As the 21st century nears its quarter mark, one lesson that we subscribe to is that the U.S. economy and markets are typically resilient. Want proof? The Dot-Com Bubble, the Global Financial Crisis, and COVID-19 have all occurred since the turn of the century—and yet, the S&P 500 has quadrupled.1 We remember that lesson as we find a blend of optimism and uncertainty entering 2025. Investor sentiment and consumer expectations are improving, while questions abound about economic policy and GDP growth is forecast to slow.

Like last year, we believe that economic growth is likely to surprise on the upside and markets can continue to trend higher. What’s different may be the growth drivers. Some market participants posit that equity valuations on broad indexes seem stretched, but in our view, flows suggest investors are ready to embrace risk-on assets. Better market breadth, further profit margin improvement, and continued earnings growth could help lift equity valuations further. By contrast, fixed income may be stuck in limbo given the potential for interest rate volatility, possibly requiring investors to get more creative and look for differentiated strategies.

For the second year in a row, the U.S. economy did better than consensus expectations. Forecasts called for real GDP growth of 0.5–1.5% at the start of 2024, with the thesis being that an overstretched consumer and a consumption pullback would cause companies to curb investment.2 Neither happened, for the most part, and the economy averaged 2.5% real quarterly growth through Q3 2024.3 The consumer remained resilient, despite the end of COVID stimulus, and consumption grew by 3.5% in Q3, up from 2.5% in the prior year.4

A strong labor market and services sector expansion supported consumption. While unemployment moved higher, from 3.4% to 4.1%, layoffs were contained.5 Companies continued to hire, consumers continued to spend on services, and inflation in areas like travel and restaurants proved sticky compared to other areas.6 The services sector strength was important, as manufacturing employment and production remained in contraction for most of 2024.

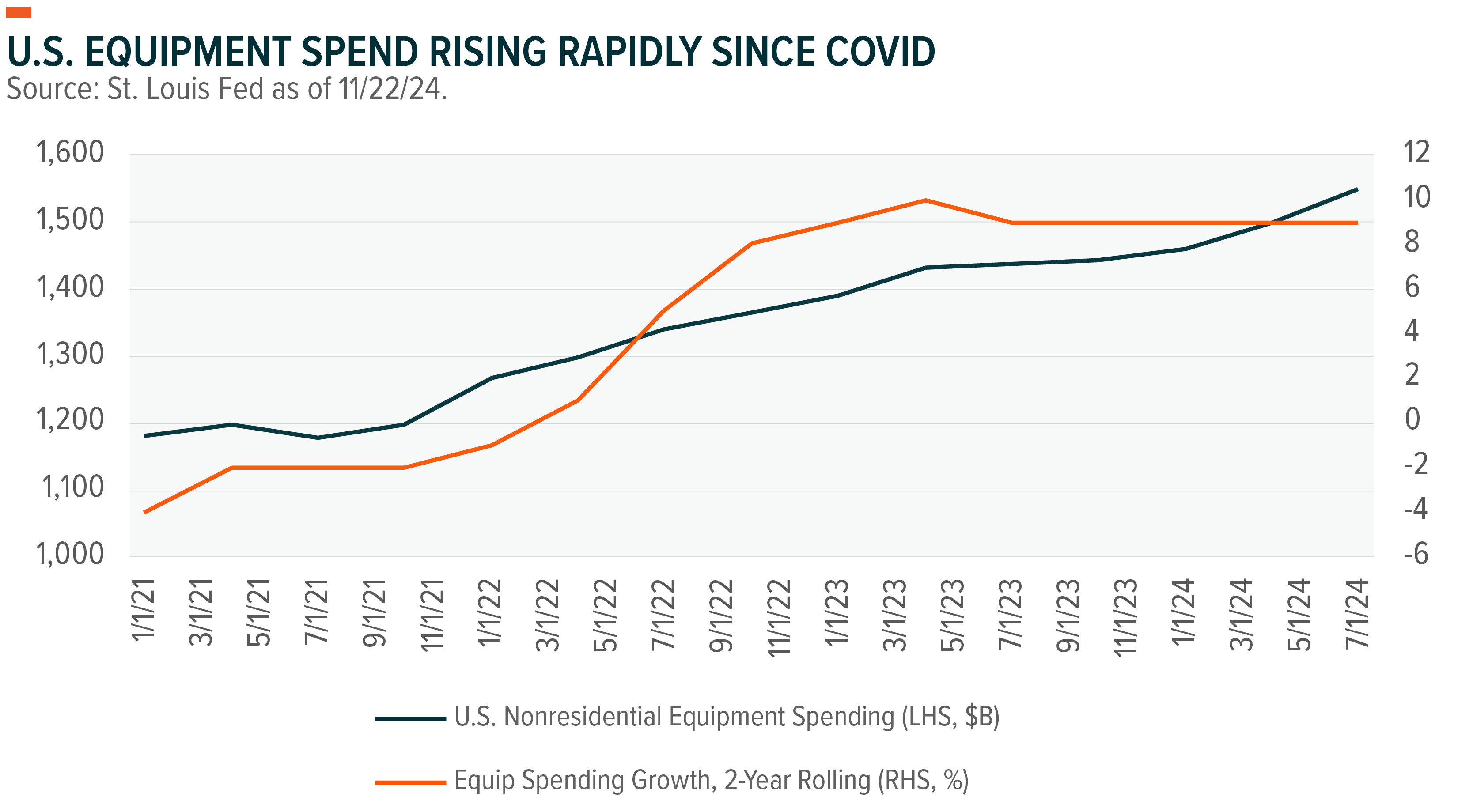

Corporate investment was another important catalyst. Mega-cap tech was the standout, with its robust investments in data centers, AI, and related technologies.7 Outside of the hyperscalers, though, capital expenditure growth slowed from the blistering pace of 2022 and 2023. In Q3 2024, quarter-over-quarter (QoQ) private investment fell to just 1.1% from 10.1% the prior year, but companies continued to invest.8 Year-over-year (YoY), nonresidential investment was up 5.2% and equipment spending grew 7.8%.9

Investments to improve productivity continued to show up in margins. As of Q3 2024, S&P 500 companies had delivered quarterly profit margins above 12% since September 2021.10 Many of the themes central to this business transformation reported topline growth and healthy margins. AI companies grew sales by 8% and delivered margins of 11%, while Digital Infrastructure firms such as data centers had topline growth of 14% with 14% margins.11

Other themes tied to this automation and digitalization revolution, like Cybersecurity, reported sales growth of more than 15%. Robotics and Automation slowed slightly, growing the topline at 6% with margins of 8%. U.S. Infrastructure continued to deliver healthy margins at 9%. Defense Technology delivered strong returns on sales growth of 15%.12 Consumer themes such E-Commerce, Millennial Consumers, and Video Games & Esports proved contrarian this year, delivering strong returns despite fears that a consumer slowdown would hurt sales. Renewable Energy and CleanTech lagged.*

Relatively strong thematic performance followed the broader market’s modest risk-on sentiment. The S&P 500 rose by approximately 25%, while the S&P Aggregate Bond Index returned just 2%.13 The Financials, Tech, and Communication Services sectors led, all returning above 30% year-to-date, while Healthcare, Materials, and Real Estate lagged.14 Small-cap stocks mounted a surprise comeback after years of underperformance, beating the S&P 500 by 11% since July. U.S. equities continued to beat international markets.15

The three pillars of the economy, labor, leverage, and liquidity, seem relatively sound going into 2025.16 The potential net impact of higher tariffs, lower taxes, deregulation, and less immigration, however, could upend the status quo. The right policy mix could stimulate the economy, but there are also implications for inflation and interest rates.

The general consensus among economists is that higher tariffs generate inefficiency and create deadweight losses to consumers that slow an economy by moving money from the private to the public sector.17 Simply looking at the relationship between GDP or consumption and tariffs is a bit misleading. Consumer spending typically increases, but it’s higher prices for the same goods that drive the increase.

Proponents suggest that tariffs stimulate domestic industry and job creation.18 GDP growth typically rises in the quarter that tariffs are increased, though that impact disappears one quarter later.19 Price increases on intermediate goods take time to work through the economy. According to one estimate, the tariffs implemented during the first Trump administration and retained during the Biden administration adversely affected GDP growth by 0.2%.20 Historically, the negative effects of tariff increases are seen at the household level. Real disposable income growth slows, while debt levels increase faster when import duties increase faster than the long-term average of 2%.21

Taxes complicate matters. Higher tariffs move money from the private sector to the government, while tax cuts move money in the opposite direction. Focusing on either policy lever in isolation can be misleading. If tariffs create deadweight loss, consumer and corporate tax cuts could alleviate it. As more money moves out of the private sector, the bigger the risk of economic slowdown.

The sensitivity analysis below tries to capture these tradeoffs by looking at potential incremental impacts based on 2023 trade data.22 Our base case is a modest transfer of 0.3% of GDP from the private sector to government. While not insignificant, this outcome would be far less than the maximal tariff policy President-elect Trump discussed on the campaign trail. Softer tariffs or a bigger tax cut could easily offset that transfer and perhaps even stimulate the private sector.

Changes to immigration policy and the regulatory environment may also shape the economy in 2025. Stricter immigration could help to reinforce the strong labor market with fewer available employees. A scenario where demand outruns supply and labor costs increase would run contrary to the Federal Reserve’s goal of slowing wage inflation.23 Continued strength in the job market and further real wage growth, however, could help sustain consumption and services growth.

Deregulation could unlock pent-up investment and help industries restructure. Corporate activity has been sluggish. New issues have been slow to market, merger activity has not accelerated, companies are not returning cash to shareholders, and there are significant sums locked up in private funds that must be returned.24 A looser regulatory environment should encourage companies to build and invest. That said, regulatory changes often have unintended consequences. For example, the Dodd-Frank bank regulations were intended to reduce risks from the systemically important institutions, but they wound up getting even bigger.25

And then there’s the market’s favorite obsession: interest rates. The Fed is on track for 100 basis points (bp) of cuts in 2024. At the start of the year, the market was pricing in a fed funds rate of 3.75% by year-end 2025. Currently, the market’s pricing 3.93%, a slight increase that likely reflects a reassessment of inflation pressures.26 For example, higher tariffs would drive up the cost of consumer goods. Reduced immigration could mean higher wages. Lower taxes could stoke inflation through demand.

Historically, interest rate volatility tends to rise during protectionist periods with higher tariffs, so interest rate expectations may fluctuate widely as different policies get rolled out and affect economic data. In our view, the market’s rate cut expectations are slightly off, and we expect four 25bp cuts in 2025, though our confidence around the path of rate policy is likely to be impacted by tariff and tax decisions.

The two areas that could prove critical to our favorable outlook for the U.S. economy in 2025 are manufacturing and small-cap spending. We believe that conditions are ripe for them to outperform, with the main risk to our positive outlook coming from potential interest rate volatility dampening the animal spirits necessary to stimulate both.

Manufacturing has been in the doldrums, contracting in 23 of the past 24 months. Excluding the modest expansion in March 2024, it’s the longest period of contraction in 25 years.27 Manufacturing is now a smaller part of the economy relative to services, but it still accounts for approximately $7 trillion, or 25% of GDP.28 New orders essentially plateaued between 2007 and 2018. The breakout to a new steady state coincided with higher tariffs in 2018 and COVID supply chain challenges in 2020. Historically, a 1% increase in tariffs is associated with a 0.2% increase in new orders and modest increase in hours worked, so modest protectionist policy might help jump start production.

Tariff policies aimed at stimulating manufacturing may trigger a slowdown in the services sector if consumers alter their spending due to higher prices. That risk, however, could be lower than some expect, as business services could offset a decline in consumer activity. In 1959, consumption accounted for approximately 82% of service spending, but today it’s only about 60%.29

Increased business activity combined with deregulation may encourage small- and mid-cap companies to spend. Capital expenditure accelerated rapidly in 2022 and 2023, rising by double digits for 10 straight quarters and snapping an almost two-decade draught in corporate investment.30 Russell 2000 constituents were even outspending mega-cap tech companies, but that changed in 2024, and now their capital expenditure is just a fraction. Creating conditions that encourage expansion and investment can be difficult, as small businesses must operate with discretion given their resource constraints, though we believe that small business sentiment can improve in 2025. Should small-caps returns to prior spending levels, that could amount to $140 billion and a 4.0% lift to nonresidential private investment.31

A recovery in manufacturing and small caps should not only be good for growth, but it could also help support higher market valuations. Multiples on major indexes have been advancing since June 2022, and the S&P forward price-to-earnings is around 24 times.32 This multiple seems a bit lofty, though we continue to argue that valuations may be undergoing a lasting rerating higher. Since 1949, multiples move higher as profit margins improve and businesses become more efficient, and now companies are racing to adopt new technologies and processes that can improve operations.33

Going into 2025, there are two critical questions about valuation. The first is whether record high profit margins are sustainable or whether they mean-revert. If margins backslide, we would expect multiples to come down, though that is not our base case. Consensus forecasts are for further margin expansion to 13.8%.34 The second question is whether earnings stability can improve. While S&P 500 earnings volatility has increased in recent quarters, a better growth and regulatory environment could help foster consistency.

Improved manufacturing and increased small-cap capital expenditure could help broaden market participation and lead to higher multiples. In fact, this combination is already evident to some extent with 73% of the S&P 500 trading above their 200-day moving average.35 Resurgence in some left-behind segments of the economy may not necessarily dent the mega-cap market concentration, but in our view, it is the most likely path to improved market breadth in 2025.

Equities and risk assets may be poised for another year of good performance; however, the unique set of economic and policy circumstances likely warrants a more targeted approach in 2025. An allocation strategy that aligns with a few key themes tied to U.S. competitiveness in can offer reasonable upside and a degree of insulation from potential volatility.

Other themes feature strong fundamentals and could prove successful in 2025.

Income investors may want to adopt a more targeted approach going into 2025 given the policy uncertainty and potential interest rate volatility. Many debt instruments could underperform in a volatile interest rate environment, led by long duration. To minimize sensitivity to rate uncertainty, equity income strategies can offer solutions.

Like last year, we believe that economic growth is likely to surprise on the upside and markets can continue to trend higher. What’s different may be the growth drivers. Some market participants posit that equity valuations on broad indexes seem stretched, but in our view, flows suggest investors are ready to embrace risk-on assets. Better market breadth, further profit margin improvement, and continued earnings growth could help lift equity valuations further. By contrast, fixed income may be stuck in limbo given the potential for interest rate volatility, possibly requiring investors to get more creative and look for differentiated strategies.

Key Takeaways

- Strength in the services sector and corporate investment from mega-cap tech firms helped power better-than-expected economic growth in 2024.

- Economic uncertainty is likely to remain elevated given the potential tradeoffs and net effects of lower taxes, higher tariffs, less immigration, more stimulus, and less regulation.

- A manufacturing recovery paired with renewed small- and mid-cap corporate investment can extend the mid-cycle expansion, translating to better market breadth and higher valuation multiples.

- For 2025, we focus on growth themes tied to U.S. competitiveness that seem reasonably priced. For income investors, equity income strategies may help offset potential rate volatility.

2024 Inspection: Services and Investment Dominate

For the second year in a row, the U.S. economy did better than consensus expectations. Forecasts called for real GDP growth of 0.5–1.5% at the start of 2024, with the thesis being that an overstretched consumer and a consumption pullback would cause companies to curb investment.2 Neither happened, for the most part, and the economy averaged 2.5% real quarterly growth through Q3 2024.3 The consumer remained resilient, despite the end of COVID stimulus, and consumption grew by 3.5% in Q3, up from 2.5% in the prior year.4

A strong labor market and services sector expansion supported consumption. While unemployment moved higher, from 3.4% to 4.1%, layoffs were contained.5 Companies continued to hire, consumers continued to spend on services, and inflation in areas like travel and restaurants proved sticky compared to other areas.6 The services sector strength was important, as manufacturing employment and production remained in contraction for most of 2024.

Corporate investment was another important catalyst. Mega-cap tech was the standout, with its robust investments in data centers, AI, and related technologies.7 Outside of the hyperscalers, though, capital expenditure growth slowed from the blistering pace of 2022 and 2023. In Q3 2024, quarter-over-quarter (QoQ) private investment fell to just 1.1% from 10.1% the prior year, but companies continued to invest.8 Year-over-year (YoY), nonresidential investment was up 5.2% and equipment spending grew 7.8%.9

Investments to improve productivity continued to show up in margins. As of Q3 2024, S&P 500 companies had delivered quarterly profit margins above 12% since September 2021.10 Many of the themes central to this business transformation reported topline growth and healthy margins. AI companies grew sales by 8% and delivered margins of 11%, while Digital Infrastructure firms such as data centers had topline growth of 14% with 14% margins.11

Other themes tied to this automation and digitalization revolution, like Cybersecurity, reported sales growth of more than 15%. Robotics and Automation slowed slightly, growing the topline at 6% with margins of 8%. U.S. Infrastructure continued to deliver healthy margins at 9%. Defense Technology delivered strong returns on sales growth of 15%.12 Consumer themes such E-Commerce, Millennial Consumers, and Video Games & Esports proved contrarian this year, delivering strong returns despite fears that a consumer slowdown would hurt sales. Renewable Energy and CleanTech lagged.*

Relatively strong thematic performance followed the broader market’s modest risk-on sentiment. The S&P 500 rose by approximately 25%, while the S&P Aggregate Bond Index returned just 2%.13 The Financials, Tech, and Communication Services sectors led, all returning above 30% year-to-date, while Healthcare, Materials, and Real Estate lagged.14 Small-cap stocks mounted a surprise comeback after years of underperformance, beating the S&P 500 by 11% since July. U.S. equities continued to beat international markets.15

The Task for 2025: Understanding the Economic Uncertainty Ahead

The three pillars of the economy, labor, leverage, and liquidity, seem relatively sound going into 2025.16 The potential net impact of higher tariffs, lower taxes, deregulation, and less immigration, however, could upend the status quo. The right policy mix could stimulate the economy, but there are also implications for inflation and interest rates.

The general consensus among economists is that higher tariffs generate inefficiency and create deadweight losses to consumers that slow an economy by moving money from the private to the public sector.17 Simply looking at the relationship between GDP or consumption and tariffs is a bit misleading. Consumer spending typically increases, but it’s higher prices for the same goods that drive the increase.

Proponents suggest that tariffs stimulate domestic industry and job creation.18 GDP growth typically rises in the quarter that tariffs are increased, though that impact disappears one quarter later.19 Price increases on intermediate goods take time to work through the economy. According to one estimate, the tariffs implemented during the first Trump administration and retained during the Biden administration adversely affected GDP growth by 0.2%.20 Historically, the negative effects of tariff increases are seen at the household level. Real disposable income growth slows, while debt levels increase faster when import duties increase faster than the long-term average of 2%.21

Taxes complicate matters. Higher tariffs move money from the private sector to the government, while tax cuts move money in the opposite direction. Focusing on either policy lever in isolation can be misleading. If tariffs create deadweight loss, consumer and corporate tax cuts could alleviate it. As more money moves out of the private sector, the bigger the risk of economic slowdown.

The sensitivity analysis below tries to capture these tradeoffs by looking at potential incremental impacts based on 2023 trade data.22 Our base case is a modest transfer of 0.3% of GDP from the private sector to government. While not insignificant, this outcome would be far less than the maximal tariff policy President-elect Trump discussed on the campaign trail. Softer tariffs or a bigger tax cut could easily offset that transfer and perhaps even stimulate the private sector.

Changes to immigration policy and the regulatory environment may also shape the economy in 2025. Stricter immigration could help to reinforce the strong labor market with fewer available employees. A scenario where demand outruns supply and labor costs increase would run contrary to the Federal Reserve’s goal of slowing wage inflation.23 Continued strength in the job market and further real wage growth, however, could help sustain consumption and services growth.

Deregulation could unlock pent-up investment and help industries restructure. Corporate activity has been sluggish. New issues have been slow to market, merger activity has not accelerated, companies are not returning cash to shareholders, and there are significant sums locked up in private funds that must be returned.24 A looser regulatory environment should encourage companies to build and invest. That said, regulatory changes often have unintended consequences. For example, the Dodd-Frank bank regulations were intended to reduce risks from the systemically important institutions, but they wound up getting even bigger.25

And then there’s the market’s favorite obsession: interest rates. The Fed is on track for 100 basis points (bp) of cuts in 2024. At the start of the year, the market was pricing in a fed funds rate of 3.75% by year-end 2025. Currently, the market’s pricing 3.93%, a slight increase that likely reflects a reassessment of inflation pressures.26 For example, higher tariffs would drive up the cost of consumer goods. Reduced immigration could mean higher wages. Lower taxes could stoke inflation through demand.

Historically, interest rate volatility tends to rise during protectionist periods with higher tariffs, so interest rate expectations may fluctuate widely as different policies get rolled out and affect economic data. In our view, the market’s rate cut expectations are slightly off, and we expect four 25bp cuts in 2025, though our confidence around the path of rate policy is likely to be impacted by tariff and tax decisions.

Shifting Gears: Manufacturing and Small-Cap Investment to the Fore

The two areas that could prove critical to our favorable outlook for the U.S. economy in 2025 are manufacturing and small-cap spending. We believe that conditions are ripe for them to outperform, with the main risk to our positive outlook coming from potential interest rate volatility dampening the animal spirits necessary to stimulate both.

Manufacturing has been in the doldrums, contracting in 23 of the past 24 months. Excluding the modest expansion in March 2024, it’s the longest period of contraction in 25 years.27 Manufacturing is now a smaller part of the economy relative to services, but it still accounts for approximately $7 trillion, or 25% of GDP.28 New orders essentially plateaued between 2007 and 2018. The breakout to a new steady state coincided with higher tariffs in 2018 and COVID supply chain challenges in 2020. Historically, a 1% increase in tariffs is associated with a 0.2% increase in new orders and modest increase in hours worked, so modest protectionist policy might help jump start production.

Tariff policies aimed at stimulating manufacturing may trigger a slowdown in the services sector if consumers alter their spending due to higher prices. That risk, however, could be lower than some expect, as business services could offset a decline in consumer activity. In 1959, consumption accounted for approximately 82% of service spending, but today it’s only about 60%.29

Increased business activity combined with deregulation may encourage small- and mid-cap companies to spend. Capital expenditure accelerated rapidly in 2022 and 2023, rising by double digits for 10 straight quarters and snapping an almost two-decade draught in corporate investment.30 Russell 2000 constituents were even outspending mega-cap tech companies, but that changed in 2024, and now their capital expenditure is just a fraction. Creating conditions that encourage expansion and investment can be difficult, as small businesses must operate with discretion given their resource constraints, though we believe that small business sentiment can improve in 2025. Should small-caps returns to prior spending levels, that could amount to $140 billion and a 4.0% lift to nonresidential private investment.31

A recovery in manufacturing and small caps should not only be good for growth, but it could also help support higher market valuations. Multiples on major indexes have been advancing since June 2022, and the S&P forward price-to-earnings is around 24 times.32 This multiple seems a bit lofty, though we continue to argue that valuations may be undergoing a lasting rerating higher. Since 1949, multiples move higher as profit margins improve and businesses become more efficient, and now companies are racing to adopt new technologies and processes that can improve operations.33

Going into 2025, there are two critical questions about valuation. The first is whether record high profit margins are sustainable or whether they mean-revert. If margins backslide, we would expect multiples to come down, though that is not our base case. Consensus forecasts are for further margin expansion to 13.8%.34 The second question is whether earnings stability can improve. While S&P 500 earnings volatility has increased in recent quarters, a better growth and regulatory environment could help foster consistency.

Improved manufacturing and increased small-cap capital expenditure could help broaden market participation and lead to higher multiples. In fact, this combination is already evident to some extent with 73% of the S&P 500 trading above their 200-day moving average.35 Resurgence in some left-behind segments of the economy may not necessarily dent the mega-cap market concentration, but in our view, it is the most likely path to improved market breadth in 2025.

Building Portfolio Resilience: Looking at 2025

Equities and risk assets may be poised for another year of good performance; however, the unique set of economic and policy circumstances likely warrants a more targeted approach in 2025. An allocation strategy that aligns with a few key themes tied to U.S. competitiveness in can offer reasonable upside and a degree of insulation from potential volatility.

- Infrastructure Development: A centerpiece of the U.S. competitiveness story is the ongoing infrastructure renaissance. Construction, equipment, and materials companies have benefitted from infrastructure-related policies and they are in line to benefit from approximately $700 billion in additional spending over the next few years.36 Despite strong performance in recent years, these companies are generally priced at valuation multiples below the S&P 500.37 Also, these traditionally stodgy industries are adopting new technologies and practices that may drive margin expansion.

- Defense and Global Security: A string of interconnected global conflicts presents a new challenge for the United States and its allies. These evolving threats are likely to prove persistent and unconventional, translating to adoption of new tactics, techniques, and technologies across physical and virtual domains. Global defense spending, which totaled $2.24 trillion in 2022, is expected to increase 5% annually in 2025.38 Defense company revenue is expected rise by almost 10%, and margins are forecasted to improve from 5.2% to 7.6%.39 Compared to traditional defense platforms like battleships and fighter jets, lower-cost solutions like AI and drones combined with greater automation in production processes should continue to improve profitability.

- Automation, AI, and Onshoring: Initiatives to onshore production and boost U.S. manufacturing likely require increased automation. We believe 2025 is likely the first year that software and service companies begin monetizing these technologies. The expectations for 2025 sales and margins are better than the S&P 500 and selling at a similar multiple.40 Data centers are another piece of the puzzle to ensure that these technologies have the capacity to run. Mega-cap tech is expected to increase spending on data center development from $213 billion in 2024 to $250 billion in 2025.41 We also expect robotics and Internet of Things connectivity hardware to accelerate, despite sales plateauing in 2024.42

- Energy Independence and Nuclear Power: Energy needs were expected to increase markedly before AI, and now AI has those forecasts are even higher. Fossil fuels will remain an essential part of the energy mix, but cost-effective and environmentally friendly alternatives to meet incremental demands are critical. The tech sector has turned its attention to nuclear energy with many of the mega-caps announcing plans to use existing facilities or build small modular reactors (SMRs).43 Beyond the United States, Japan, Germany, and Australia are also likely to add to nuclear capacity creating a robust demand for uranium.

Other themes feature strong fundamentals and could prove successful in 2025.

Income investors may want to adopt a more targeted approach going into 2025 given the policy uncertainty and potential interest rate volatility. Many debt instruments could underperform in a volatile interest rate environment, led by long duration. To minimize sensitivity to rate uncertainty, equity income strategies can offer solutions.

- Covered Calls: Strategies that sell options on underlying equity assets can generate reasonably stable income with limited exposure to interest rates. These strategies collect the premium from writing calls and distribute those premiums as income.44 The underlying value can fluctuate with the broad index, and thereby be indirectly impacted by volatility, but these strategies do not have the direct exposure to interest rate risks as fixed income. To the extent that fluctuating interest rates increase equity market volatility, it often increases the premiums collected on the calls and maximizes income.

- Energy Infrastructure: Master limited partnerships (MLPs) are energy infrastructure assets like pipelines that can generate income without direct exposure to interest rates. These assets generally pay out steady dividends. Many pipeline and infrastructure companies have long-term supply contracts that stabilize cash flow. While the underlying value can move with oil prices, the correlation is generally modest because they don’t extract or own the commodity, they simply move it. Also, real assets like commodities and energy infrastructure are often treated as inflation hedges.

- Preferred Stocks: Preferreds sit higher on the capital structure than common equity but below fixed income. They sell at a par value and pay out a regular fixed or variable dividend. Unlike bonds, investors are not guaranteed the payments contractually, but they must be paid before any dividends to regular equity holders. Preferreds are issued at par with a predetermined payout structure, so they can be interest rate-sensitive. Because they are riskier than debt, though, they can pay a higher dividend. Most preferred securities are issued by banks, which have a regular cash flow tied to their net interest income. Given the potential for deregulation in the financial sector and an acceleration in small business lending, preferreds may be an attractive income option.