In each of the past 15 years through 2024, an Emerging or Frontier Market has led global market performance.1 However, the asset class, as defined by traditional metrics, has underperformed the U.S. Fortunately, investors now have more sophisticated options on how to play the parts of the market they view as most attractive, while avoiding those they deem risky. Between equity, bonds, active, passive, thematic, and regional investment strategies – there are various ways to access the potential outsized growth at discounted valuations often sought in Emerging Market (EM) assets.

Looking into 2025, we have high conviction across key areas within EM, depending on the preferred style of the allocator. We strive to find bottom-up opportunities across different styles that span structural growth, momentum, value, income, contrarian, and thematic backdrops.

Key Takeaways

- U.S. interest rates, the strength of the U.S. dollar, and China typically combine to have an outsized impact on EM performance. Given recent trends across these three variables, the stars may once again be aligning for EM assets.

- We have high conviction on India and Argentina equities. Greece and Colombia could be attractive deep value plays, while Brazil and Chinese consumer names could appeal to contrarians. For those looking for income, we think EM dollar bonds stand out via yield, duration, and growth diversification opportunities.

- The Trump presidency creates uncertainty, but similar to 2016, the bark may be worse than the bite, and we think Trump administration policies could create tailwinds for Argentina, India, Greece, Eastern Europe, and Southeast Asia.

What Moves the Asset Class?

Three key factors drive broad EM performance: (1) U.S. interest rates (2) The strength of the U.S. dollar and (3) China. These factors drove the last EM upswing, when the MSCI Emerging Markets Index outperformed the S&P 500 Index 344.4% versus 15.07% between 2001 and 2010 (cumulative).2 Given the Fed has reached the middle of a cutting cycle, that the dollar could face mean reversion, and that China has begun implementing stimulus, there is an argument that the stars may once again align for EM assets.

When looking at the third driver, we note that China delivered a 19.70% return in 2024, allocators are just starting to begin looking again, and the MSCI China Index trades at 9.54x earnings.3 After years of successful export-based economic growth, we believe government officials are committed to pivoting towards consumption and technology. The highlights of recent Chinese Communist Party (CCP) meetings include stimulus and support around:

- Capital Markets: Outward solicitation from private sector opinions to boost equity market values, encourage M&A, improve governance and profitability goals, and create funds for both market stabilization and for share buybacks.

- Real Estate: Stabilization of the property market via lower mortgage rates, lower down payment requirements, funding banks helping with destocking, and longer credit duration.

- Monetary Policy: Plans to continue cutting interest rates and increasing liquidity

- Fiscal Policy: A higher fiscal deficit ratio and support to the consumer with examples such as (1) Subsidized trade-in programs for consumer goods and (2) Cash handouts to residents “facing hardship.”

- Debt: Refinancing for indebted local governments.

- Stimulus Language: In the December Politburo meeting, officials used the terms “moderately loose” around monetary policy and “more proactive” around fiscal policy. The former language has not been used since the 2008-2010 period and the latter had not been used since COVID-19. Additionally, we continue to hear that spending should focus on “people’s livelihoods and promoting consumption.”4

Standing Out in 2025

We have noticed a dramatic uptick in interest for EM assets. Many investors are coming from low to no positioning and are looking for differentiated ways to find exposure. Some are in search of a U.S. dollar hedge, many are looking for alpha potential, and others are simply looking for diversification. Looking into 2025, we highlight six opportunities.

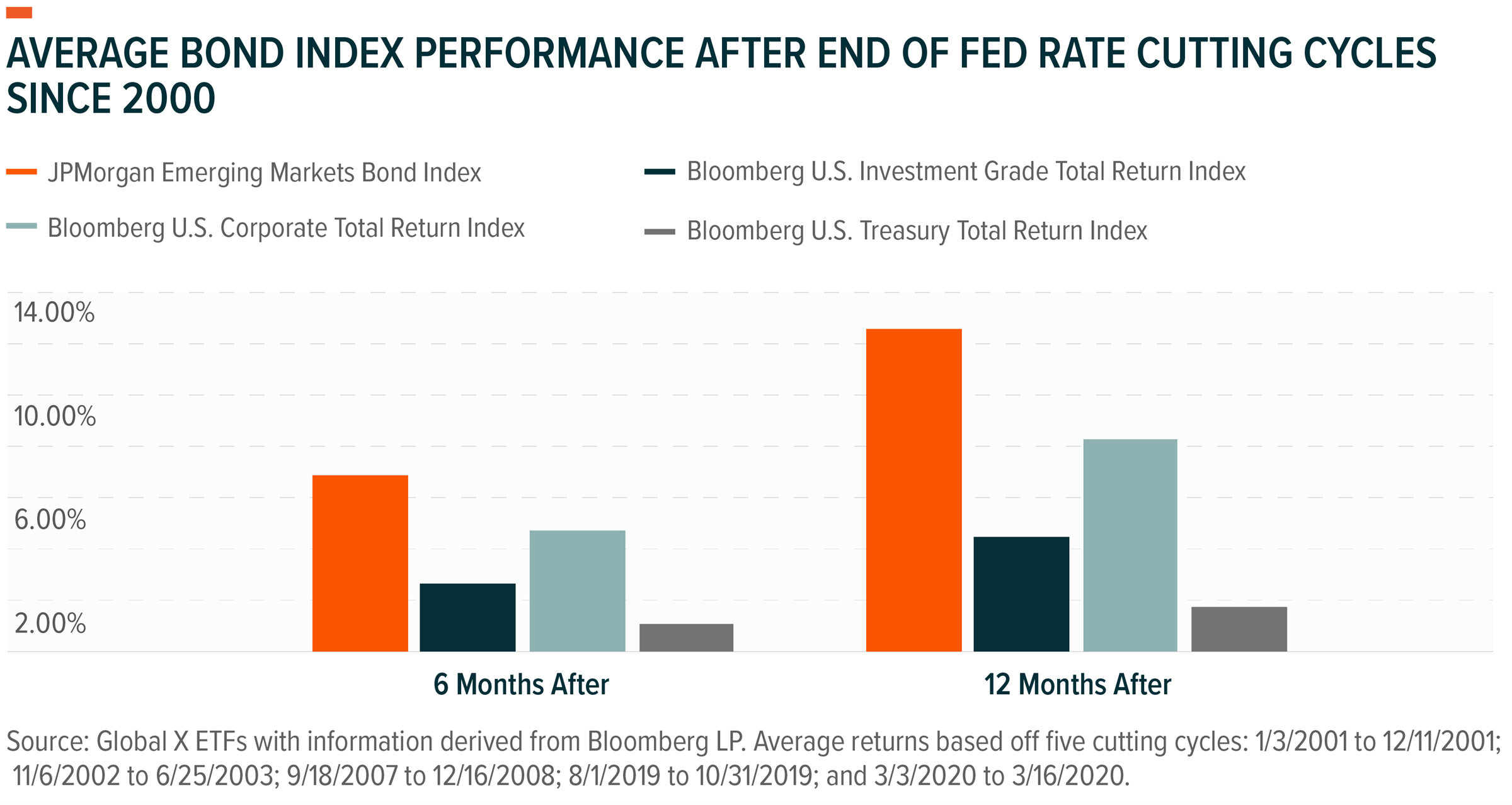

Income: Emerging Market Bonds

Emerging Market bonds offer exposure to the same dynamics as EM equities, typically with less China exposure, more yield, and less volatility. From a diversification perspective, they offer different duration, yield, and credit exposure than those found in standard domestic fixed income allocations. We believe the recent high-interest rate environment has largely washed-out weak issuers, and that EM bonds are in a healthier place than they’ve been since 2008. With a focus on relative value and downside protection, we prefer an active approach.

Structural Growth: India

Our recent due diligence trip to India convinced us the market is presenting a rare opportunity. It began in September when equities dipped on “fast money” taking profits and stepping into a bet on Chinese stimulus. The pullback continued with uncertainty around state elections and then saw incremental negativity on the third quarter’s 5.4% GDP growth figure.5 Although 5.4% isn’t the 6-7% investors have grown comfortable with, growing a 1.4-billion-person economy at 5.4% is still impressive. We think this quarter was one-off and continue to look for the next five years to produce roughly 6% GDP growth per year.

Assessing these recent factors, we believe India looks as attractive as ever.

- Any incremental China headwinds from the Trump administration could serve as a tailwind to the India story.

- Prime Minister Modi’s Bharatiya Janata Party (BJP) produced an impressive victory in the Maharashtra and Haryana elections, confirming a mandate of growth and continuity for the party that has helped lift roughly 250 million people into the middle class over the past decade.6

- In terms of the GDP print, it’s important to look at government spending. Contrary to the budget expectation for 17% growth, capex declined 15% in the first half of fiscal year 2025 (India’s fiscal year ends on March 31st).7 This means that capex must grow over 50% to meet the full-year target. This leads us to believe the government will meaningfully increase spending over the next six months.

Broadly speaking, we believe India is still a compounding machine, and we see the recent pullback as a unique opportunity to step-in with conviction.

Momentum: Argentina

Argentina has graduated from being our top contrarian idea last year to our top momentum play for 2025. Javier Milei’s first year (yes only one year so far!) has laid the foundation for sustainable growth. The fiscal adjustment has been the fastest and largest in Argentina in over three decades and has improved from a 4.9% of GDP deficit to a 0.5% surplus.8 Argentina’s eliminated its deficit for the first time in 123 years.9 The central bank cut interest rates from 133% to 32% as inflation has slowed to its slowest pace of monthly increases since July 2020.10 We could be in the early stages of unlocking Argentina’s economy. Potential 2025 catalysts could include fully liberalizing the currency, a new deal with the IMF, and potential consolidation of power for Milei in the midterm elections. Global bonds have gone from 30 cents on the dollar to 64, and the MSCI Argentina Index still trades at 0.91x book value.11

Value: Greece and Colombia

We see Greece and Colombia as unique pockets of deep value in EM. Despite geopolitical neutrality, the highest GDP growth rates in Western Europe, a market friendly government, and investment grade credit ratings, the MSCI Greece Index still trades below book value with a solid 7.48% dividend yield.12 The MSCI Colombia Index trades at depressed multiples of 0.84x book value with a 8.32% dividend yield.13 The market is pricing in market un-friendly reforms, but we believe that political gridlock and a path back towards the center – especially with 2026 elections just around the corner – should prevail. For those looking deeper into the weeds, we also see Colombia as the cleanest way to play potential political changes out of sanctioned Venezuela.

Contrarian: Chinese Consumer and Brazil

- China Consumer: We began 2024 suggesting investors follow the advice of Warren Buffett and "be greedy while others are fearful" and now remain selectively optimistic on segments of China’s equity market – specifically within Chinese consumption. We see Chinese consumption as clearly aligned with the interests of the CCP. Just in December we heard officials say that shifting policy focus to consumption to repair the economy would be a top priority.14 China doesn’t want to be the low-cost factory to the world anymore, government spending cannot last forever, and domestic consumption could serve as the future of Chinese economic growth. Within the consumer discretionary sector, one finds exposure to areas where China has competitive advantages, such as internet & artificial intelligence, electric vehicles, travel & hospitality, and more.15

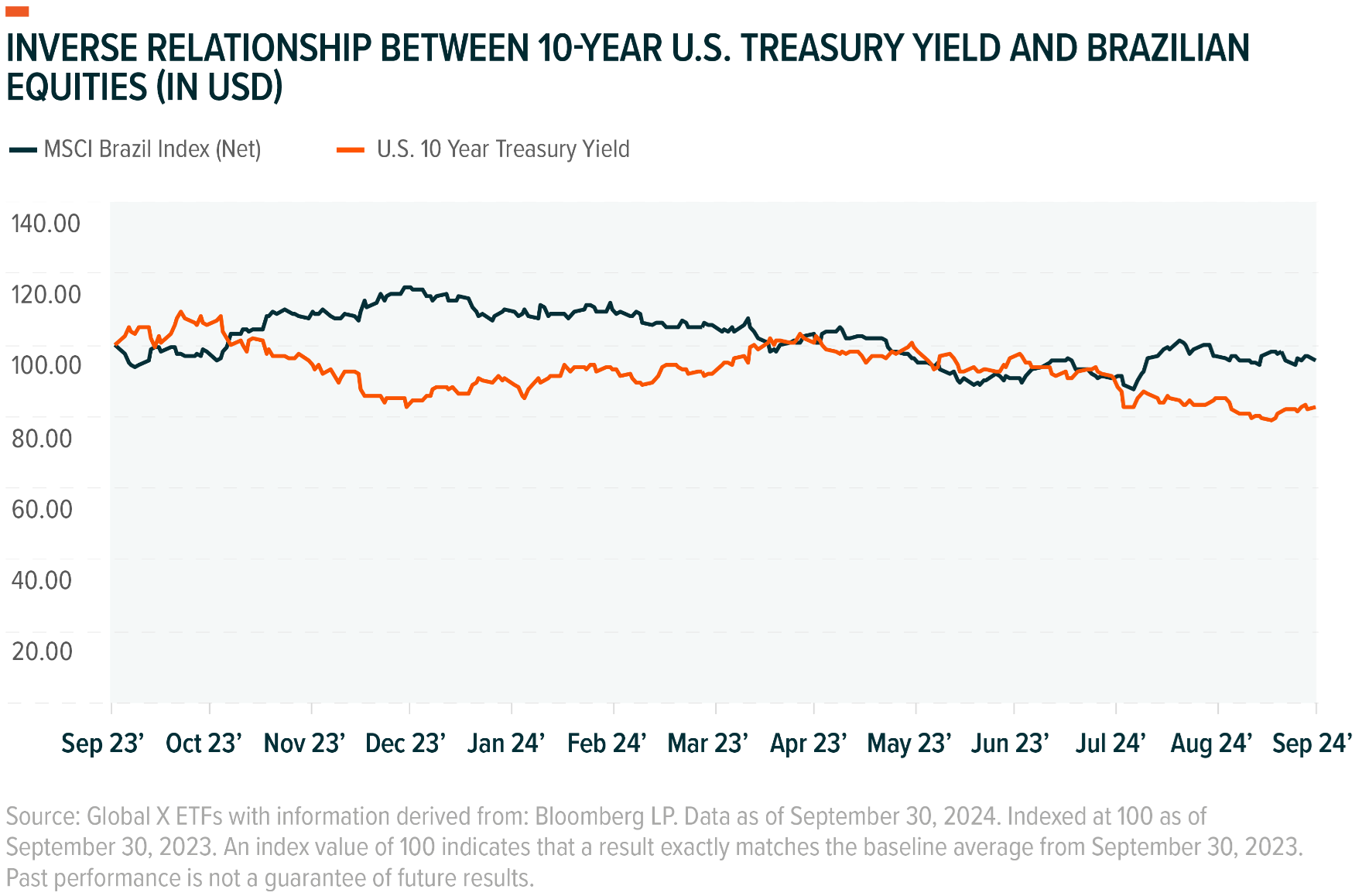

- Brazil: Brazil appears to have hit peak pessimism, which may set it up for a rally in the second half of 2025. Despite an attractive backdrop of low unemployment, mid-single-digit inflation, and better-than-expected GDP data, the executive branch continues to get in the way of the country's potential economic strength via a lack of fiscal orthodoxy. By not making progress towards a balanced budget, the government has put the onus on the Central Bank. We believe Brazil needs fiscal consolidation much more than monetary tightening, but the government has failed to deliver, which means the Central Bank has been forced to pick up the slack. This means higher interest rates, more capital moving from equities to bonds, and more redemptions in the local investment community. On the bright side, this could be creating a generational opportunity to buy high quality companies at distressed valuations. Interest rates will likely peak around 15% in 2025, just at the time when the market begins to focus on 2026 elections. It appears less likely that the current administration will stay in office, and the two other front-runners are centered politicians with more orthodox economic views and respect from the market. The combination of the above could unleash a violent rally and investors can be paid a healthy dividend to wait for it.

Thematic: Emerging Market Consumption

We see the long-term evolution of EM economies shifting from asset-heavy, low return exporters to asset-light, profitable, domestic providers of service & goods. History doesn’t repeat, but it often rhymes. The economic backdrop and post WWII “baby boom” led to a significant expansion of the U.S. middle class. The U.S. benefitted from 76.4 million baby boomers born from 1946 through 1964.16 Global X believes there will be various similar economic patterns across Emerging Markets, as roughly five billion people are expected to join the consumer class by 2031.17 This megatrend, along with the ability to minimize the unknown volatility around foreign exchange, commodity prices, and trade rhetoric, increases our optimism around domestic EM consumption.

What About Trump?

We’ll conclude this EM outlook with an overview on today’s most common question – “what will Trump 2.0 mean for EM?”. Similar to 2016, we believe the bark may be larger than the bite. In 2016, the S&P 500 Index outperformed the MSCI EM Index by 8.76% in the first two months following the election, but EM ended up rallying 29.01% over the 12 month period following the election versus 23.49% for the S&P.18 Trump’s playbook seems based on anchoring negotiations with large tariff-based threats (which we believe are currently priced into the market), and then ultimately meeting in the middle. We believe the current rhetoric on 60% tariffs for China and 25% for Mexico may follow the same pattern. From a country specific standpoint, we believe the Trump presidency will be positive for Argentina (potential IMF deal), India (relationship with Modi and stepping-in for Chinese manufacturing), Greece (helped by a strong U.S. consumer), Eastern Europe (prospects of a potential peace deal in Ukraine), and Southeast Asia (another China +1 beneficiary). On the negative side, we believe that Chinese exports (tariffs), Mexico (new terms to USMCA), and Saudi Arabia (lower energy prices) could face headwinds. Big picture, asset class movement will likely depend on the dollar. Though various election promises sounded inflationary, which could lead to a more conservative Fed, Trump has said he wants a weaker USD, and his initial spending plans show an increased fiscal deficit – which could imply mean reversion for the dollar and a tailwind for EM assets.19