Global X Research Team

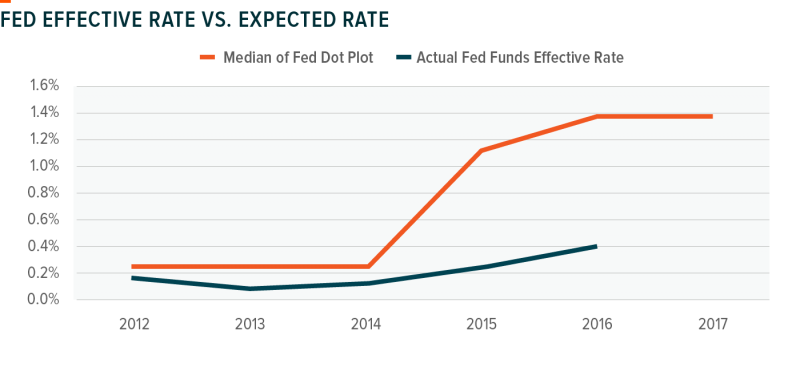

Global X Research TeamOn Wednesday December 14th, the US Federal Reserve (“the Fed”) announced a rate hike of 25 basis points, bringing the range of the federal funds rate to 0.50% to 0.75%.1 The rate hike is the second in a decade and the first and only rate hike announcement in 2016. This is in stark contrast to guidance from the Fed in late 2015 in which its members foresaw four rate hikes occurring in 2016.

The Fed believes there will be three rate hikes in 2017, yet we are somewhat skeptical of this outlook as the Fed has consistently overestimated rate hike expectations over the last few years. In the chart below, we show the Fed’s year-ahead interest rate expectations based on the median “Fed Dot Plot” of Fed Open Market Committee (FOMC) members. For example, at the end of 2014, the median expectation of FOMC members was that by the end of 2015, short term interest rates would reach 1.13%. In reality, the Fed Funds Effective Rate at the end of 2015 was 0.24%.

Source: Bloomberg: 2012 to 2016

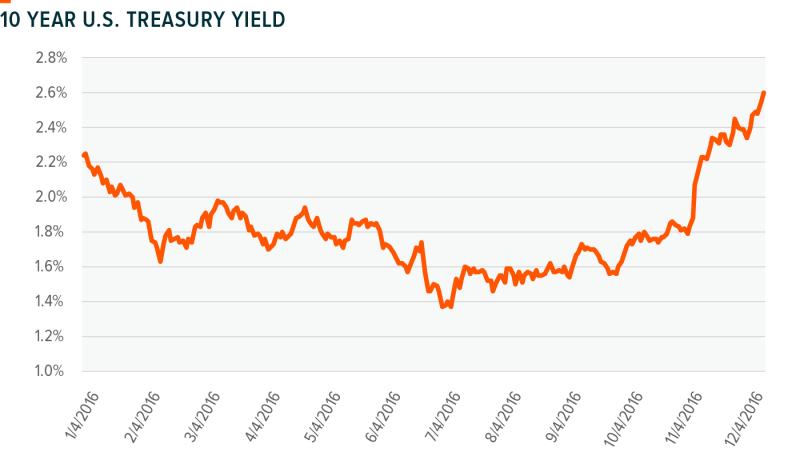

While the 2016 news cycle has often been dominated by what the Fed would do with short term interest rates, the more dramatic event has been changes in the 10 Year US Treasury, which are controlled by the market, rather than the Fed. In addition, the 10 Year US Treasury includes greater expectations for long-term inflation. The 10 Year US Treasury has surged over 100 basis points since it reached a bottom in July as rate hike and inflation expectations have risen.

Source: US Department of the Treasury. 1/1/2016 to 12/15/2016.

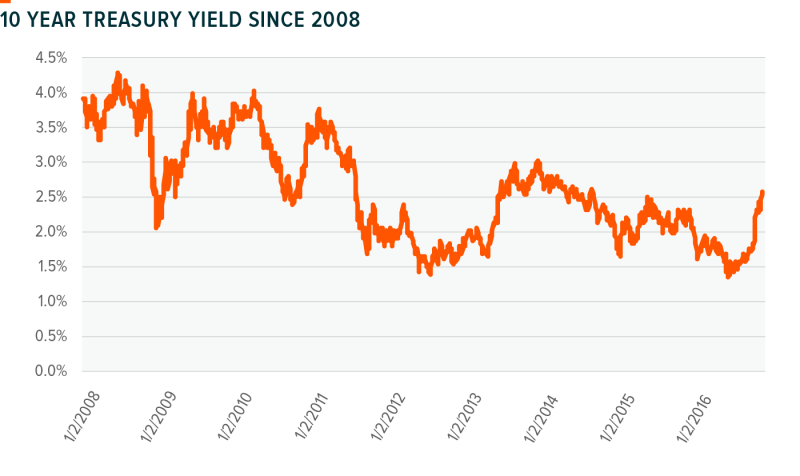

To put this increase in context, the 10 year treasury is now yielding 2.6%, which is virtually identical to its average yield since the beginning of 2008 and on par with the yields in 2013 and 2014.

Source: US Department of the Treasury. Data from 1/1/2008 to 12/15/2016.

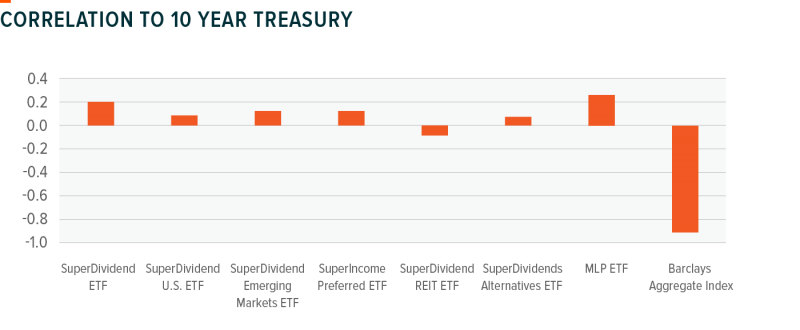

Despite the recent upswing in 10 year US treasury yields, we saw that many high dividend paying stocks responded neutrally or mildly positively. In the chart below, we show the one-year correlations of the price changes of the SuperDividend suite of ETFs, which invest in many of the highest yielding securities in various geographies and asset classes, to the changes of 10 year US treasury yields.2,3 We found a slight positive correlation between the SuperDividend suite of ETFs prices and 10 year US treasury yields, indicating that as 10 year US treasury yields increased, there was a slight increase in the prices of the SuperDividend ETFs. The chart below also shows the correlations of the 10 year US treasury yields to the price changes of the broad US fixed income benchmark, the Bloomberg Barclays US Aggregate Bond Index.4 As expected, the rising 10 year US treasury yield closely corresponded with a decrease in the price value of the Bloomberg Barclays US Aggregate Bond Index, indicating how traditional fixed income investments tend to suffer in a rising rate environment.

Source: Bloomberg: 12/15/2015 to 12/15/2016.

We have conducted research on the performance of high dividend payers in a rising rate environment and found that high dividend payers have performed well in environments where interest rates are increasing gradually. This relationship is due to the fact that high dividend payers exhibit value characteristics and tend to benefit from a strengthening economy with mild inflation, which is often the case when 10 year treasury yields are moderately increasing. Given that the Fed’s interest rate increase expectations remain gradual5 with three expected increases in 2017, their recent history with overestimating the speed of rate increases, and the fact that the 10 year treasury’s recent spike was more of a normalization to recent averages, we believe that high dividend and alternative income strategies can continue to perform well in this environment.