.

Investment strategies highlighted this month:

- Renewables Benefit from Europe’s Likely Move To Cap Gas Prices – Capping gas prices to help curb inflation can preserve superior profit margins for renewable energy producers. More broadly, Europe’s energy security and decarbonization goals will spur R&D in cleantech, solar in particular.

- 20th Party Congress Policy Agenda Positive for Chinese Equities – We expect further easing of monetary and fiscal policies to boost growth prospects and earnings expectations, and possibly trigger a rebound in Chinese equities.

- Technology to Help U.S. Firms Navigate Difficult Conditions – Tech stocks have been battered this year, but we believe bright spots will emerge as U.S. companies invest in productivity-enhancing and cost-saving technology.

Europe’s Renewables: Energy Security and Decarbonization Push Spurs Investments

We believe investors have reason to be slightly more optimistic about Europe as it progresses in its energy transition. The region’s dependence on Russian gas is now just 9%, down from 40% before the invasion of Ukraine. Gas reserves are at about 88% full, within range of the European Commission’s (EC) requirement of maintaining reserves at 90%, though most European countries still need to save 10–15% of their gas consumption to comply with the EC’s targets.4,5

In the real economy, consumers, companies, and governments must make do with less and more expensive energy. Countries such as France, Portugal and Spain have it easier, as they were hardly dependent on Russian energy. The situation is different in Eastern and Central Europe, given their reliance on Russian gas, but countries are pivoting. Germany unveiled a new €200 billion stimulus package, which should help support consumers and business activity over the winter months and improve the outlook for the region overall.6 The outlook is less optimistic for Italy and the UK, where political uncertainty compounds the economic uncertainty and fiscal and financial risks are rising.

Further coordinated measures seem likely, including a price cap on natural gas. If implemented at the EU level, this measure would partially subsidize energy consumption, relieving some of the burden on consumers and companies. The exact structure remains unclear, including the financing and whether fossil energy companies’ profits will be tapped. Also, we expect changes in the energy pricing system that decouple natural gas prices from other electricity sources, including liquified natural gas (LNG), wind, solar, and nuclear.

However, the EU is unlikely to drastically change the “pay-as-clear” mechanism in the European energy market, where the most expensive energy source dictates the price of a kilowatt-hour of electricity. Under this pricing model, producers of cheap electricity, such as renewables, sell their electricity at the highest price, which is often the gas price. This model is positive for renewable energy producers because it can result in high margins. The net profit margin for European renewable energy producers is 11.6% currently, versus 7.4% for the rest of the world.7

For investors, what should be increasingly clear is that Europe will not return to its 2021 energy mix. Europe’s expedited moves to secure its energy and decarbonize have spurred numerous initiatives. Notably, REPowerEU is the EC’s plan to cut make Europe independent from Russian fossil fuels well before 2030. The plan includes a rapid rollout of solar and wind energy projects combined with renewable hydrogen deployment. The EC estimates that 780 gigawatts (GW) of solar and 510GW of wind power must be installed across the region by 2030 to meet REPowerEU’s objectives. As part of the REPowerEU’s plans under the modified Recovery and Resilience Fund, the EU announced a €300 billion investment in renewables and cleantech and the electrification of infrastructure and transportation.8

In addition, urgent needs include new grid balancing and back-up power sources, currently provided mainly by fossil fuels, hydro, and nuclear. Other large-scale projects include geothermal and nuclear fusion studies. Also, the European Space Agency (ESA) proposed a research and development (R&D) program to develop commercial solar power stations in space. Dubbed the Solaris project, European science ministers are set to evaluate its feasibility in November. In 2050, solar is expected to be the single largest contributing energy source to the EU, accounting for 40% of the EU’s energy.9

We view companies that manufacture, operate, or supply components for renewable energies such as solar panels, wind turbines, nuclear components, and hydrogen as attractive given the demand prospects. Raw materials like nickel, cobalt, copper present opportunities for the long term. In the short to medium term, uranium is core to renewed focus on nuclear energy.

Chinese Equities: Rebound Can Materialize Amid Easing Policies

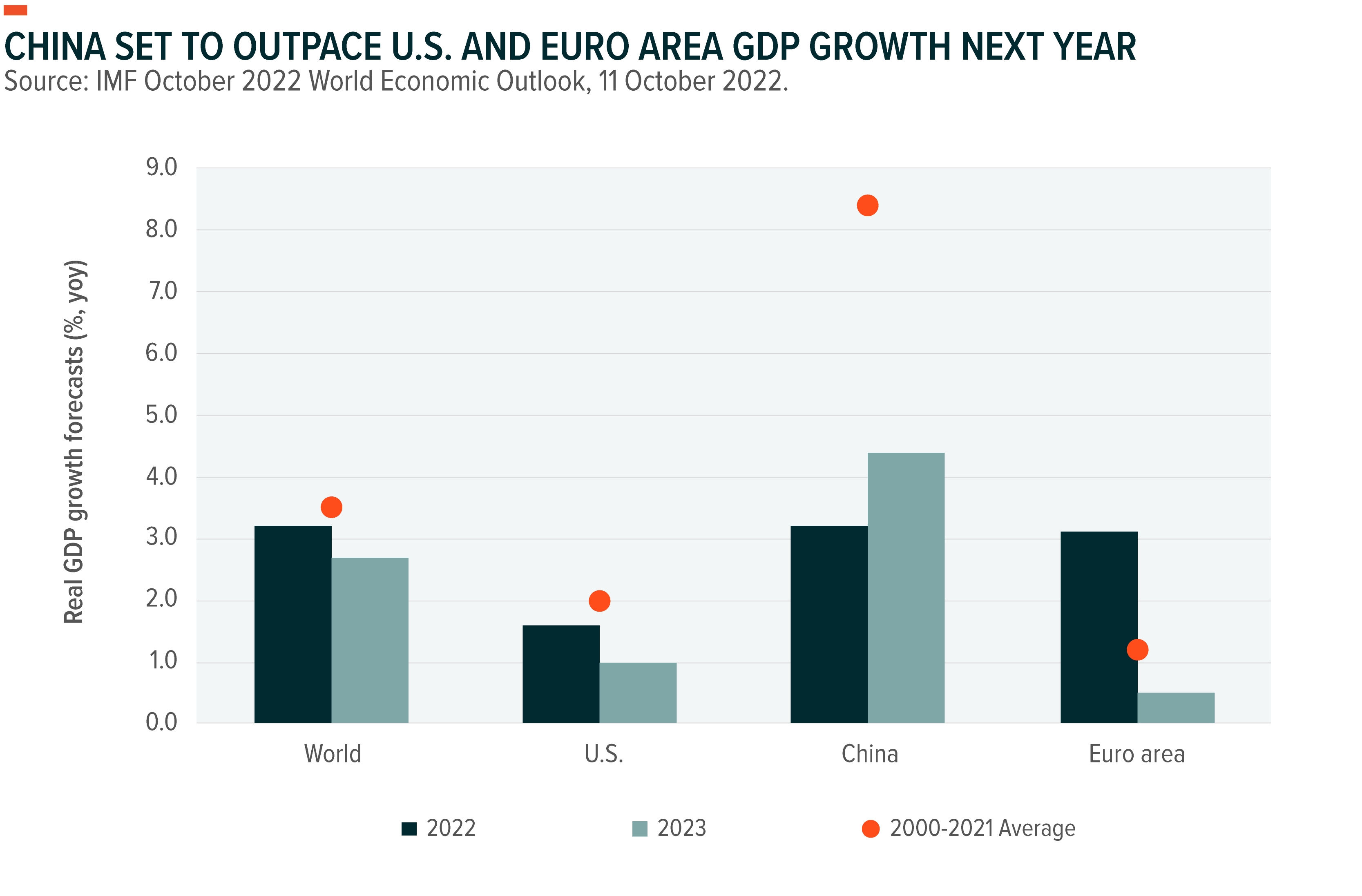

China started on its path to easier monetary and fiscal policy due to the Omicron variant, which resulted in several long lockdowns this year. With dampened consumption and business activity amid the government’s zero-COVID policy, the International Monetary Fund (IMF) forecasts China’s economy to grow just 3.2% in 2022.10 The strong U.S. dollar reducing global demand and the risk-off environment created a challenging investment backdrop for Chinese equities. However, positive signs include industrial production and manufacturing production improved slightly in in September.11 For 2023, the IMF forecasts China’s growth to accelerate to 4.4% in 2023, outpacing global GDP growth forecasts of 2.7%.12

The 20th National Congress of the Chinese Communist Party in October, at which President Xi unveiled new party leadership for the next five years, offered additional reasons for optimism about China’s growth trajectory. The government seems determined to boost growth and achieve three key targets: common prosperity, technological and manufacturing self-reliance, and liberalization of market access. However, Xi’s declarations at the Congress about prioritizing national security and stronger military alongside the reaffirmation of opposition to Taiwan independence point to elevated geopolitical uncertainties in the region. These factors could weigh on investment sentiment for Chinese assets and cap near-term growth prospects.13

First, China’s objective to reduce inequality and shift to a consumer economy, so-called “common prosperity”, could benefit consumer discretionary-oriented sectors and themes as easing measures take hold. The effects of these measures depend on the number of COVID cases and resulting lockdowns, as Xi reiterated the government’s commitment to the zero-COVID strategy.14

Second, China’s push to develop its domestic semiconductor market illustrates the country’s goal of technological and manufacturing self-sufficiency. The focus on semiconductors is likely to accelerate following President Biden’s announcement of additional export control restrictions on chip companies. Chinese hardware technology companies could gain domestic market share as a result and increase profits for chip companies like SMIC, China’s largest semiconductor manufacturer.

The People’s Bank of China is likely to help the corporate landscape by cutting banks’ reserve requirement ratio by at least 25bps by year-end. With accommodative monetary conditions and increasing tax refunds and tax cuts and deferrals, corporate loans rose to 1.35 trillion yuan in September, nearly double from a year ago.15 We expect most of this funding to be directed to infrastructure developments.

And for the third objective, recent PBOC policy decisions indicate a reluctance to intervene heavily to cap the yuan’s weakness. The central bank’s preference for a market-driven approach to stabilize the currency point to greater monetary policy independence and exchange rates liberalization.

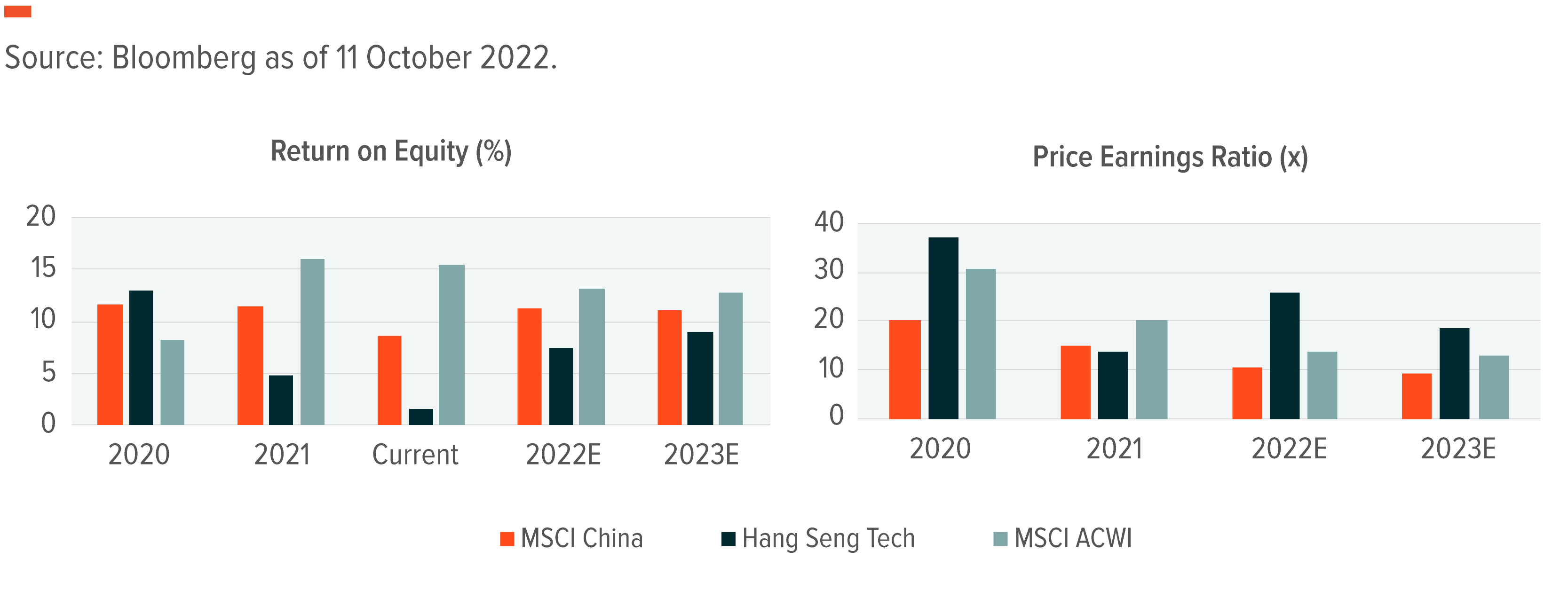

From a market standpoint, Chinese stock valuations are compelling, in our view. Following the large selloff since early 2020, Chinese stocks captured in the MSCI China index are trading at 10x forward earnings, close to their 2011 lows.16 Chinese stocks’ return on equity (ROE) could beat expectations in 2023, should China implement additional easing measures to boost economic growth. Sectors that are likely to outperform in the next year include Tech, Industrials amid higher defense spending, and Consumer Discretionary, led by automobiles and electric vehicles. Consensus aggregated by Bloomberg shows that analysts expect the combined earnings of companies in the Hang Seng Tech index to rebound over 10% in 2023 and close to 40% over the next two years. In comparison, analysts forecast the combined earnings for the broader MSCI China Index to grow 6% in 2023 and 11% over the next two years.17

Themes that look well-positioned to benefit from this upside potential in Chinese stocks include Renewable Energy, including solar, an industry where more than half of the constituents are produced by Chinese companies, and wind. Other themes that can benefit include Lithium & Battery Technology, Disruptive Materials, and E-commerce. These themes should not only benefit from the global structural push for digitization and decarbonization, but also local tailwinds from Chinese policies to stimulate growth.

U.S. Tech: Productivity Enhancers and Cost Savers Are Bright Spots

While high inflation, slowing growth, and market volatility may make investors skittish, these dynamics can create compelling investment opportunities as companies adjust to this challenging operating environment. Investing in technology is one way for companies to achieve higher productivity gains, especially in the U.S., where the job market is likely to remain tight and wage growth elevated.

In September, the U.S. unemployment rate dropped to 3.5%, despite the Fed’s tightening.18 The growth in average hourly earnings remained at a monthly pace of 5.0% yoy, which is not consistent with the Fed’s 2% inflation target.19 We expect the supply of workers to keep pressuring the job market, due in part to a large group of U.S. workers set to reach retirement age. The possibility of a downward trend in the participation rate will not help bring down wage growth in the medium term.

We expect cost-reducing technologies will be in greater demand as price levels rise. Longer-term, technology’s role in cost reduction is likely to increase significantly in the next decade, given the likely reversal of globalized manufacturing that led to decades-long deflation. For example, developed economies’ heightened focus on economic resilience through energy security and end-to-end supply chain controls, coupled with the prospect of stubbornly higher inflation, suggest greater investments in robotics and automation. In our view, dampened valuations in the Tech sector currently offer attractive entry opportunities in companies active in these technologies.

Some of the top disruptive themes that will enable productivity gains and cost reduction are trading at a discount to the broader market while providing better risk-adjusted returns. Renewable Energy, U.S. Infrastructure Development, Cybersecurity, Lithium & Battery Technology, and Disruptive Materials have been relatively defensive compared to the broader market while also standing out as key drivers of growth for the next decade among the clean energy and digital transition.