David Beniaminov

David Beniaminov Michelle Cluver

Michelle Cluver

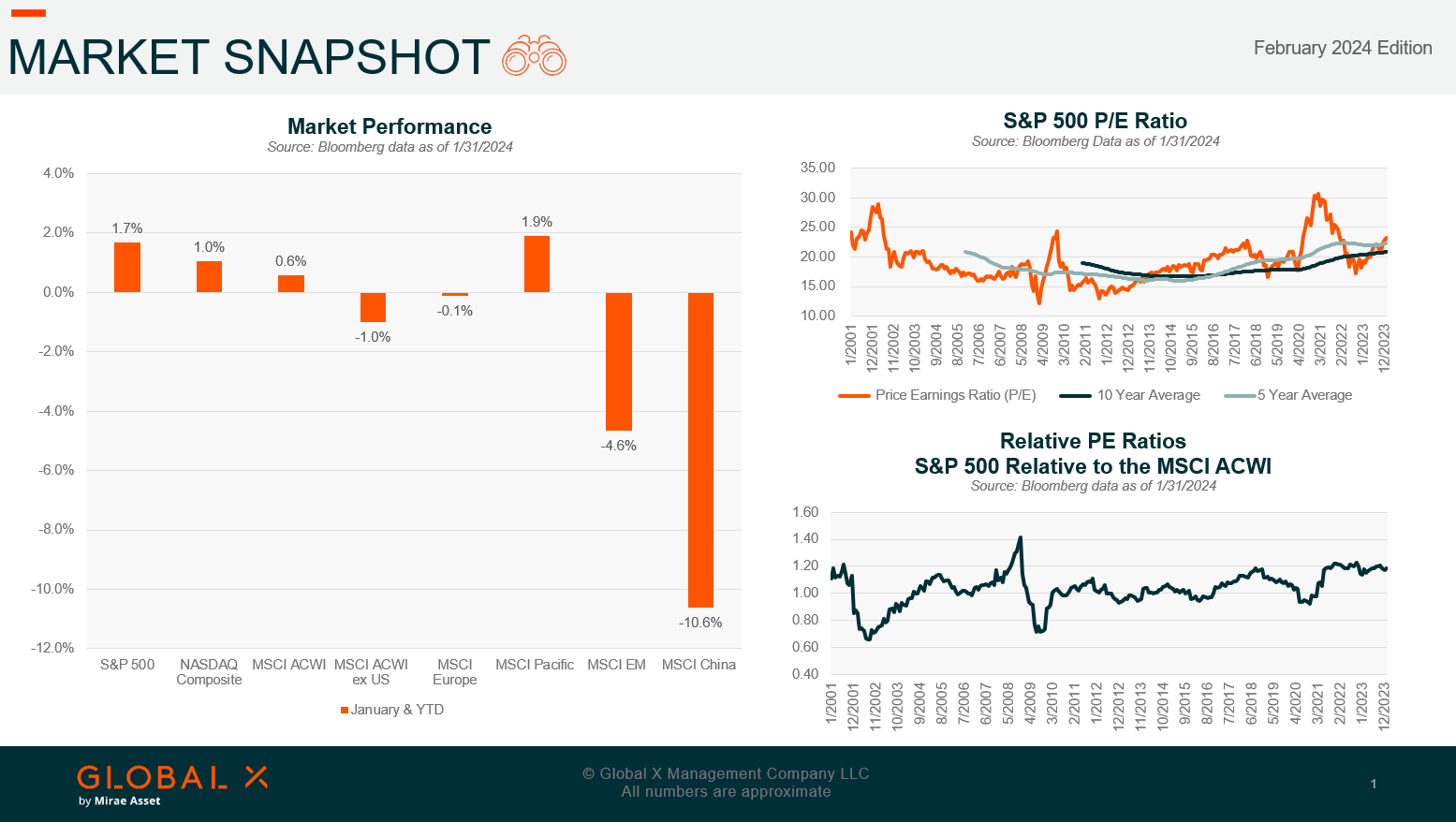

U.S. equities continued their rise in January, with the S&P 500 Index rising +1.7% as the soft-landing narrative continued to dominate market sentiment. Markets were supported by better than expected Q4 2023 GDP growth, strong December retail sales figures, and a softer but still robust labor market.

Market breadth narrowed again, supporting large cap growth. The Russell 1000 Growth Index rose +2.5% while the Russell 2000 Growth and Value Indexes fell -3.2% and -4.5%, respectively. Sector performance was mixed, with Communication Services and Information Technology pushing higher +5.0% and +3.9%, while Real Estate and Materials decreased -4.7% and -3.9%, respectively.

The 10-Year Treasury yield peaked at 4.18% as markets push back interest rate cut expectations. However, earnings weakness in select regional banks raised concerns about commercial real estate, putting downward pressure on Treasury yields at the end of January. The 10-Year Treasury yield ended the month at 3.91%, essentially unchanged.

Global equities lagged and emerging markets (EM) felt pressure from a stronger dollar. Within EM, China continued to weigh on performance.