Global X Research Team

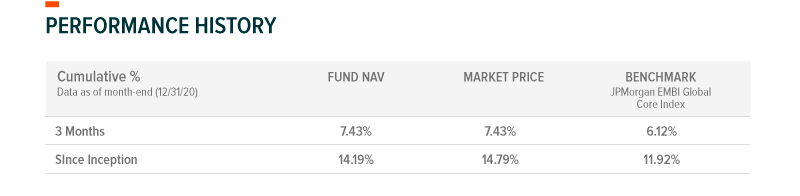

Global X Research TeamFor the period September 30, 2020 to December 31, 2020, the Global X Emerging Market Bond ETF (EMBD), sub-advised and actively managed by Mirae Asset Global Investments (USA) LLC, returned +7.43% including dividends. This compares to a return of +6.12% for the JP Morgan EMBI Global Core Index, the fund’s benchmark, over the same period. The index tracks liquid, US dollar emerging market (EM) fixed and floating-rate debt instruments issued by sovereign and quasi-sovereign entities.

The performance data quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance data current to the most recent month end, please click here

Cumulative return is the aggregate amount that an investment has gained or lost over time. Annualized return is the average return gained or lost by an investment each year over a given time period.

General Market Review

Global growth continued to recover from the second quarter lows on the back of large monetary and fiscal stimulus. Risk sentiments got a boost during the fourth quarter from the promising news of vaccine developments. The prospects for less disruptive trade policy by the incoming Biden administration should help support global trade flows, which would likely boost higher risk asset prices, including emerging markets. Even as the concerns over a second wave of coronavirus infections rose, investors appeared focused on the economic normalization prospects in the coming year with the vaccine rollout. The negative developments from the second wave of infections seemed to give rise to positive market responses for risk assets, as investors priced the prospects of additional fiscal stimulus measures and the extended supports from the Fed.

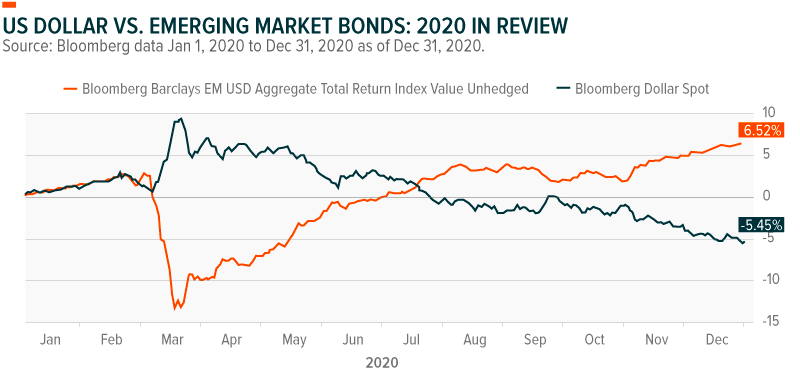

During the fourth quarter, emerging asset prices performed well as the commodity prices continued to rise from increased demand from China. China was the only major economy that managed to grow GDP in 2020 with the economy expanding +2.1% as policymakers successfully flattened the infection curve, which helped support the service sector during the second half of the year. Weaker dollar trends helped ease financial conditions for emerging markets, reversing investors’ earlier flight-to-quality flows. As a result, investors ended 2020 with very bullish sentiments.

The performance data quoted represents past performance and does not guarantee future results.

During the period, the emerging sovereign debt market posted a gain of +6.12% as the credit spread narrowed by -81 basis points to 352 basis points; the emerging corporate bond market posted a gain of +4.29%. The investment-grade sector, up +2.96%, underperformed the high yield sector, up +9.33%, as lower quality African issuers led a strong recovery in the fourth quarter driven by positive risk sentiments and investors’ search for higher yielding assets on the back of strong inflows into emerging debt markets. However, restructured debt issued by Argentina and Ecuador continued to perform poorly in the fourth quarter with losses of -2.83% and -2.39%, respectively. Investors remained cautious due to the lack of economic reform measures and political uncertainty, especially as Ecuador faces a presidential election in early February. During the period, the worst-performing country was Sri Lanka reporting a loss of -13.12% after all three rating agencies downgraded it to CCC level as fundamentals continued to deteriorate. The best performing country was CCC rated Angola with a gain of +22.49% as investors digested the positive news that Angola secured debt reliefs from Chinese lenders and the IMF providing debt relief for the next three years. The emerging debt markets ended 2020 strong as the global recovery theme gained traction with promising vaccine developments and strong inflows into the asset class as investors searched for yielding assets.

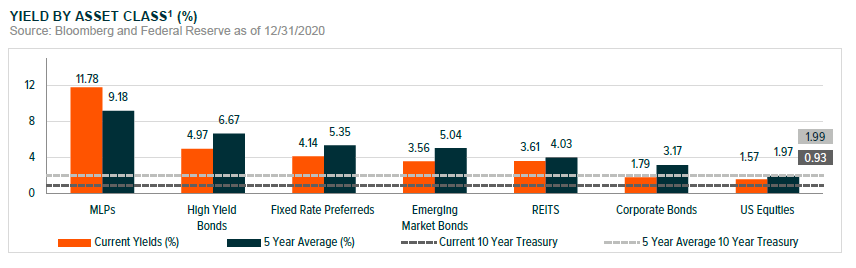

Note: Asset class representations are as follows, MLPs, S&P MLP Index; High Yield Bonds, Bloomberg Barclays US Corporate High Yield Total Return Index; Emerging Market (EM) Bonds, Bloomberg Barclays EM USD Aggregate Total Return Index; Corporate Bonds, Bloomberg Barclays US Corporate Total Return Index; REITs, FTSE NAREIT All Equity REITS Index; Equities, S&P 500 Index; and Preferreds, BofA Merrill Lynch Fixed Rate Preferred Securities Index. The performance data quoted represents past performance and does not guarantee future results.

EMBD Portfolio Attribution

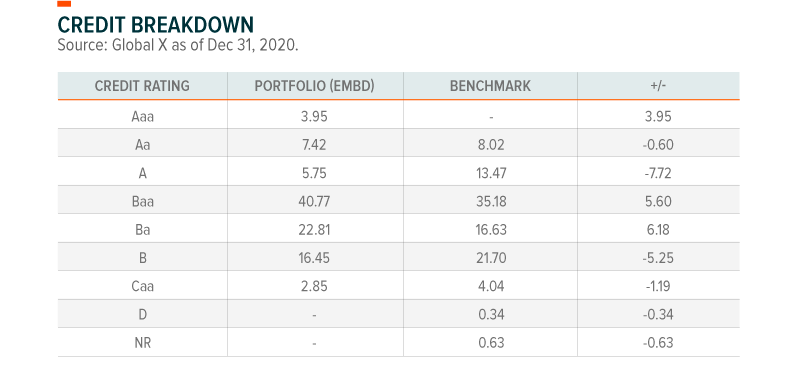

During Q4 2020, the Fund outperformed the Index by +131 basis points with positive contributions from both country allocations, which contributed +33 basis points, and security selections, contributing +85 basis points. We entered the fourth quarter with a cautious stance due to the growing risks of a second wave of coronavirus infections. However, when the prospects for vaccine approvals and distribution gained traction, we were able to quickly pivot to a more bullish stance by increasing the Fund’s credit risk profile. The Fund capitalized on the vaccine rollout theme by taking a new position in the Bahamas during the period. Given that the Bahamas’ economic recovery is highly sensitive to the tourism industry, the news of vaccine developments led to strong performance for Bahama bonds. From a country allocation perspective, the Fund’s underweights to China and Sri Lanka positively contributed +26 and +24 basis points, respectively, as we acted to reduce the Fund’s exposure to certain Chinese issuers when US sanctions were first revealed in the media and maintained underweight positions in Sri Lanka. The Fund’s security selections in corporate issuers contributed positively to performance with Brazil’s pulp and paper producers, Suzano and Klabin, and UAE’s DP World as key contributors. The main detractor from performance was the Fund’s underweight to Angola and some high yielding issuers such as Ghana and Kenya. The Fund’s underweight to the Dominican Republic also had a negative contribution to the performance. As the valuation for higher quality issuers such as Malaysia and the Philippines became more expensive, the Fund reduced exposure to those countries while increasing the allocation to corporate issuers in the commodity sector in the Latin America region. During the period, the Fund reduced the duration risk relative to the benchmark as the prospects for higher core rates increased in 2021 with economic normalization.

Outlook & Strategy

As we move into 2021, we expect risk sentiment to maintain a constructive tone driven by continued global growth recovery with the vaccine rollout and supportive fiscal and monetary policy measures. We expect investors who held capital on the sidelines over concerns of a potential double-dip recession in the US will increasingly look for income-generating assets as the Fed’s zero interest rate policy for the next couple of years will erode the purchasing power of money. We believe that emerging market assets will be a main beneficiary of this macro trend. That being said, the valuations for the emerging debt markets are leaning expensive, especially for the high quality investment grade sector. The investment grade sector’s credit spread has reverted to pre-Covid-19 levels leaving little room for spread compression if core rates rise in 2021.

Given the positive macro backdrop, we expect core rates to gradually move higher from 2020 levels as economies normalize and a higher supply of government bonds to finance fiscal stimulus policies negatively impacts short term technicals. Therefore, we favor high yielding assets over the investment grade sector. We also look to reduce the Fund’s overall interest rate risk exposure, especially longer maturity debt. We favor high yielding quasi-governmental issuers such as Mexico’s oil and gas producer, and a government-owned airport operator in Panama. We continue to like Mexican industrials that will benefit from a strong US economic recovery for our emerging corporate strategy. We still do not find Turkish corporate and banks attractive for investment, as they trade inside the sovereign issuer’s credit spread. Even as the global growth outlook improves, we expect an uneven recovery across regions, making an active strategy particularly relevant in navigating these volatile markets.

Holdings subject to change. Current and future holdings subject to risk.

Definitions

S&P MLP Index provides investors with exposure to the leading partnerships that trade on the NYSE and NASDAQ. The index includes both master limited partnerships (MLPs) and publicly traded limited liability companies (LLCs), which have a similar legal structure to MLPs and share the same tax benefits.

Bloomberg Barclays US Corporate High Yield Total Return Index measures the USD-denominated, high yield, fixed-rate corporate bond market.

Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

Bloomberg Barclays EM USD Aggregate Total Return Index is a flagship hard currency Emerging Markets debt benchmark that includes fixed and floating-rate USD dollar-denominated debt issued from sovereign, quasi-sovereign, and corporate EM issuers.

FTSE NAREIT All Equity REITS Index is a free float adjusted market capitalization weighted index that includes all tax qualified equity REITs listed in the NYSE, AMEX, and NASDAQ National Market.

The Bloomberg Barclays US Corporate Total Return Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD denominated securities publicly issued by US and non-US industrial, utility and financial issuers.

MSCI USA High Dividend Yield Index is based on the MSCI USA Index, its parent index, and includes large and mid cap stocks. The index is designed to reflect the performance of equities in the parent index (excluding REITs) with higher dividend income and quality characteristics than average dividend yields that are both sustainable and persistent. The index also applies quality screens and reviews 12-month past performance to omit stocks with potentially deteriorating fundamentals that could force them to cut or reduce dividends.

S&P 500 Index tracks the performance of 500 leading U.S. stocks and captures approximately 80% coverage of available U.S. market capitalization. It is widely regarded as the best single gauge of large-cap U.S. equities.

BofA Merrill Lynch Fixed Rate Preferred Securities Index tracks the performance of fixed-rate U.S. dollar denominated preferred securities issued in the U.S. domestic market.

MSCI ACWI Index captures large and mid cap representation across 23 Developed Markets (DM) and 24 Emerging Markets (EM) countries. The index covers approximately 85% of the global investable equity opportunity set. DM countries include: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the UK and the US. EM countries include: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Pakistan, Peru, Philippines, Poland, Russia, Qatar, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates.

The Bloomberg Barclays US Treasury: 7-10 Year Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury with 7-9.9999 years to maturity.

The Bloomberg Barclays EM USD Aggregate Total Return Index Value Unhedged is a debt benchmark that includes USD-denominated debt from sovereign, quasi-sovereign, and corporate EM issuers.

Bloomberg Dollar Spot Index tracks the performance of a basket of ten leading global currencies versus the U.S. Dollar. Each currency in the basket and their weight is determined annually based on their share of international trade and FX liquidity. The BBDXY Index data starts from Dec 31, 2004 with a base level of 1000.

Credit Rating Agencies noted are Fitch, Moody’s, and Standard & Poor’s. Ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest).

Related ETFs

EMBD: The Global X Emerging Markets Bond ETF is an actively managed fund sub-advised by Mirae Asset Global Investments that seeks a high level of total return, consisting of both income and capital appreciation, by investing in emerging market debt.