Rohan Reddy

Rohan ReddyIt’s no secret that Greek banks have been under pressure for the better part of a decade, contending with the effects of a deep economic recession as the country works through its excessive debts. While the Greek equity markets have managed to rally over 20% so far in 2017, returns for the nation’s banking sector are largely flat and have demonstrated intense volatility around news of potential asset quality reviews or stress tests.1

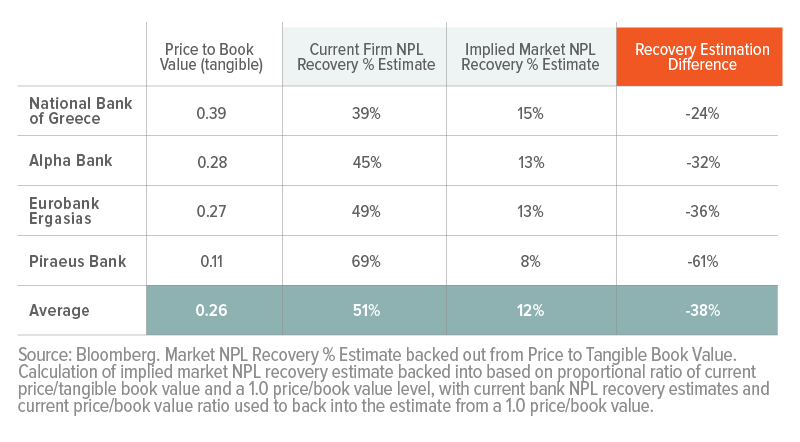

We believe this underperformance and bouts of volatility stems from the market’s intense scrutiny of Greek bank assets. Greek bank assets are particularly difficult to value given that they face significant non-performing loan (NPL) issues, meaning many loans are in default and the banks (and the market) are attempting to calculate how much they expect to recover of their principal. Based on how the banks are carrying these loans on their balance sheets, they believe they can recover on average just over half of the assets that they have designated as non-performing. But the banks currently trade at a 75% discount on average to their tangible book value, implying that the market predicts only a 12% recovery of these assets.2 Theoretically, if the market believed that the banks’ estimates of their assets and recovery levels were correct, the banks’ shares would trade close to their tangible book value.

The chart below shows the divergence between how various Greek banks are implying the recovery rate for the NPLs on their balance sheets, versus what the market is implying could be the recovery rate.

While this analysis is quite simple, as it assumes a bank’s assets are the only driver behind its share value, it can still give an idea of the differences between official bank expectations and the market’s opinion. If the market is correct about the lower NPL recovery levels and/or other assets that have not been designated as impaired, there could be potential negative downstream effects like another recapitalization that would dilute current shareholders. Other possibilities could include splitting bank assets into separate entities that hold either toxic or non-toxic assets. More regulatory oversight of banks could also result. If the banks are correct about their NPL recovery rates, it could signify a severe underpricing of Greek bank shares, meaning there is a major value opportunity in the sector.

Related ETFs

GREK: Global X MSCI Greece ETF invests in among the largest and most liquid companies in Greece.