Global X Research Team

Global X Research TeamIn our Q1 MLP Insights piece, we focused on the long term outlook for Master Limited Partnerships (MLPs). We noted that asset-heavy industries such as pipelines tend to suffer amid adverse business conditions, but are also real assets, like real estate, which can be resilient over the long term and have the potential to pay attractive yields to investors while they wait for a recovery.

In this piece, we will shift gears to focus on near term trends in the midstream MLP space, specifically by looking at midstream MLP fundamentals and current drivers of MLP price movements.

- Midstream MLP fundamentals were robust in 2015, with strong adjusted EBITDA and distribution growth

- Despite the strong fundamentals, MLPs are increasingly being driven by oil prices

- The disconnect between fundamentals and daily price movements might create value opportunities for long term investors

MLP Fundamentals

Following heavy losses and heightened volatility in 2015, investors eagerly awaited Q4 earnings reports in February 2016 to provide insights into the financial condition of MLPs. The reports also gave us a chance to see a full year of performance for MLPs in an environment where the average price of oil was 35% lower than the year prior1.

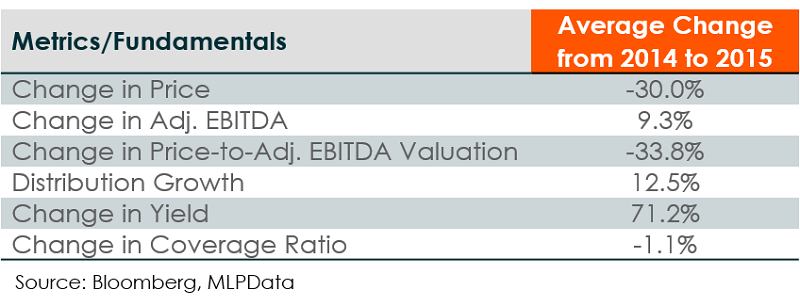

Below is a table of the average changes from 2014 to 2015 in various metrics and fundamentals for the 20 large cap midstream MLPs which are the current constituents of the Solactive MLP Infrastructure Index.

The average large cap midstream MLP sold off 30% despite a solid 9% improvement in adjusted EBITDA. Of course, this improved both the numerator and denominator of the price-to-adj. EBITDA valuation metric, resulting in valuations that were a third lower than 2014. Also of note, these MLPs increased distributions on average by over 12%, with only a minimal negative impact in their ability to cover these distributions. Coverage ratios in 2015 for this segment still remained a healthy 1.25 on average.

In short, midstream MLPs got cheaper, while adjusted EBITDA and distributions grew. For value investors, these results are quite attractive and perhaps what led to value-hunting institutions like Berkshire Hathaway, Jana Partners, and Appaloosa Management all initiating positions in midstream infrastructure companies and MLPs in their latest 13f filings2.

Despite the strong earnings and falling valuations, many investors fear what will happen in the medium term if this low oil price environment persists for a few more years. The longer oil remains cheap, the more likely producers could go out of business or reduce production, resulting in less volumes for midstream MLPs to transport, store or process.

MLP Correlation with Oil

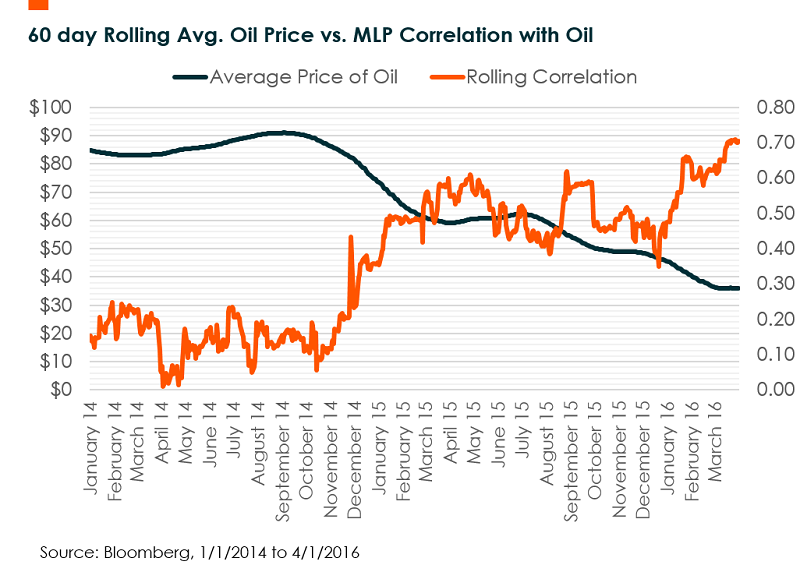

These oil price-related fears are increasingly dictating the price movements of MLPs. In the chart above, we compared the rolling 60-day average price of oil with the rolling 60-day correlation of midstream MLPs to oil. The chart depicts a trend of rising correlations between MLPs and oil, which is currently peaking around 0.70. In addition, during each period of falling oil prices, correlations spiked, showing that the lower the price level, the more sensitive MLPs become to oil. This can be considered the contagion effect, where historically uncorrelated assets become more correlated during stressful time periods. MLPs are not the only asset class to experience this phenomenon, as we saw at the beginning of the year that bank stocks became increasing correlated to oil due to the spillover impact of potentially bad energy loans.

While rising correlations are a source of frustration for many investors who invested in MLPs as a diversifier to other energy investments, it can also present new opportunities. For example, those looking for ways to bet on oil prices could either buy oil futures, which are currently in contango and have a –14% annual roll yield3, or invest in MLPs yielding 9.2%4. All else equal, in a flat oil market where neither the price of oil futures nor MLPs move, the MLPs would outperform the futures by 23%. In addition, value-focused investors looking to buy assets on the cheap could wait for a short term pullback in oil prices (and therefore likely MLPs) to buy into MLPs, which are real assets with a long term operational lifespans and have demonstrated robust earnings.