Global X Research Team

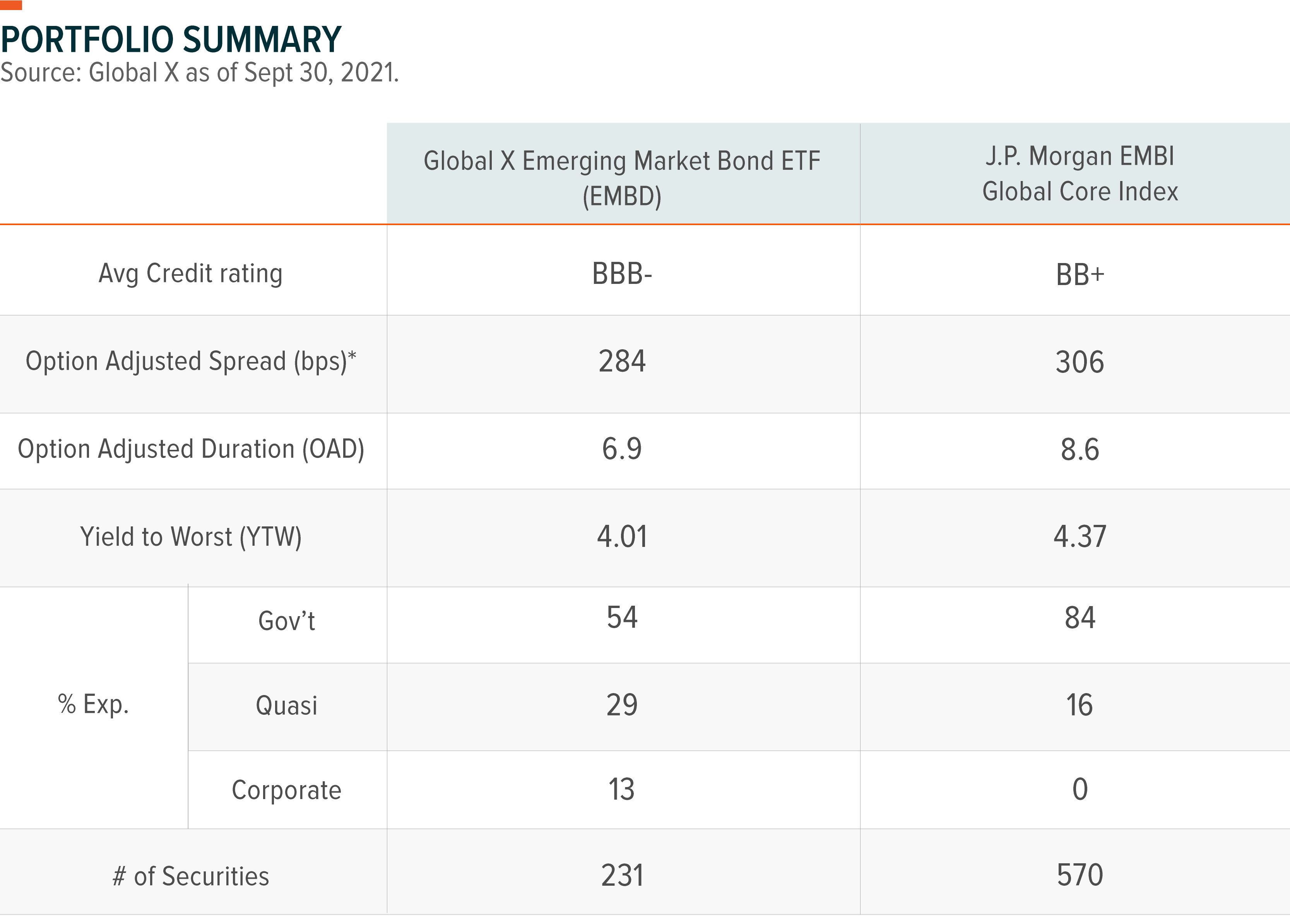

Global X Research TeamDuring Q3 2021, the Global X Emerging Markets Bond ETF (EMBD) sub-advised and actively managed by Mirae Asset Global Investments (USA) LLC, recorded a total return of -0.56%. Despite the loss, this compares favorably to the -0.82% returns for the fund’s benchmark, JP Morgan EMBI Global Core Index, over the same period. The benchmark index tracks liquid, US dollar emerging market (EM) fixed and floating-rate debt instruments issued by sovereign and quasi-sovereign entities.

The performance data quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance data current to the most recent month end, please click here. Total expense ratio: 0.39%.

Cumulative return is the aggregate amount that an investment has gained or lost over time.

General Market Review

The lackluster performance for Q3 can be explained by a broad range of cross-currents in the market, which made it challenging for market participants to make directional conviction calls. One segment of both the equity and fixed income markets that attracted significant attention were energy-related and inflation-linked assets. Even as global central banks were persistent with the “base-effect” and then the “transitory” narratives for rising inflation, it became clearer that inflationary pressures would persist for longer than expected based on economic data. This belief led investors to seek assets that offered potential protection against inflation, leading them to energy-related assets.

From a global growth perspective, there were continuous downward revisions as (1) supply-chain bottlenecks lasted longer than expected, (2) China’s regulatory and market turmoil across sectors like Consumer Discretionary, Communications Services, and Real Estate, (3) US Congress’s lack of progress on the Biden administration’s economic agenda, and (4) the power shortage crisis in China/Europe threatening industrial activities and consumer spending. Even with this backdrop of adverse developments, the market was not yet ready to rotate out of risk assets and into cash-like instruments. The global equity market attracted over $177 billion of inflows, while money market funds attracted only $11 billion during the quarter. It was evident that the expansionary monetary policy, which injected over $200 billion per month of liquidity into the financial market system, played a key role in investors’ decision-making process.

Even as the growth projections were revised downwards, some market participants remained hopeful for the “return of reflation” investment narrative given (1) there are still massive household savings and pent-up demand for goods and services once Covid-19 concerns subside, (2) a healthy household balance sheet that can take on more leverage with improving employment markets, (3) higher industrial activities as companies return to more normal inventory levels, and (4) an expected surge in global corporate capital expenditure with ample cash on corporate balance sheets.

However, the most relevant driver for changes in the investment atmosphere had to be the explicit policy shift in the global monetary policy regime. We believe the Fed’s decision to shift its policy stance to becoming more hawkish came not from market pressures, but rather from the survey results of the consumer inflation expectations. As the consumer inflation expectation rose to levels last seen just before the Great Financial Crisis (GFC), we believe the Fed grew concerned about de-anchoring inflation expectations in the household sector. Therefore, the Fed decided to make policy shifts more explicit than what the market broadly anticipated. In conclusion, these cross-currents in the market led to mixed results for financial markets during the period.

Even as pandemic-related disruptions and vaccination distribution in EM improved, Q3 was a particularly challenging period for emerging market investors to navigate. First, ongoing negative developments stemming from China’s President Xi Jinping’s new “common prosperity” mantra extended from internet to education industries and then to the economically sensitive Real Estate sector. Second, the surge in global energy and food prices will likely impact EM economies more than developed market (DM) economies due to EM’s transmission mechanism, which forced EM central banks to aggressively push for policy normalization. Last but not least, the Fed’s shift towards more hawkish monetary policy to re-anchor inflation expectations negatively impacted investors’ appetite for EM risk assets.

The EM sovereign debt market posted a loss of -0.80% during the period while the emerging corporate debt sector returned -0.06%. Weaker spread returns led by the single B ratings sector – which widened by 52 basis points – caused the high-yield sector to underperform the investment-grade sector. Interestingly, distressed and defaulted sovereigns, like Lebanon +32.7%, Belize +26.3%, Zambia +21.6%), were among the best performing sectors as positive developments related to negotiations with creditors and the IMF generated positive sentiment. On the other hand, El Salvador, which became the first country to adopt bitcoin as legal tender, was the worst performing sovereign down -16.5%. Investors believed an IMF deal is unlikely given the IMF’s warning against using bitcoin as legal tender. In general, sovereign issuers with weaker external balance positions, such as Egypt (-3.7%) and Ghana (-5.4%), performed poorly. In contrast, issuers with less liquidity, but lower supply risks, such as Argentina (+3.4%) and Cameroon (+7.1%), performed better. One notable outlier was Colombia sovereign debt, which fell -4.6%. Even as oil prices climbed back towards $80/barrel, the Fitch rating agency followed through with a downgrade decision in July, causing forced-selling among investment grade mandated investors.

The emerging corporate debt market, which outperformed the sovereign debt market, suffered from negative developments in China’s property market as it appeared that the Chinese government was unlikely to bail out China’s largest private property developer, Evergrande. What was surprising for investors was neither how precarious Evergrande’s liquidity conditions were, nor the implementation of regulatory constraints, as this information was well reported. Rather, what surprised investors was a lack of reaction from the Chinese government, since a property market downturn could have significant spillover effects on the broader Chinese economy. As a result, the Chinese high yield dollar market fell -9.5% during the period. However, there was no contagion effect on the broader emerging corporate debt market from the Evergrande crisis as Asia local investors held most high yielding Chinese property developers. Latin America corporate issuers which could be negatively impacted by a broader slowdown in China, held up well during the period gaining +0.5% as these issuers were recovering from idiosyncratic shocks from Q2.

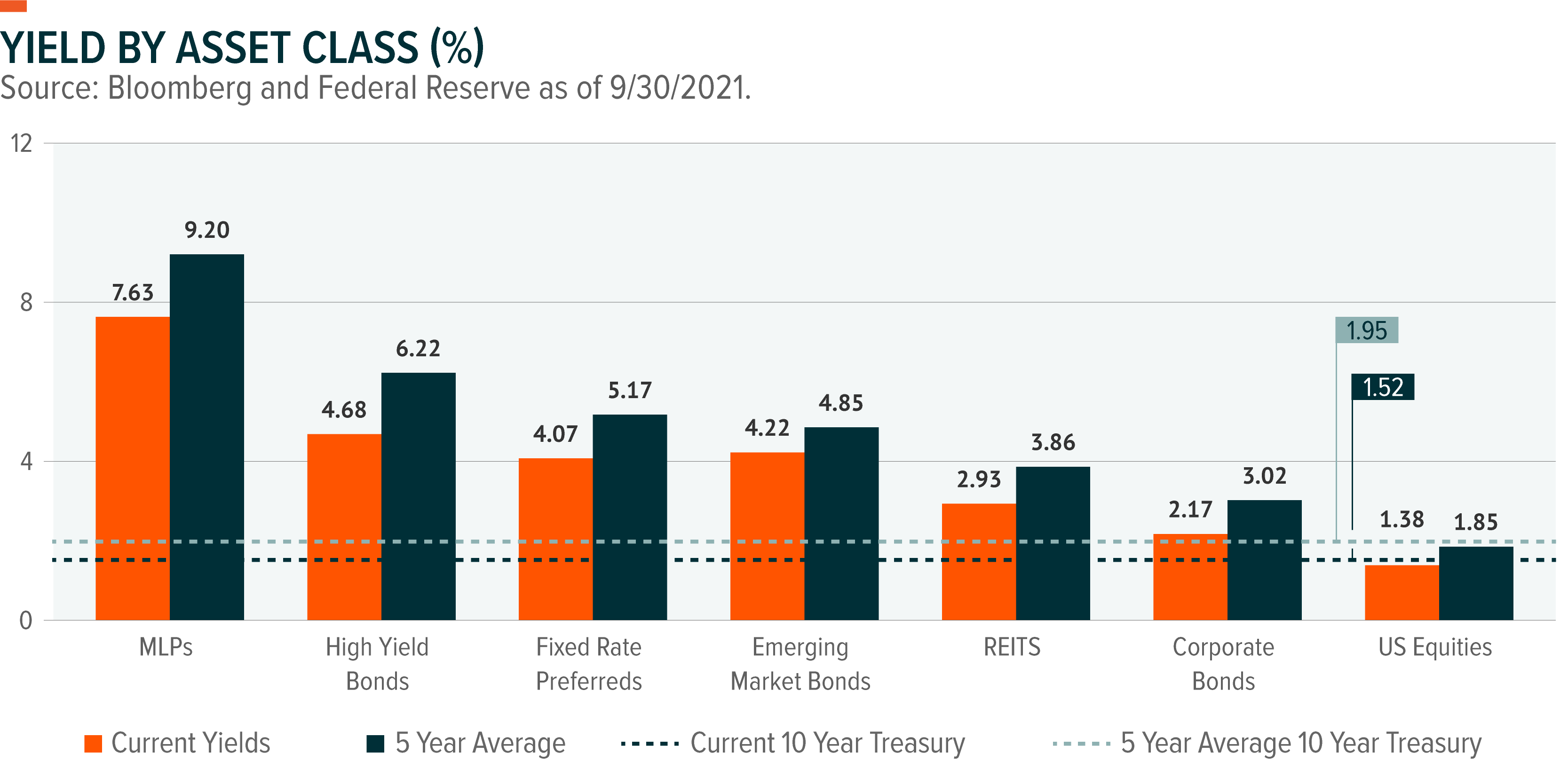

Note: Asset class representations are as follows, MLPs, S&P MLP Index; High Yield Bonds, Bloomberg US Corporate High Yield Total Return Index; Emerging Market (EM) Bonds, Bloomberg EM USD Aggregate Total Return Index; Corporate Bonds, Bloomberg US Corporate Total Return Index; REITs, FTSE NAREIT All Equity REITS Index; Equities, S&P 500 Index; and Fixed Rate Preferreds, ICE BofA Merrill Lynch Fixed Rate Preferred Securities Index. The performance data quoted represents past performance and does not guarantee future results.

EMBD Portfolio Attribution

During the period, EMBD outperformed its benchmark index by 26 basis points. EMBD’s lower duration relative to the index was a main detractor to performance (-21 basis points) offset by positive contributions from security selections (+64 basis points). Heading into Q3, EMBD’s portfolio managers maintained their underweight duration exposure, while tilting the portfolio to pro-cyclical and higher growth sensitive issuers in high yielding sectors. They also entered tactical long positions in idiosyncratic names such as Peru and Colombia via corporate issuers.

High beta long exposures in pro-cyclical sovereigns such as Egypt detracted from performance. Egypt continued to surprise investors with a willingness to tap the market to support expansionary fiscal policy, which spurred investors to question Egypt’s growing debt sustainability. Furthermore, a long position in Colombia negatively contributed to the performance as the portfolio managers’ decision to build a long position soon after S&P downgrade proved too early. Additionally, underweight positions in distressed and defaulted sovereigns such as Lebanon and Zambia detracted from performance. On the other hand, security selections in the Latin American region via corporate issuers contributed 34 basis points to performance. EMBD did not have any exposure to Chinese property developers during the period as there were too many uncertainties related to regulations to enter any positions.

Q4 Outlook & Positioning

We expect the investment narrative of “stagflation,” which was the dominant theme in Q3, to evolve to “stabilizing growth, but higher inflation” in Q4. Declining global growth momentum is expected to stabilize as economies re-open again alongside a decline in Covid-19 Delta variant cases. We expect the key driver for growth pressures to come initially from consumer spending and then corporate expenditure programs. Improving labor market conditions and cleaner balance sheets will likely support US households to spend more this holiday season. Also, the global supply bottlenecks that were a drag on growth momentum during Q2-Q3 are expected to improve in Q4 supporting the growth outlook. That being said, it is inevitable that the power crisis and the debacle of property developers in China will have a negative spillover impact on the broader Chinese economy and global demand in the coming months. Our main investment thesis is that the China-driven slowdown will start to effect global growth momentum early-to-mid next year as opposed to Q4.

The recent surge in global energy prices will likely feed into higher production prices and increase the risks of de-anchoring inflation expectations in an environment where aggregate demand impulse remains strong. Therefore, we expect the Fed to proceed with a liquidity withdrawal starting with tapering in December 2021 and signaling that the tapering will be on autopilot until it expires in mid-2022. We think this sort of exit program will be very aggressive and it risks disrupting global recovery progress in 2022. However, our view is that initially, risk assets will not respond negatively to a hawkish Fed given that the growth momentum will be recovering from the Q3 pullback. Consequently, we anticipate that risk assets will move sideways during the period with sectoral rotation being the key source of market attention. We are looking for higher rates into the year-end, especially when US Congress’s short-term debt ceiling agreement results in a treasury supply of $480 billion in the next month and half.

Even as global growth momentum stabilizes, the expectation of tighter DM monetary policy will be a major headwind for EM assets. However, the key question will be whether the financial liquidity condition will be tight simply on the expectation of tighter Fed monetary policy or whether the market will realize that an additional $1 trillion of liquidity will be injected into the system until the Fed ceases the tapering program. Our view is that EM assets will face an initial shock when the Fed announces the tapering program, but will stabilize once investors realize that the market is still awash with liquidity.

We expect the 10-year Treasury yield to move gradually higher, helped by a rise in real yields. However, the speed at which government yield increases will be a much more measured pace than what the market observed in Q1, given that the market will only tolerate higher yields to the extent that the global growth momentum stabilizes.

Even though we are past the peak liquidity cycle, driven by the additional $1 trillion of reserves pumped into the financial system, we expect the abundant liquidity in the financial system to support growth and carry assets. As a result, we expect investors to consider EM credit assets which should benefit from the global recovery (i.e. rising commodity prices), while offering carry income in a rising volatile rate environment.

We maintain our view that global bond yields will move higher in the second half of the year, with EM credit spreads absorbing much of the rate movements. Therefore, we favor high-yielding assets over the investment-grade sector, given that there are more spread buffers to absorb in the high-yield sovereign bonds. That said, we believe credit differentiation driven by sovereigns with healthy external balance sheets will be the major theme for EM assets as the Fed withdraws liquidity supports from the system. We find the EM corporate sector offers attractive investment opportunities as corporate fundamentals continue to improve with the global recovery while management teams have maintained a conservative strategy to strengthen balance sheets. Also, we find particular corporate issuers such as Colombia utilities and Peru corporates attractively priced as the sovereign downgrade (i.e. Colombia) and political instability (i.e. Peru) put pressure on corporate issuers. We anticipate that market volatility will remain elevated as the Fed’s tapering discussions, Covid-19 variant concerns, and the Biden administration’s infrastructure plan may alter either growth trajectory or policy directions.