Global X Research Team

Global X Research TeamBenchmark is a price data collection and assessment company specializing in the lithium ion battery supply chain. They offer price data, analysis and forecasting services for lithium ion cathode and anode raw materials particularly lithium, graphite, cobalt and nickel. The following is an excerpt from Benchmark’s Lithium Price Assessments – December 2017 Review.

Key Takeaways

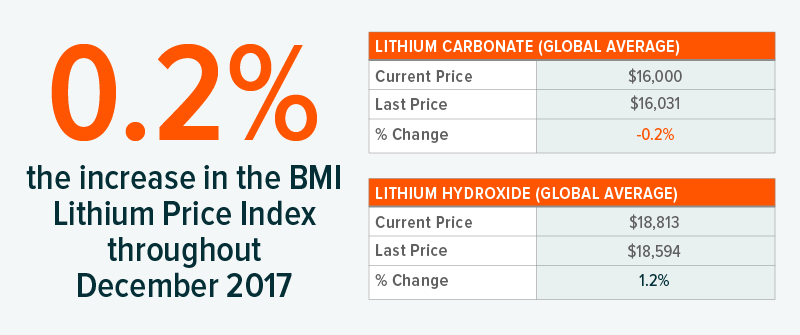

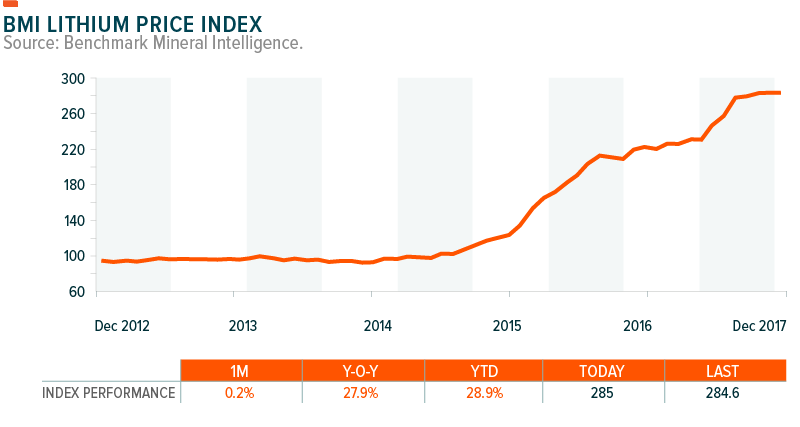

- Lithium prices stabilized in December despite end-market pressures; Benchmark Lithium Price Index finished year up 29%

- Outlook for lithium ion battery demand continues to strengthen with SK innovation announcing new 7.5 GWh plant in Europe; Chinese electric vehicle (EV) production up over 30% in November

- Piñera wins Chilean presidential election providing hopes of SQM1 resolution; company enters into conciliation process with state development agency, Corfo

- China extends EV subsidies out to 2020, increasing production outlook for 2018

Lithium Overview

Lithium demand projections continued to strengthen in December 2017 with new megafactory announcements and original equipment manufacturer (OEM) partnerships boosting the long-term outlook, and a rush on new energy vehicle production in China enhancing short-term prospects. In November 2017 China produced a record number of EVs – over 30% higher than any previous month on record – and the government’s decision to extend subsidies for another three years is expected to see further substantial production increases in 2018. Despite these pressures, lithium prices remained relatively stable throughout December due to the continued introduction of new supplies from Chinese conversion facilities.

The Chinese market, which has led the way in price rises over the past two years, stabilized somewhat as pressures eased on lithium carbonate supplies. Cost Insurance & Freight (CIF) prices for lithium carbonate into Asia subsequently fell by 1% over the month. With additional new feedstock supplies expected to reach the Chinese market throughout 2018, the ability of converters to ramp up battery-grade processing capacities will have a major bearing on prices entering the new year. In addition to the expected increase in supplies from Greenbushes, Mt Cattlin, Mt Marion and Wodgina in Western Australia, specialty mineral producer AMG NV announced plans to increase lithium concentrate supply from its Mibra Tantalum mine in Brazil.

With mechanical completion at the project due by April, the company is targeting first production by June 2018, ahead of a ramp-up towards a 90,000 tonnes per annum (tpa) capacity. The additional investment is aiming to take this to 180,000 tpa by 2019, the majority of which will be sold to an unnamed offtake partner. While new feedstock will see increased Chinese production, limited volumes will be exported meaning other countries targeting rapid expansions in lithium ion battery capacity will have to strengthen supply chains. Concerns over raw material dependence saw US President Trump sign an executive order in December aimed at reducing critical mineral reliance. This could have positive implications for new mining projects in the US.

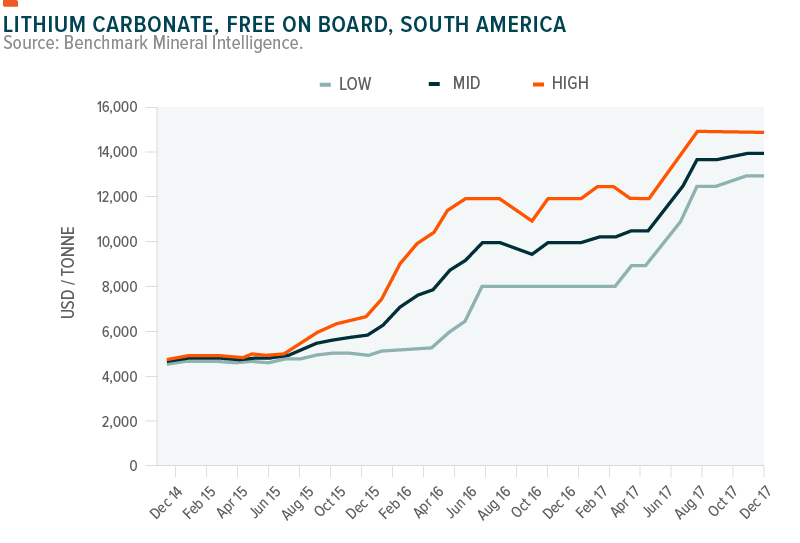

Lithium Carbonate

Following strong increases in lithium carbonate pricing in H2 2017 – driven by spot market transactions within China – the higher end of price ranges into Asia fell throughout December, seeing a marginal decrease in average price levels.

Benchmark’s Cost Insurance and Freight (CIF) Asia lithium carbonate price slipped to an average of $20,750/tonne in December, down from a peak of $21,500/tonne in October 2017 when the upper-end of the price range had reached $25,000/tonne.

Although an easing of pressures at the upper-end of price ranges saw a marginal decrease in average prices in Asia, prices into other regions which are typically agreed on a longer-term basis were robust as the gradual shift towards Asian price levels continued. The CIF price of lithium carbonate into North America climbed 0.8% on average in December, while Free On Board (FOB) prices out of South America were stable at $14,000/tonne.

Moving into 2018, increased volumes will be shipped at new contract rates which is expected to see prices into Europe and North America continue their trend towards the upper end of current price levels.

Lithium Carbonate, Free on Board, South America

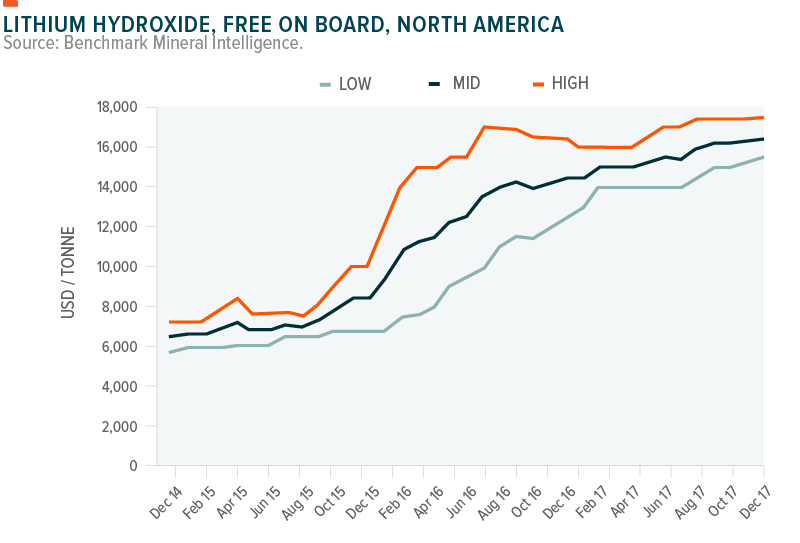

Lithium Hydroxide

The introduction of new lithium hydroxide supplies throughout H2 2017 failed to see a major decrease in price levels, particularly in the Asia market where there were marginal gains in prices throughout December.

Ex Works (EXW) China prices climbed 2% while average CIF prices into Asia were up just over 1%, finishing the year $20,500/tonne, their highest point since September.

While sales at significant premiums have been less frequent in 2017 – limiting the higher-end of price ranges – new longer-term agreements have been agreed at slight increases throughout the year, seeing few low price transactions.

With robust prices into Asian consumers, North American suppliers have gradually increased their offers and increased inquiries approaching the end of the year saw a 0.8% increase in average FOB prices out of the region.

Based on our analysis and expectations, new feedstock supplies into Chinese conversion facilities could see hydroxide prices settle at a slightly lower levels in 2018, however the slowdown in Chinese production approaching the country’s Spring Festival is likely to see robust pricing in Q1.

Lithium Hydroxide, Free on Board, North America

Supply

Feedstock: Prospects for new feedstock supplies were strengthened once more in December with the news that AMG NV was looking to double lithium concentrate production from its Mibra mine in Brazil by 2019. The company is targeting first production from its new 90,000 tpa lithium facility by June 2018, with concentrate volumes destined for an unnamed offtake partner. Elsewhere, Pilbara Minerals2 signed another offtake agreement for the sale Direct Ship Lithium Ore (DSO) to Australian iron ore company Atlas Iron Ltd, with the subsequent concentrate expected to be sold into the Chinese market.

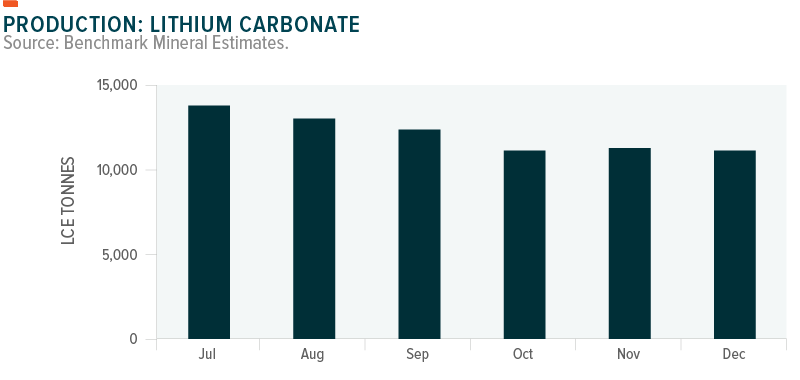

Carbonate: Lithium carbonate production is estimated to have fallen marginally in December with slower production rates in China and Chile. Increased feedstock supplies into Chinese conversion facilities throughout 2017 have seen a gradual increase in chemical output, however not all of this new raw material has yet been converted. With new raw material supplies expected to emerge through 2018, there is the potential for a shortfall in battery grade carbonate production, particularly with the growing trend towards NCM cathode technologies which is likely to continue into the new year.

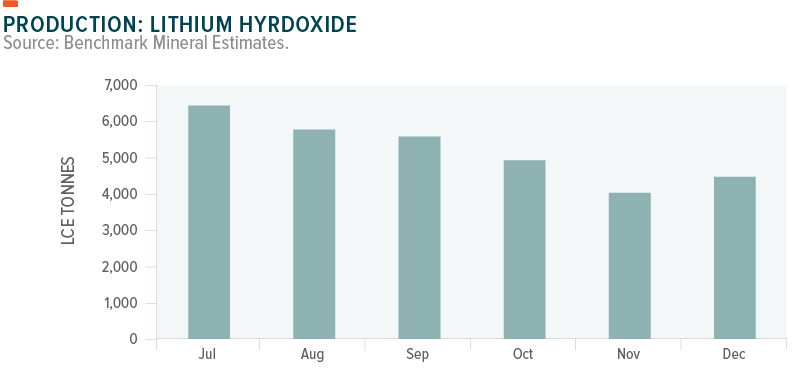

Hydroxide: Lithium hydroxide production is estimated to have risen marginally in December with increased conversion volumes being reported out of China. While the country remains the primary lithium hydroxide producer and is expected to further increase production in 2018, industry majors outside of China are also targeting increased output by the end of 2018. Initial production from Tianqi Lithium’s Kwinana facility is scheduled for late-2018 while SQM is aiming to more than double production from Antofagasta by the same time. While this increases long-term supply prospects, conversion capacity will continue to hinge on the ability of Chinese processors to produce significantly larger volumes of battery-grade hydroxide from the new spodumene feedstocks.

For more information on Benchmark Price Assessments please contact Andrew Miller – amiller@benchmarkminerals.com

For more holdings information on the Global X Lithium & Battery Tech ETF (LIT), please visit: www.globalxetfs.com/funds/lit. Holdings subject to change.