Global X Research Team

Global X Research Team“Risk-off” remains a prevailing sentiment in 2023 following the notable declines in equity and fixed income markets in 2022. Through Q1 of 2023, flows into U.S.-listed fixed income ETFs doubled their equity ETF counterparts, perhaps a result of investors looking to lower equity betas and risk levels within their portfolios.1 Within the ETF marketplace, another way investors can potentially modify systematic risk in their portfolio is to implement a defensive options strategy on an asset or index, such as an options collar. In this piece, we highlight the growth of this type of strategy in the U.S. ETF market and explore different styles of potential implementation.

Key Takeaways

- We expect growth in options collar strategies in ETFs to continue as investors prioritize risk management in these difficult market conditions.

- Options collar strategies for capital appreciation can be constructed differently, resulting in distinct risk and return trade-offs, both of which should be evaluated based on investor objectives.

- Premium costs for collar strategies can be adjusted based on preferences for the level of tail risk exposure and upside potential desired. In this post, we evaluate two common collar strategies, net debit collars and zero-cost put spread collars, to show the profiles of each.

Options Collar Strategies in ETFs Rise in Popularity

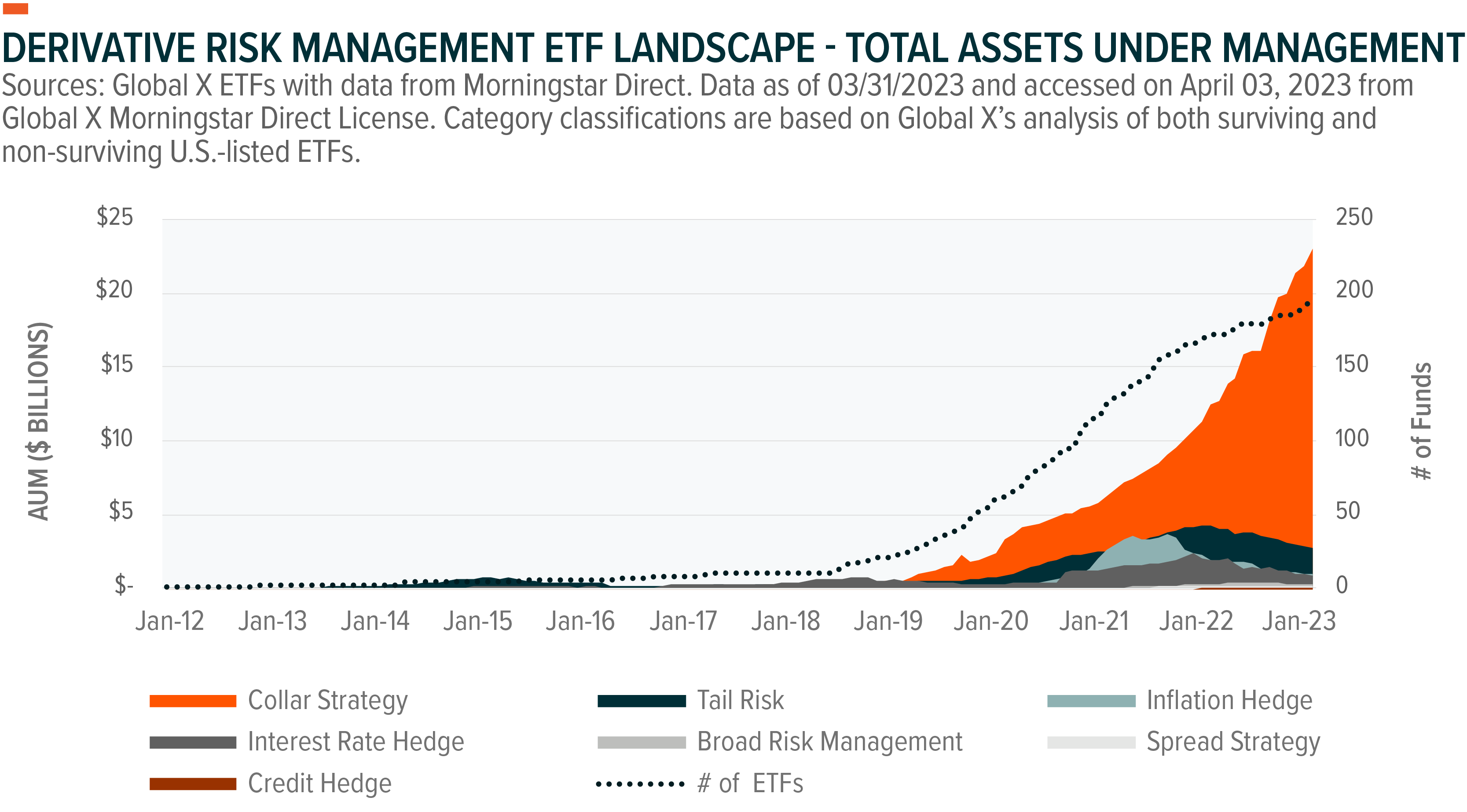

Collar strategies involve creating range bound return outcomes, often through combining a short call option position with a long put option position. Among derivative-based risk management strategies, collar strategies have had the most traction with investors. Assets under management (AUM) for options collar strategies in the ETF wrapper totaled $23 billion as of the end of March 2023, followed by tail risk strategies, a derivative-based strategy that seeks to provide a hedge against significant downside losses on a chosen asset, at just $2.7 billion.2 Historically, collar strategies have been used to manage equity or fixed income betas more efficiently by sacrificing a level of upside participation on the reference asset or index with the goal of capital appreciation or income potential.

In this risk-off market environment, investors are starting to gravitate towards these strategies more than ever. The chart below shows that from January 2022 to January 2023 assets doubled in this segment of the ETF ecosystem. In our view, this growth suggests investors’ increasing comfort with accessing the options market in an effort to achieve a more defined level of risk and reward.

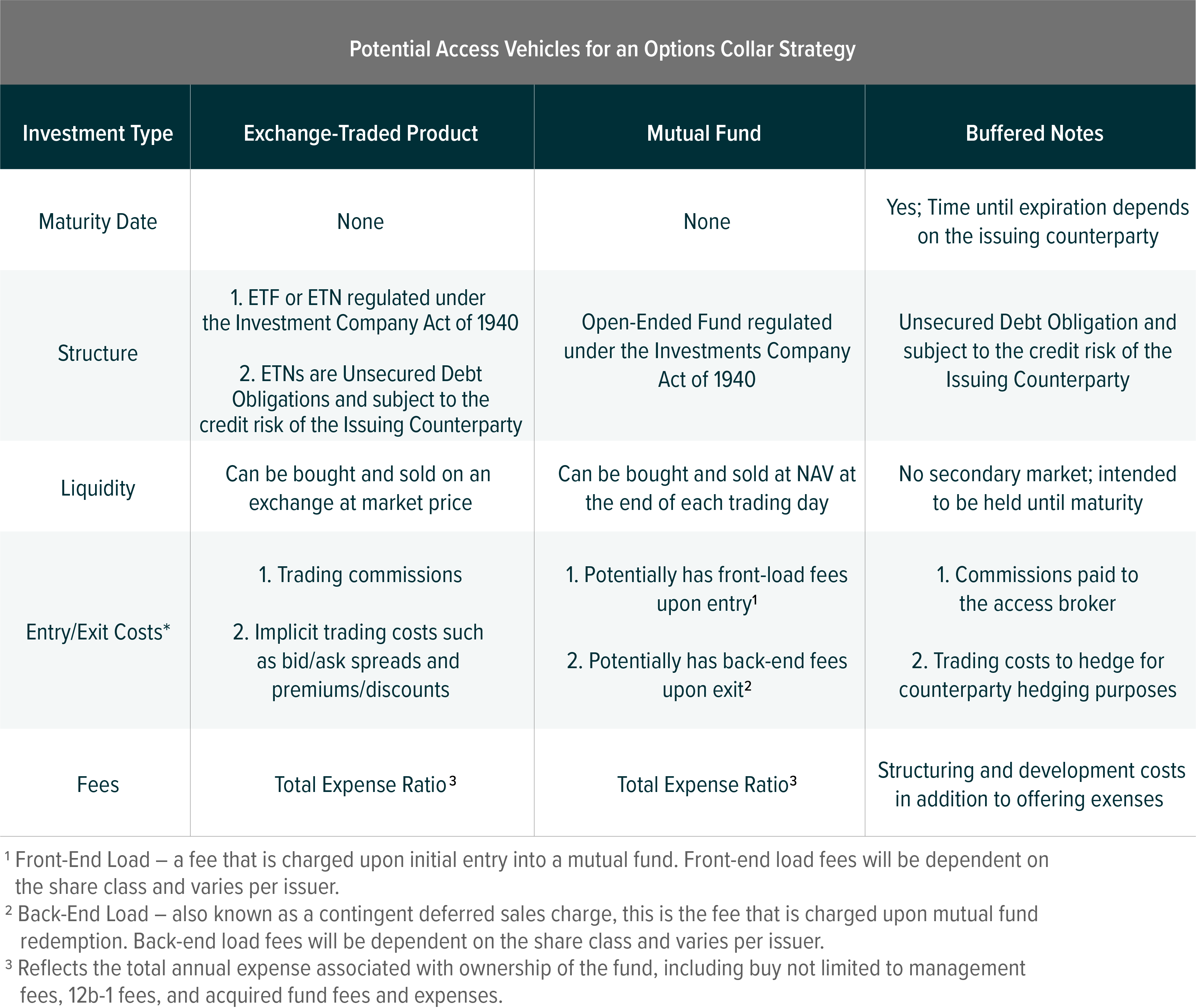

Derivative-based funds and products have historically been implemented in investment vehicles that are not ETFs. Mutual funds in addition to buffered notes, a type of structured product issued by a large bank, have a longer history within this segment of the asset management industry. ETF issuers have recently launched similar strategies, largely within the past 5 years, to provide investors another avenue of options market access.

Not All Collar Strategies for Capital Appreciation Are Structured the Same

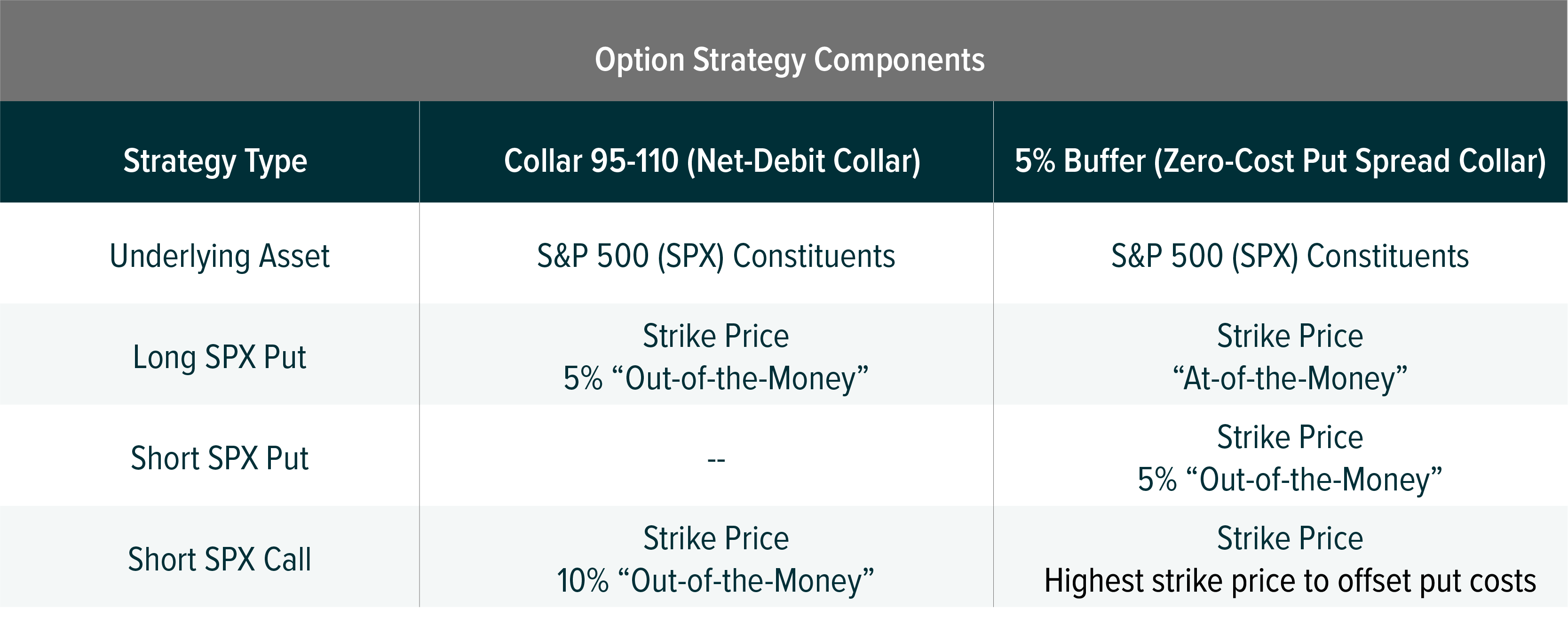

Collar strategies can be created with different combinations of call options and put options to provide a specific exposure. Key considerations when implementing or investing in an investment vehicle with such a strategy include the strike price, the time until expiration, and the reference asset of the options used.

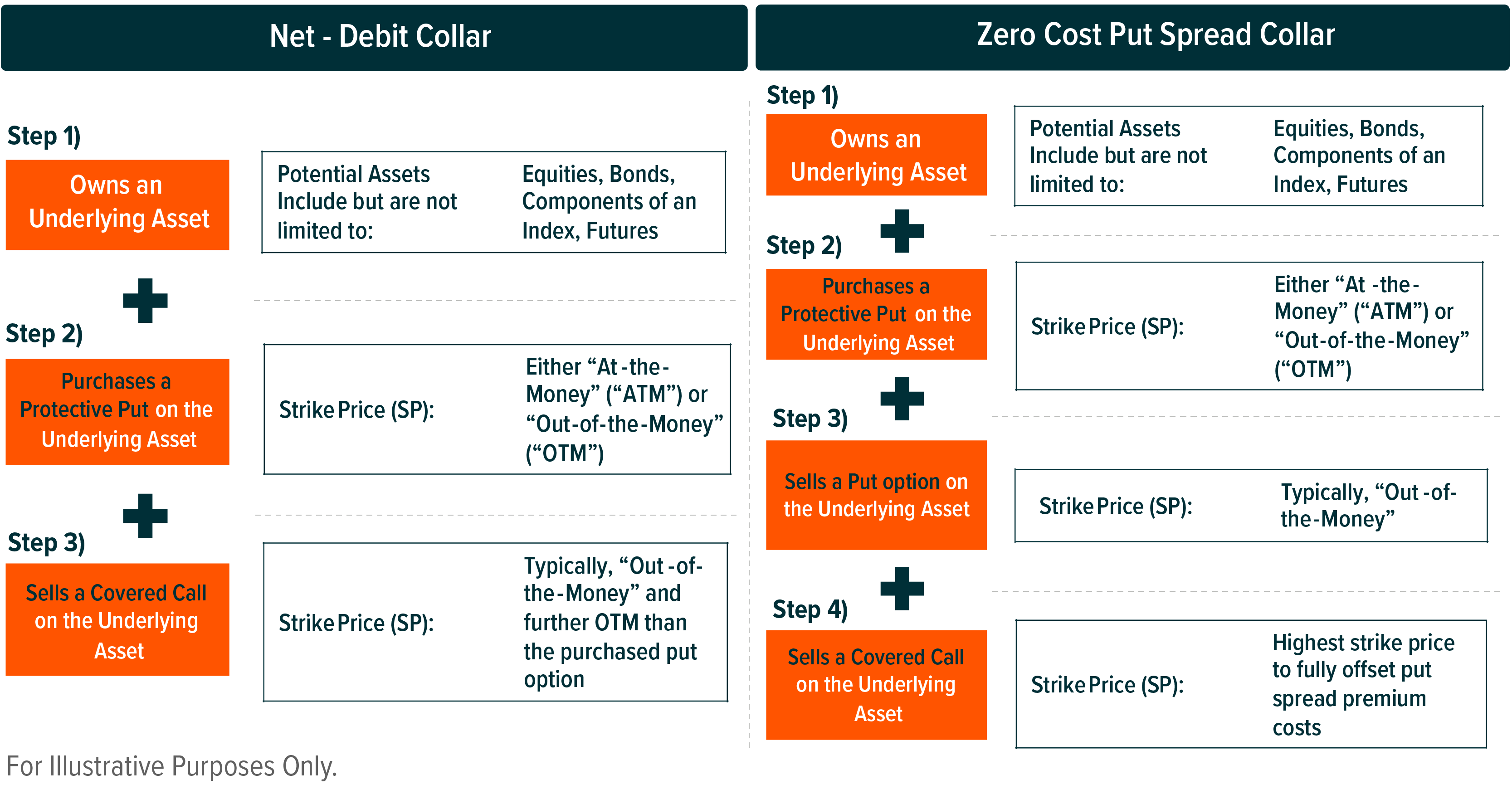

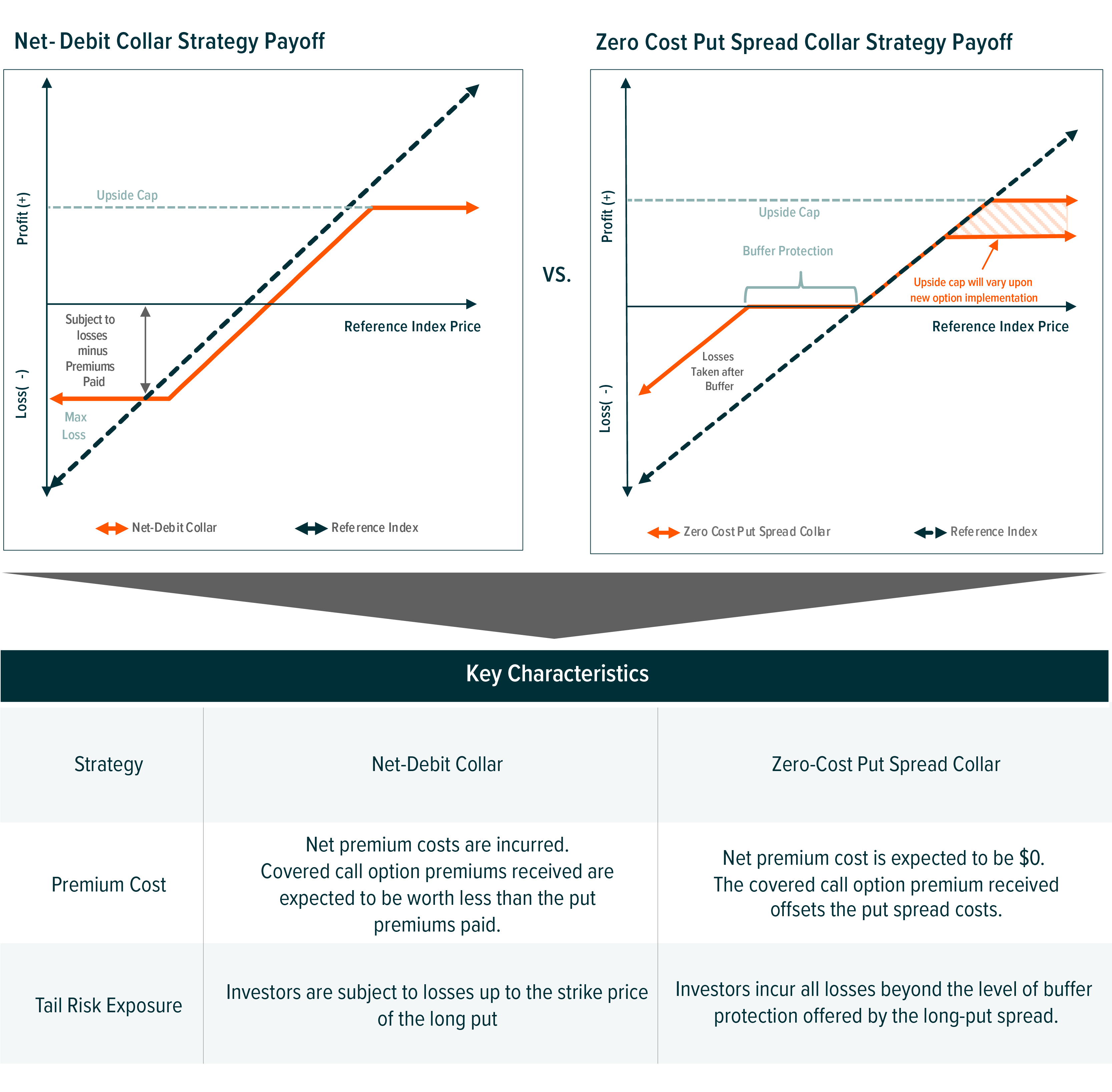

While there are numerous way to implement collar strategies, we will discuss two. One type of options collar is a net-debit collar strategy, which seeks to provide a floor, or max loss, on a specified reference asset. Another iteration of an options collar is a zero-cost put spread collar, an options strategy that seeks to provide a buffer – but not a floor – on the reference asset’s downside, in which the investor is protected for a specified level of reference asset downside. Both are constructed by combining calls and puts in a different manner. A key difference between a net-debit collar and zero-cost put spread collar is that as the name would imply, net debit collars involve a net premium cost outlay to investors to implement whereas zero-cost collars are designed to not have a net premium cost outlay.

For net-debit collars, the premium cost each time new options positions are initiated stems from the fact that the premiums received from the sale of the call option do not fully offset the costs of the purchased put option. However, by implementing this type of collar, if the options overlay is held until the options expire, there is a max loss on the reference asset minus any premiums paid for strategy construction. This floor can help alleviate some tail risk in a portfolio.

Zero-cost put spread collar investors receive buffer protection relative to the reference asset and take any losses beyond the strike price of the sold put option. However, as the strategy is designed to enter contracts resulting in zero net premiums, the strike price of the call – and therefore the upside cap – will vary upon each option reset.

Collar Strategy Example Demonstrates Risk and Reward Trade-Offs

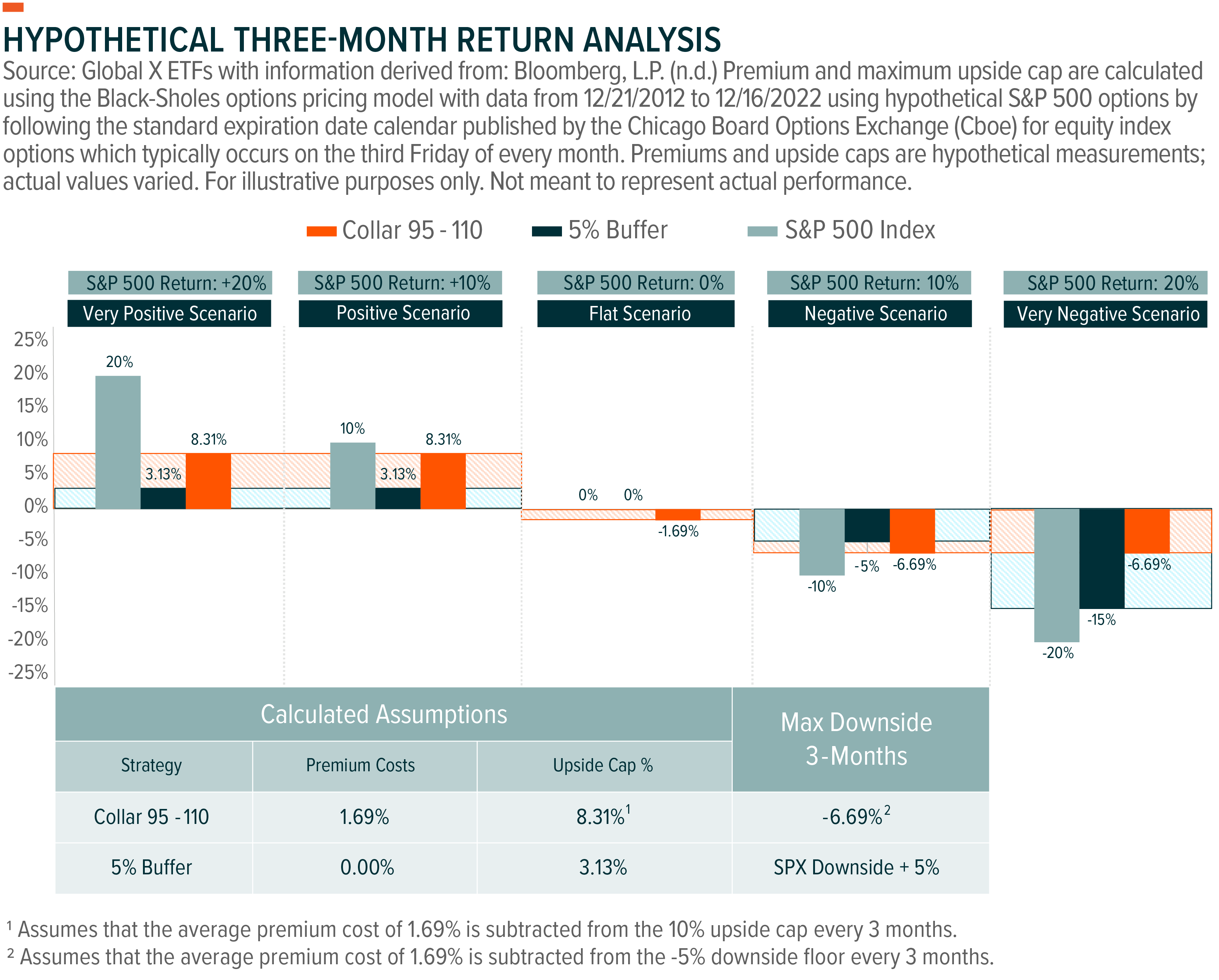

To demonstrate the key characteristics of each aforementioned options collar strategies, we show a hypothetical scenario analysis with an example of each. The hypothetical net-debit collar owns the components of the S&P 500 (SPX) while purchasing a 5% “out-of-the-money” (“OTM”) put and selling a 10% OTM covered call. The other type also owns the components of the SPX while selling a covered call at the highest strike price possible to offset the costs of the established 5% put spread. The final results demonstrate how terminology such as “buffer” and “floor” do not mean the same thing and differentiated investment outcomes are likely.

We show the results below and detail the impacts of each strategy’s options components. The assumptions, in which some are calculated, are as follows:

- For collar 95-110, the calculated average net premium cost is 1.69%.3 Therefore, we account for these premium costs when calculating maximum upside and downside. Premiums will vary with market conditions.

- In a 5% Buffer strategy, the calculated average upside cap is 3.13%.4 Upside cap will vary with market conditions.

- We assume both strategies utilize S&P 500 (SPX) index options with a time until expiration of three months, rolling their options portfolios on the third Friday of every third month.

- S&P 500 returns are over the same three-month period as the options’ terms.

- No dividends were received from the S&P 500 constituents.

Very Positive (SPX +20%) and Positive (SPX +10%) Scenarios: In an S&P 500 bull market, based on these positive scenarios, the collar 95-110 strategy may provide a higher level of upside, relative to the 5% buffer strategy, due to having a higher upside cap from contract initiation minus any premiums paid. Implied volatility is likely falling during equity bull markets, potentially lowering put premium costs for both collar strategies. However, with a history of smaller average upside caps, the 5% buffer strategy may be unable to provide the same level of upside participation.

Flat Scenario (SPX 0%): When the S&P 500 index is flat, the 5% buffer strategy, in addition to the reference index, are expected to outperform collar 95-110 due to the premium cost difference. Typically, the closer the strike price of the contract sold is to the price level of the asset upon contract initiation, the higher the potential is for a higher premium. Since collar 95-110 sells a call further OTM than the purchased put, it’s always expected to incur a premium cost, which decreases the returns.

Negative Scenario (SPX -10%): The 5% buffer strategy is expected to outperform a collar 95-110 strategy if the reference index modestly declines due to the premium cost difference. In this scenario, the S&P 500 fell -10%. This was enough for collar 95-110 to outperform the S&P 500, however, the strategy underperformed the 5% buffer strategy by the premium costs.

Very Negative Scenario (SPX -20%): However, during severe market declines, when the S&P 500 moves substantially beyond the buffer protection offered by the 5% buffer strategy, the collar 95-110 strategy is expected to outperform due to the floor provided by its long-put option position. This demonstrates the higher level of tail risk associated with a zero-cost put spread collar strategy. Implied volatility is also expected to rise. If this also coincides with rising put option demand relative to calls, higher net-debit premium costs for a collar 95-110 strategy are expected, however, the extra cost may be worth it relative to the zero-cost put spread collar implemented by the 5% buffer strategy.

Conclusion: ETF Industry Offers Compelling Risk Management Capabilities

U.S.-listed ETFs have $6.93 trillion in total AUM, and as this market expands, it continues to offer investors new ways to help them manage risk, pursue a level of capital appreciation, or both.5 Derivative-based strategies are a part of this growth, with the rise of collar strategies playing a major role. That investors can implement options strategies with ETFs indicates the industry’s growth. However, with these strategies more prevalent, it is important that investors understand both the potential benefits and the risks of options strategies tailored for capital appreciation and rangebound return profiles.

Related ETFs

QCLR – Global X Nasdaq 100 Collar 95-110 ETF

XCLR – Global X S&P 500 Collar 95-110 ETF

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.