Global X Research Team

Global X Research TeamAt this year’s Inside ETFs Conference, I participated in a panel called ‘Everything You Need to Know: The Thematic Crystal Ball’ which covered a range of topics related to thematic investing: top themes for 2019, what makes a good theme, why investors should consider thematic investing, and more. During the Q&A portion of the panel, we unfortunately ran out of time before addressing an important question that I was eager to discuss with my fellow panelists: ‘Should thematic ETFs be equal weighted or market cap weighted?’ In the piece below, I share Global X’s perspective on weighting thematic ETFs, and welcome the debate with fellow panelists that unfortunately didn’t happen on stage.

Constructing a portfolio of securities ultimately comes down two major decisions: 1) what should I own (selection); and 2) how much should I own (weighting). Whether investing in themes, factors, sectors, or broad asset classes, these two questions are unavoidable. Beneath these two overarching questions, there are indeed multiple detailed sub-questions such as rebalance and reconstitution frequency, IPO and corporate action treatments, and so on, but ultimately these roll up under the overarching questions of what to own and how much.

It’s safe to say that most investors likely focus more attention on selection than weighting scheme. The decision to own US Large Cap or Emerging Market Small Caps is likely debated longer in investment committees than whether broad US equities exposure should be market cap weighted or equal weighted. Yet weighting scheme should not be ignored – it is a key contributor to both risk and returns. Over the last 10 years, for example, the S&P 500 Equal Weight Index has had annualized returns of 18.84% with a volatility of 15.09% compared to 16.67% annualized returns and volatility of 12.90% for the regular market cap weighted S&P 500 Index.1 Owning the same ~500 stocks with a different weighting scheme added 2.17% more annual returns, with 2.19% higher risk, which is a meaningful difference over 10 years.

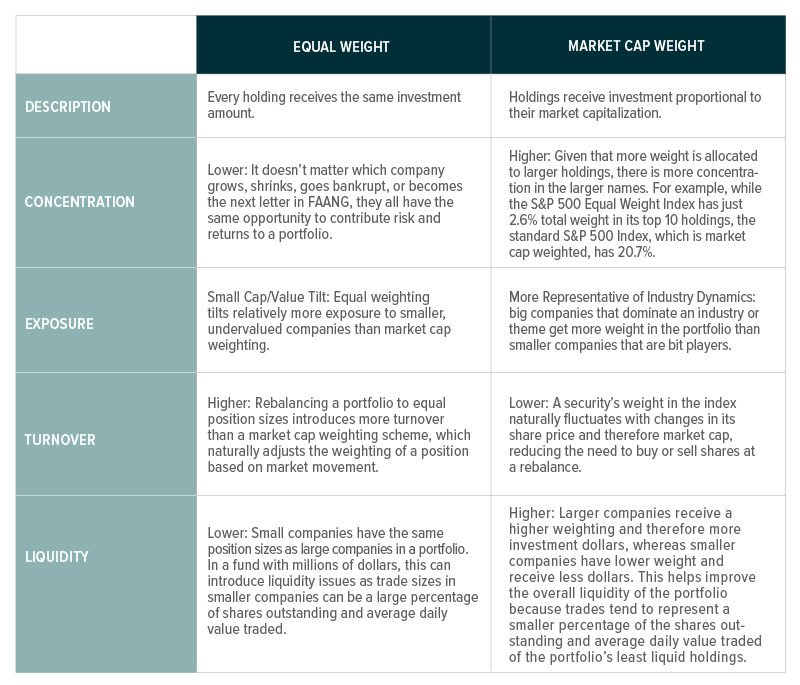

When developing a thematic ETF and working with an index provider to create the index methodology, the same key questions apply: what securities should be selected and how much weight should be in each security. On the selection front, our product team spends months during the R&D phase ‘defining’ a new theme: taking a concept like robotics & AI and translating it into a rules-based process to identify key companies in the space. But also significant is the decision of which weighting scheme to apply to those companies. While there are infinite approaches to weight a basket of securities, we most frequently encounter two approaches in thematic ETFs: equal weighting and market cap weighting. Below is a brief discussion of the characteristics of both approaches.

Which Do We Choose?

While there are trade-offs with both approaches, at Global X, our thematic growth ETFs follow a market cap weighted-based approach, which contrasts with many thematic ETFs in the market that opt for equal weight-based approaches.

The key reason why we opt for the market cap weighted-based approach is to be more representative of industry dynamics. We view many themes as sector disruptors, or new industries that are challenging existing paradigms. In such emerging industries there is still much to be settled. Which company will be the dominant robotics maker in 20 years? Which company will struggle and go bankrupt? With a market cap weighted approach, we gain more exposure to companies as they begin to dominate an industry and reduce exposure to those that are failing. By contrast, an equal weighted approach is forced to sell exposure to companies as they grow and buy those that struggle. In other words, market cap weighting increases exposure to Amazon as it grows and reduces exposure to Pets.com as it dies. An equal weight strategy would sell Amazon while it grows and buy more of Pets.com as it fails.

While some might argue that in the aggregate smaller companies offer higher growth opportunities than larger companies and therefore warrant more exposure than a market cap weighting scheme offers, we do not always find this to be the case in disruptive industries. Using history as our guide, recent powerful themes have demonstrated that larger companies enjoy enormous benefits due to economies of scale and network effects. Apple and Samsung dominate the smart phone market due to the high fixed costs of developing cutting edge phones and software. Google dominates search as more searches breed better search results, which in turn breeds more people searching. In e-commerce, Amazon dominates because of both the network effects of having a two-sided marketplace connecting buyers and sellers, and the economies of scale of efficient distribution.

Going forward, we think this trend will continue. In FinTech, for example, we believe mobile payment providers will have strong economies of scale through access to data and complimentary business services offerings. In the robotics industry, the high fixed costs of developing both an advanced robot and the software required to operate it will continue to accrue benefits to the market leaders. In short, we want to own more of the bigger companies. Yes, small companies will emerge and challenge the status quo, but in many of these new industries, we think there are substantial economic benefits to being larger. And as a small company begins to prove itself, we’ll begin to own more of that company.

The advantages of better representing the dynamics of an emerging industry, combined with the added benefits of improved liquidity and lower turnover, which help reduce transaction costs, ultimately sway our decision to favor market cap weighting schemes. While market weighting is not perfect, many of the indexes we track include minor variations to a pure market cap weighting approach to address some of its shortcomings. For example, many indexes we track include a cap on the largest position size to mitigate overly top-heavy portfolios. The index tracked by our Robotics & AI ETF, for example, caps the largest position size at 8%. We believe this approach gives us an optimal solution for thematic investing: an index that is representative of the industry, mitigates excessive levels of concentration, maintains high liquidity, and has lower turnover.

Conclusion

There’s no single ‘right’ way to weight an ETF because there are tradeoffs with each approach. In the thematic growth space, we favor market cap weighting as a way of mirroring an emerging industry, improving liquidity, and reducing turnover. In investment strategies where minimizing idiosyncratic risks is more of a priority, we believe equal weighting can still make sense. This is the case with our SuperDividend suite, for example, where mitigating the impact of a company changing its dividend policy is preferred. But as investors consider different ETFs, it’s important to remember not to just look at what an ETF holds, because how much can be just as significant in aligning one’s investments with their goals.