Rohan Reddy

Rohan ReddyThe following is Part 2 in a 3-part blog series on the market making landscape for exchange traded options. This part dissects additional options risks that options market makers will need to consider when enacting hedging trades. Part 1 discussed the role of liquidity providers when it comes to making a market in list options. Part 3 will discuss potential option market impacts on market volatility and considerations when analyzing the growth in ETF usage of such contract types.

In part 1 we discussed how market makers play a significant role within the listed options ecosystem. The 5 option greeks are key metrics monitored by this group of market participants to ensure their profit stream is isolated to their trading activities. Thus, their trading activities do not represent a market view, but their ability to manage their options exposures swiftly. These risk metrics are key, however, we will continue this series by exploring the most commonly known, second order greek, gamma. Furthermore, we will explain how delta and gamma are managed simultaneously by market makers.

Key Takeaways

- We explore how embedded economic leverage found within an option results in sharp movement risks, or option gamma. This is another consideration for option market maker hedging activities.

- Market makers need to hedge delta to eliminate directional risks, however, we demonstrate how this isn’t enough and selling or purchasing options may be needed for a full hedge.

- To limit option gamma risk, a measurement of option delta sensitivity, market makers may combine both stocks and options in their hedging trades for a complete hedge. We explain how both delta and gamma may be neutralized simultaneously.

Hedging Quickly Is Key to Market Makers Mitigating Sharp Price Moves

Gamma measures the sensitivity of delta. Market makers monitor it to measure an option’s sensitivity to potentially large price swings in its underlying asset. For example, if a long call option position has a delta of 0.47 and a gamma of 0.03 and the underlying asset increases in value by $1, the new delta is expected to be 0.50. Because delta is more closely associated with an equity option’s linear risks, it can be hedged by taking the opposite trade in the underlying equity asset. Gamma risk can only be hedged using other option contracts because stocks are not derivatives and do not exhibit the convex characteristics of this sensitivity factor. This gamma hedging effectively helps to create the needed delta hedging.

As an option nears expiration, gamma is expected to be at its highest when an option is trading at-the-money (ATM) or in close proximity to ATM. Option deltas for these types of contracts move quickly since time is running out to trade the contract. This time value component is typically measured by the theta greek. The volatile movements in gamma and delta values are key components of what drives market maker hedging trades that can offset these risks as efficiently as possible.

As an option nears expiration, gamma is expected to be at its highest when an option is trading at-the-money (ATM) or in close proximity to ATM. Option deltas for these types of contracts move quickly since time is running out to trade the contract. This time value component is typically measured by the theta greek. The volatile movements in gamma and delta values are key components of what drives market maker hedging trades that can offset these risks as efficiently as possible.

Hedging Against Delta Is Not Enough To Fully Offset Sharp Movement Risks

As we discussed previously, hedging directional risk, or delta hedging, alone with equities or equity-linked futures only allows market makers to hedge against smaller movements because they don’t have enough time to react to sharper movements in the underlying equity asset. Options are likely needed, especially with respect to gamma hedging, because they have a level of economic leverage, which makes them more volatile when the underlying equity asset moves sharply. When offsetting a short option position, going long an option with similar characteristics assists in neutralizing this gamma exposure. In practice, these hedging trades are implemented quickly to limit these risks, likely through computer programs or algorithms designed for these trading scenarios.

Within the example provided, we recognize how owning the underlying asset offsets directional risks of the short call option and neutralizes delta completely. Therefore, the profit and loss contribution is primarily coming from the gamma exposure embedded within the short call option position. This is not a complete hedge and market makers will need to seek out gamma exposures via other options contracts as a means to neutralize such risks.

Hedging Against Delta and Gamma Provides A More Complete Hedge

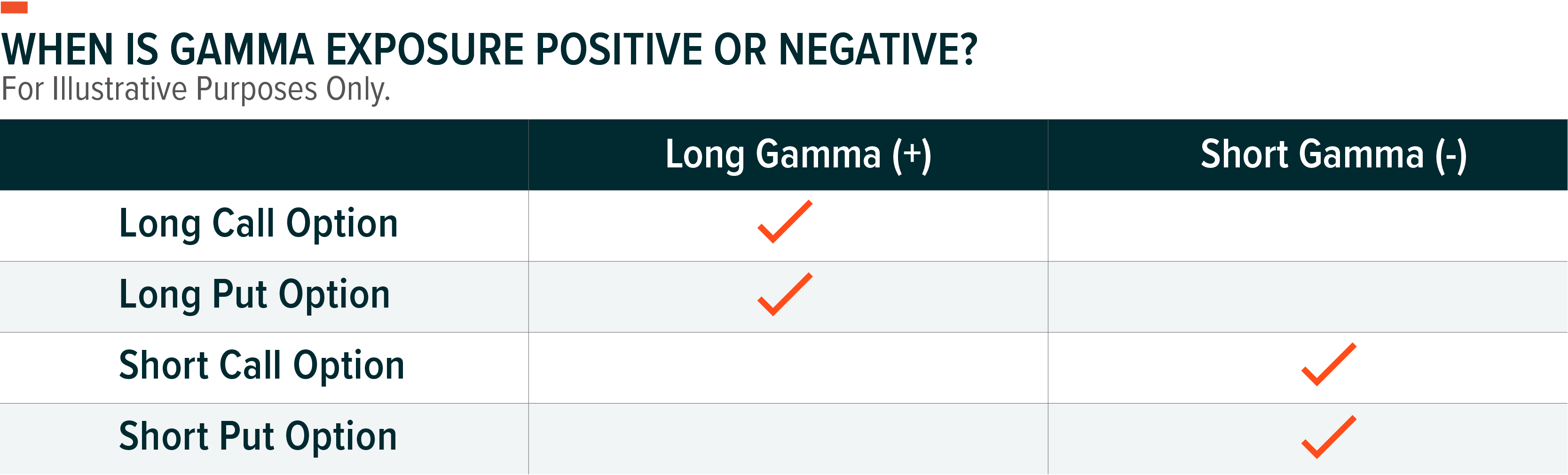

Tangentially similar to delta, gamma can also be represented by either a positive or negative number depending on the side of the trade each participant is on. Regardless if an investor is long or short an option, this investor has gamma exposure. The side of the options trade itself will determine if an investor or market maker is either long or short gamma.

A market maker may offset positive or negative gamma with option hedging trades by going long or short an option of similar characteristics and contract specifications. When hedging stock option greek risk, delta and gamma may be hedged by utilizing options and shares of the underlying stock simultaneously to provide a full hedge. Using the same example above, we can see how both delta and gamma risks are effectively neutralized by implementing options and underlying stock within the same hedging trade.

Within our example, options gamma has been effectively neutralized, all else equal.

- The market maker using out-of-the-money (OTM) call options of the same underlying asset may have been expected to purchase 1.14 contracts for every 1 contract of its ATM call option counterpart contract to effectively neutralize gamma.

- Since the market maker is also long a 0.25 delta call option, the number of shares purchased to achieve full delta neutrality was cut in half since the previous example.

The potential for losses within this hypothetical example has been significantly reduced and 1-day losses are only expected to occur for significantly large movements in the underlying asset. This is typically a factor of potential changes in implied volatility, measured by vega, affecting option pricing amidst these less likely events. We should caveat that this is a simplified example where delta and gamma are at play. The other greeks can affect options pricing too.

We can see below that when actively hedging delta and gamma risks, the exposed P/L position has much flatter tails than when just purely delta hedging.

Other greeks representing time value (theta) and interest rates (rho) are expected to impact option valuations and is utilized as an input within the Black-Scholes options pricing model, a pricing model typically used for valuing European-style options. In practice, delta changes throughout the day thus market makers will likely modify their delta hedge ratios on a continuous basis.

The underlying reference asset underpinning an options contract is another consideration. Generally speaking, U.S. large cap stocks are more liquid than small-caps and international equities, therefore cheaper to trade. This may be further pronounced when attempting to hedge long options exposures of the latter asset classes.

Conclusion: Options Market Makers Need to Be Nimble

With an average daily volume of 42 million contracts in Q2 2023 relative to nearly 15 million contracts in Q2 2013, this continued growth requires market makers to be even more efficient in their distribution of liquidity, quotes, and information to investors.1 This growth is also a testament to the ease of access listed options contracts offer with the assistance of market makers on standby to provide liquidity. In practice, option deltas change throughout the day thus market makers will likely modify their delta hedge ratios on a continuous basis.