Global X Research Team

Global X Research TeamAs COVID-19 grips global markets, we consider the pandemic’s short- and long-term implications for Emerging Markets (EMs). We also highlight the critical factors in assessing the strength of EM’s during this time, such as prior experience with viral outbreaks, the state of public health systems, leadership and policy measures to prevent the virus’s spread, and fiscal and monetary options to stimulate economic growth.

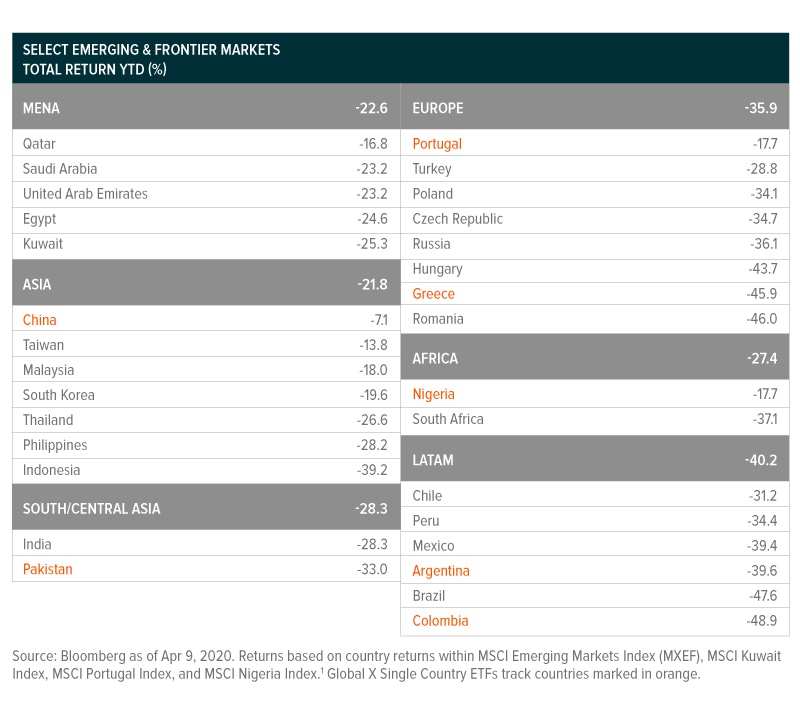

EMs Face Additional Pressures Both from the Outside and from Within

Like their developed market (DM) counterparts, EMs are contending with unprecedented health, societal, and economic challenges as a result of the COVID-19 outbreak. But given differences in demographics, institutions, and economic strength, EMs face additional external and internal challenges. From the outside, broader aversion to risk around the globe may scare away foreign capital from EM equities or debt. Such flows can increase the cost of capital for EMs, making it more difficult or expensive to raise capital, or even service existing hard currency debt. Further, a slowing global economy could threaten demand for raw materials and finished goods, placing greater strain on export-dependent economies. From within, EMs are struggling to control the spread of the virus, including enacting stay at home policies, supporting weak health care infrastructure, and stimulating their economies with a limited set of fiscal and monetary tools.

Key Factors for EMs in Combating COVID-19

EMs best equipped for crisis will be those with experience or a responsive approach to virus control, strong public health infrastructure, proactive leadership on policy and public health measures, less exposure to low oil prices, as well as long-term focused economic stimulus measures.

Leadership: Some countries, like Indonesia, Brazil, and Mexico, whose leaders were slower to act to prevent the spread of COVID-19, may face longer-term public health and economic damage as the virus spreads. On the opposite end, countries like Argentina, Colombia, and South Korea, whose leaders were proactive and enacted stay-at-home orders quickly, are likely to contain the spread of COVID-19 sooner. Both Colombia and Argentina reported very few cases of the virus so far, likely helped by swift policy actions. Such decisive leadership is particularly important in Emerging Markets, many of which are less prepared for the pandemic given already fragile economies, underdeveloped public health systems, and limited policy tools.

Health Care Systems: Health care services are expensive and tend to be less comprehensive in EMs than developed countries. But within EMs, there is still a wide range of quality and access to health care. Some countries like China have relatively established systems that can adapt to surges in COVID-19 cases, whereas others like India and Argentina have taken early and harsh steps to avoid overwhelming their weaker public health care systems.

Oil Exposure: Countries like Kuwait in the Middle East and North Africa (MENA) region, as well as frontier markets like Nigeria, face the dual problems of COVID-19 and record-low oil prices. These oil exporters are suffering from crashing prices as demand plummets. Many of these countries depend on oil revenues to fund key government social policies, including health care, which could compound COVID-related issues for these countries. These countries could face further headwinds should prolonged low prices diminish their terms of trade or have a depreciative impact on their currency. On the other hand, oil importers may see some inadvertent stimulus from low oil prices, as consumers and businesses pay less for energy. This could be particularly impactful for countries like China, India, or countries in Southeast Asia, which may reap the benefits of lower input costs as manufacturing and consumerism comes back online.

Fiscal and Monetary Stimulus: countries with greater capacity to stimulate economic growth, either through fiscal stimulus (government spending) or monetary stimulus (cutting interest rates), will likely rebound economically faster than others. EMs generally have less room for stimulus than advanced economies and therefore may need to implement more targeted and creative solutions.

Monetary Stimulus: As the general exception to EMs because of its sheer size and importance to global markets, China’s ability to implement monetary stimulus sets it apart. To offset the impact of COVID-19, Beijing has taken multiple steps to limit the deterioration of financial conditions, including several short- and medium-term rate cuts by the PBOC, the reduced reserve requirements, and the expansion of credit facilities and terms for lending. Other large EM central banks also cut rates to offset the economic impact of COVID-19, including Korea, India, Brazil, Turkey and Chile, while countries like Argentina and Russia eased credit conditions and lowered reserve requirements for households and SMEs.2

Fiscal Stimulus: According to the IMF, global fiscal actions to combat the economic impact COVID-19 could amount to $8 trillion – including $7 trillion from the Group of Twenty (G20). These funds include emergency funding initiatives, public sector loans, and guarantees. Several EM countries, including Brazil, have announced emergency economic packages to support the most vulnerable, to maintain employment levels, and to combat COVID-19. India, Brazil, and Mexico are reducing personal income tax rates or expanding cash transfer programs. Developed Markets have taken lessons from Emerging Markets, like Korea, which gave wage subsidies and expanded unemployment benefits early on to encourage people to stay home. China accelerated unemployment disbursements, and in Korea and China, officials are providing tax breaks for key industries.

Experience with Outbreaks: Emerging Markets in the APAC region, for example, tend to have more experience with virus outbreaks such as SARS, MERS, H1N1, and Swine Flu. In Latin America and Africa, some EMs have experience with disease or viral outbreaks as well, including Zika, West Nile, and Dengue, but many either lack the policy framework or public health infrastructure to control the spread. Such experience can be critical in responding to the crisis quickly, slowing the spread of the outbreak, and treating those who are infected.

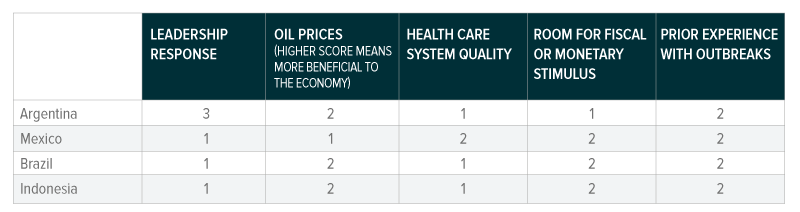

Countries with the Most Vulnerabilities

Countries that are most vulnerable to COVID-19 are those that took long to respond to the outbreak, are adversely impacted by low oil prices, have weak health care systems, even compared to other EMs, have little room for fiscal or monetary stimulus, and have little experience dealing with prior viral outbreaks.

In the table below, we highlight a few countries that score poorly on these measures.

1= below average, 2 = average, 3 = above average

Scores based on Global X ETF’s outlook regarding the country’s response to each issue. Scores are strictly opinion based and do not represent a rating of any securities or company. For informational purposes only.

Inaction in countries like Indonesia, Brazil, or Mexico, which waited a longer time to promote social distancing, are likely to face longer term hurdles of unknown proportions to contain the virus. Countries with weak fiscal positions and high foreign-denominated debt, like Argentina, Peru, Ecuador, Turkey, Indonesia, and South Africa, could face economic headwinds if they are unable to implement sustainable stimulus measures or garner necessary support from the international community, including the IMF.

Central banks with high external debt are more sensitive to currency movements and as such, have less influence over inflation and employment and fewer mechanisms to fulfill their mandates of monetary and economic stability. Central banks looking to cut rates face the tradeoff between depreciating their currency and providing needed stimulus to the local economy. This tradeoff leaves central banks in such EMs with little margin for error and often forces them to turn to the IMF as a lender of last resort.

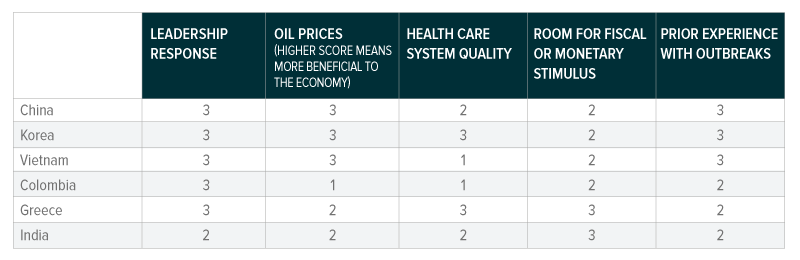

Potential Bright Spots and Best Cases

In the table below, we show examples developing economies that may be better positioned to handle the crisis.

1= below average, 2 = average, 3 = above average

Scores based on Global X ETF’s outlook regarding the country’s response to each issue. Scores are strictly opinion based and do not represent a rating of any securities or company. For informational purposes only.

Monetary or fiscal support is expected to play an important role in supporting certain EMs. Since the outbreak, nearly 103 countries have approached the IMF about potential funding to protect their most affected populations and industries.3 To combat what it sees as the world’s worst economic crisis since the Great Depression, the IMF doubled funds available for emergency relief to meet expected demand of over $100 billion, and suspended debt repayments by six months for the most vulnerable and low-income countries. While IMF expanded a $1 trillion funding facility to serve those most affected, such immense pressure from the global community could very well overwhelm the institution’s financing capabilities.

In addition to funding, there are other mechanisms that could have an enormous impact on these markets as well. Greece has a unique lifeline with additional support from the ECB. Greece already earmarked 10 billion euros from its budget and funds from the ECB to support its vulnerable populations and industries, which would likely include the shipping, tourism, and banking. The ECB also announced a $860 billion asset purchase program, which will include Greek bonds previously exempt for purchase by the ECB due to their low credit ratings.

Also critically important is the early success in containing COVID-19. Countries in the APAC region leveraged their prior experience with outbreaks to quickly enact contact tracing technologies, which are currently considered for rollout across several states in the US. Such technologies can identify people who have or may have encountered the virus, allowing for more preventative measures to be taken faster. Emerging Markets benefit greatly from adopting contact tracing technology, because it could reduce dependence on otherwise deficient public health systems.

Contact tracing appears to be used effectively in China, where harsh but effective transmission control allowed economic activity to resume relatively quickly. After reaching all-time record lows in February, manufacturing data rose back out of contraction in March, as workers returned to their occupations. Although Q1 GDP data reflected a 6.8% year-on-year contraction, many forecasts estimate that GDP will begin its rebound in Q2 ahead of most of the rest of the world.

Conclusion

The eventual economic recovery will look drastically different between countries. Although Emerging Markets may be disproportionately hurt from COVID-19, there are some countries that may be more resilient than their developed market peers. EMs are no stranger to crises, particularly those within Emerging Asia, which saw the Global Financial Crisis, the Russian Banking Crisis, and the 1997 Asian Financial Crisis all in a relatively short period of time. History suggests that while EMs may sell off faster than developed markets under periods of stress, they tend to recover more quickly. And although the COVID-19 pandemic is unique and initially began in Asia, giving it a natural head-start in terms of timeline, the uptick in economic activity across countries within the region suggests that some Emerging Markets may reopen sooner than Europe and the United States, driving their leadership in expected global economic growth for 2020.

Related ETFs

- The Global X MSCI Argentina ETF (ARGT)

- The Global X FTSE Southeast Asia ETF (ASEA)

- The Global X MSCI China Large-Cap 50 ETF (CHIL)

- The Global X DAX Germany ETF (DAX)

- The Global X MSCI Greece ETF (GREK)

- The Global X FTSE Nordic Region ETF (GXF)

- The Global X MSCI Colombia ETF (GXG)

- The Global X MSCI Pakistan ETF (PAK)

- The Global X MSCI Portugal ETF (PGAL)

- The Global X MSCI Norway ETF (NORW)

- The Global X MSCI Nigeria ETF (NGE)

Click the fund tickers for standard performance data. The performance data quoted represents past performance. Past performance does not guarantee future results.