Pedro Palandrani

Pedro PalandraniFor this post, we interviewed Joe Lowry, also known as “Mr. Lithium,” to get his unique insights and views of the lithium industry. In the Q&A below, we discussed the supply/demand environment, battery technology, challenges and opportunities for companies in the space, and much more.

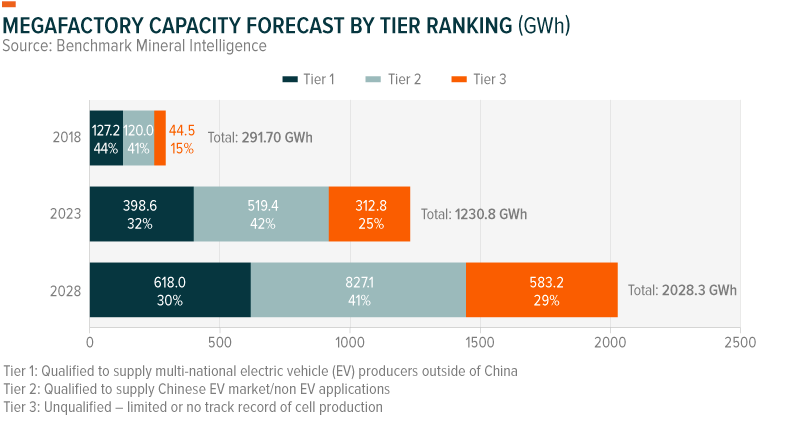

With Tesla’s recent battery megafactory announcement, which is expected to be built in Germany and be the 4th Tesla’s megafactory, Benchmark Mineral Intelligence has now tracked 103 battery plants with a total capacity of 2028 GWh by 2028, up 77% in last 12 months. What does that mean in terms of demand for raw materials like battery quality (BQ) lithium?

All these planned factories will not be built on a timely basis. The total capacity would require 1.6 million metric tons (mt) of battery quality lithium carbonate equivalent (LCE), which the industry is not in a position to do by 2028 given the lack of investment and the fact current BQ capacity is less than 250,000 mt. I continue to be surprised that OEMs and battery producers are blindly expecting a lithium supply miracle while many lithium mining projects can’t move forward due to lack of financing.

Notes: 1 gigawatt hour (GWh) = 1,000,000.00 kilowatt hours (kWh). 2028 GWh in battery plants capacity would equal an annual capacity of over 40 million Tesla Standard Range Model 3s (battery capacity 50 kWh).

You have called 2019 lithium’s “gap year,” potentially spilling over to 2020. Yet, as market dynamics become well understood, will the expected undersupplied environment be the tide that lifts all boats, including smaller/new entrant lithium producers?

The rising tide will benefit the “Big 4” (Albemarle, SQM, Ganfeng Lithium, Tianqi Lithium) plus Livent who are all well-established in supplying the battery quality lithium market. Of smaller companies, only Lithium America’s (LAC) project in the 50/50 Mineral Exar JV with Ganfeng is fully funded and likely to produce battery quality material quickly given both Ganfeng’s involvement and LAC’s team which has some of the best and brightest talent from FMC Lithium/Livent who have executed projects in the past. Orocobre and Galaxy Resources either supply or plan to supply less than BQ lithium (primary grade). Their prices may rise to a modest extent, but likely not much, as low-quality lithium remains oversupplied and third party reprocessors (who turn low grade lithium into battery grade) will have to make a profit in order to invest capital in facilities and make a reasonable return.

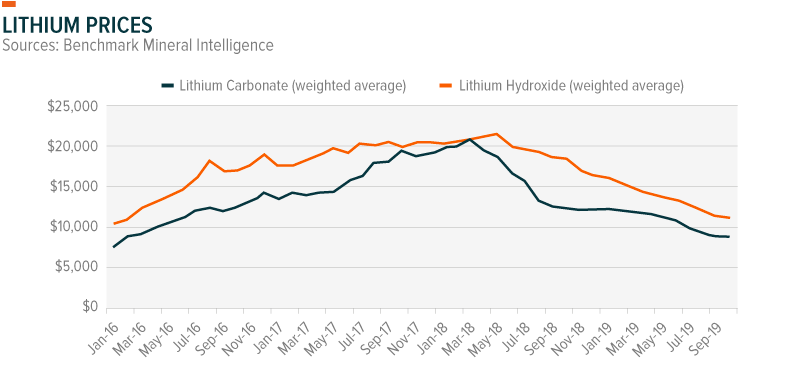

There is a perception that lithium miners don’t offer much pricing transparency, making it hard for analysts and investors alike to differentiate between an apparent oversupply of technical grade lithium, but a balanced or even undersupplied market for battery quality (BQ) lithium. Could you share your insights into the current supply/demand environment and to what degree prices will continue to fluctuate?

The major lithium companies clearly do not support price transparency. The key question is – what is in it for them? As I write this from Tokyo on 11/21 – SQM just reported their 3rd quarter results. BQ lithium shipments to the high-end cathode market in Japan and Korea continue to average above $10,000 per metric tons for lithium carbonate. The low end of the market in China is still at approximately $7,000 per metric tons, but at that price many Chinese converters cannot earn a return, so that level of pricing is unsustainable. Although I am not calling “the bottom” of pricing yet, I believe we are close. I expect prices to be around the current level for up to a year before it becomes obvious that there is insufficient BQ carbonate and hydroxide, and prices begin to move up above $12,000 per metric tons of LCE – what I have called the “new normal” range.

Some suggest that cathode makers have very little lithium inventory. Does this have the potential to cause another period of lithium price increase?

I have not done site audits of cathode makers in China’s raw material inventory, but the destocking phenomena has been well established via conversations with key players in China. Even the oversupply camp has noted this situation. Once the price for battery quality material begins to rise, both natural market growth and restocking will put pressure on price quickly; however different from the last time oversupply of poor-quality material/primary grade will create an even greater gap in price between technical grade and battery quality lithium. Significant “reprocessing/upgrading” capacity will ultimately be required to keep battery quality supply adequate. The lithium industry has always relied on lot selection in the past when battery demand was less than half of total global demand, but since 2017 when battery-related demand exceeded 50% of the market for the first time, degrees of freedom to lot select were strained. By 2025 > 85% of demand will require battery quality. A situation the industry is simply not prepared for.

Note: When lithium is produced normally, companies put a standard quantity in what is called a lot which is analyzed and prepared to ship. Some lots meet the battery specification others don’t. So, the ones meeting the battery spec are the ones selected.

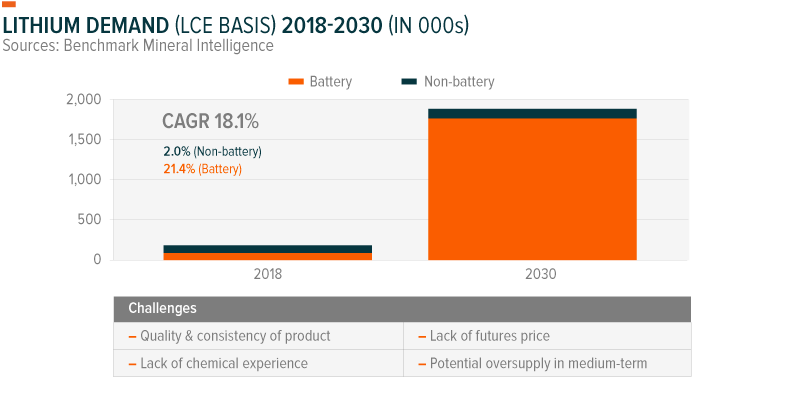

By 2025, lithium carbonate equivalent (LCE) demand is expected to triple to 800,000 mt, rising from 270,000 mt in 2018. In some cases, lithium majors are planning for scenarios where demand exceeds 1 million metric tons. Is the lithium industry ready to supply all that lithium?

No, the lithium industry cannot deliver 1 million metric tons of mostly battery quality lithium by 2025. It is already too late for that. There is no shortage of lithium resources but there is a shortage of investment. In my opinion the industry needs at least $12 to $14 billion invested as soon as possible to meet 2025 demand.

Where will the capital come from? OEMs, battery manufacturers, bio oil/energy companies, other miners?

A great question that I can’t answer. The majors can self-fund, but others require outside capital that simply is not flowing to smaller company projects in a meaningful way, with the exception of Ganfeng’s investment in LAC.

By looking holistically at the industry’s supply chain, pundits have called it the ‘China Moment.’ Is the industry dependent on China today, or is it a more global story?

Look at where the high end of the cathode/battery market is – Japan and Korea. Combined imports of LCE in these two countries will increase by over 25,000 mt of LCE in 2019. In a total market that was only 270,000 mt globally last year, this is significant growth. China is a major story, but not the only one. Major growth is also coming from Europe, North America, etc. that will largely be supported by Tier 1 battery makers outside of China.

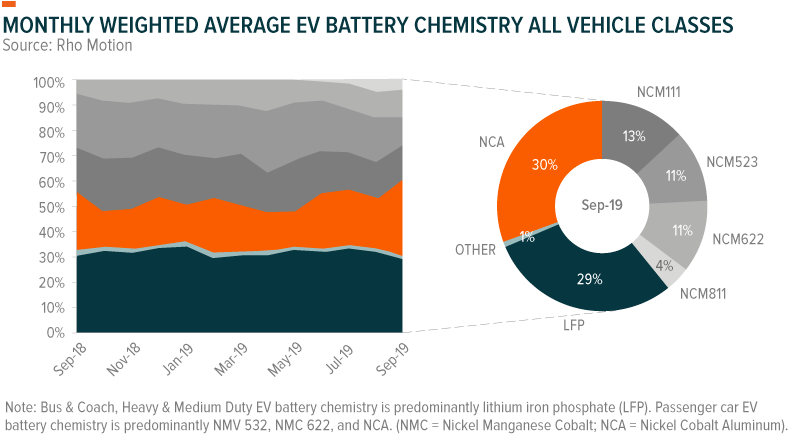

Can you please explain how the lithium battery technology is evolving? NMC 811 is being adopted slower than expected. Are NMC 622 and NMC 532 the flavors of day?

Making NMC 811 is technically more complex, which has become obvious. Yes, in NMC something less than 80% nickel is the flavor of the day. Some is NMC 532 some is NMC 622 and some is higher than 60% nickel but less than 80%.

Note: NMC 811 or lithium ion batteries with a cathode composition with 80% nickel, 10% manganese, and 10% cobalt, are new generation batteries that can generate greater energy density and deliver more range to vehicles. These batteries are known as nickel-rich batteries because they have more content of nickel and less cobalt and manganese. The battery industry has been improving NMC technology by steadily increasing the nickel content in each cathode generation (e.g. NMC 433, NMC 532, NMC 622, and NMC 811).

Definitions

Battery Megafactories: A term coined by Benchmark Mineral Intelligence that describes the surge of new, huge lithium-ion battery plants, usually larger than 1 GWh.

Battery Quality Lithium: A free-flowing, odorless white powder with guaranteed 99.5% purity and a relatively fine particle size. Battery grade product is a superior purity grade product for use as a precursor in making critical battery materials.1

Technical Grade Lithium: Lithium with less than 99% purity. Technical grade product is useful in the manufacture of glass, frits, other ceramics and a variety of specialized applications.2

Lithium Carbonate Equivalent (LCE): a term used in the lithium industry for the first commonly traded Lithium intermediate in the value chain.

Related ETFs

LIT: The Global X Lithium & Battery Tech ETF (LIT) invests in the full lithium cycle, from mining and refining the metal, through battery production.

DRIV: The Global X Autonomous & Electric Vehicles ETF (DRIV) seeks to invest in companies involved in the development of autonomous vehicle technology, electric vehicles (“EVs”), and EV components and materials. This includes companies involved in the development of autonomous vehicle software and hardware, as well as companies that produce EVs, EV components such as lithium batteries, and critical EV materials such as lithium and cobalt.