Michelle Cluver

Michelle Cluver David Beniaminov

David BeniaminovThis month we will be dissecting the dividend discount model (DDM), its various uses, and how higher yields impact the intrinsic value of equity valuations. This piece will be the first of a series where we examine the impact of a higher yield environment on various fundamental and technical equity factors.

First, we will go through defining the equation that creates the DDM, covering each variable and how it interacts with the rest of the equation. Then we will discuss how higher yields impact equity intrinsic values, as the risk-reward trade off becomes more important with higher rates. Finally, we will translate this information to the sectors of the economy with our monthly sector views.

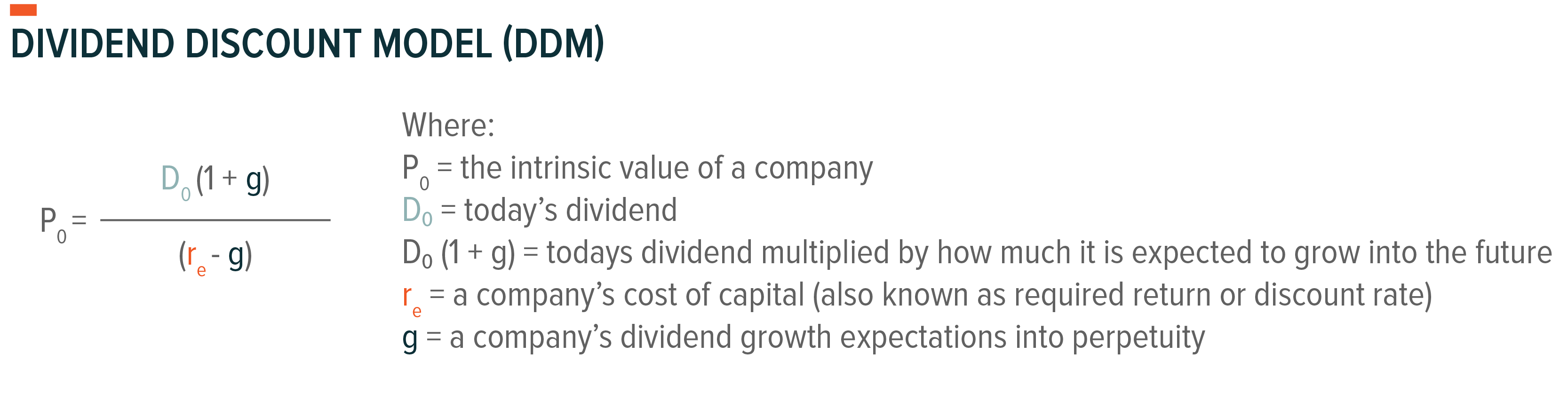

First, let’s start by introducing the DDM formula and then we’ll explain what goes into it. The equation itself is below.

The goal of the DDM is to quickly and easily utilize available resources of an asset to understand what the intrinsic value of that asset is based on certain market and company expectations. It values a company as the sum of all its future dividends discounted back to the present. The discount rate (re), or individual company’s cost of capital, has a positive relationship with interest rates. Meaning as interest rates rise, so does the cost of holding a security, assuming stable growth (g).

The first main component of the formula is the numerator which is made up of today’s dividend multiplied out by the growth of that dividend one period into the future. For example, if a company pays a dividend of $2 today, and has a growth rate of 5% for their dividends then D0 = $2, while D1 = $2(1.05) = $2.10. The second main component is the denominator which is the difference between a company’s required return (also known as discount rate or cost of capital) and its growth rate. For example, let’s assume the company we just mentioned that pays a $2 dividend today growing at 5% has a cost of capital of 10%. Its denominator will be the difference between the required return of 10% minus the growth rate of 5%, which is 5%.

How does this all relate to valuations? Despite the DDM seeming like an overly simplified way to value a security, it carries an exceptional amount of weight when performing valuation analysis on equities due to its widespread use. Because the formula can be quickly calculated, the inputs can be manipulated and adjusted to stress test various scenarios with ease. So, let’s bring together the example mentioned above.

This means the intrinsic value of a company is $42 given its $2 dividend today, growth expectations of 5%, and a cost of capital of 10%. If this company is trading in the market for more than $42 then it is overvalued and should be sold, if it is trading for less than $42 then it is undervalued and should be bought.

Now, if the required return component of the equation rises without expectations of higher company growth, then the difference between the two variables in the denominator widens, reducing the company’s intrinsic value. Let’s assume that interest rates are expected to rise which could raise the discount rate from 10% to 12%.

A 2% rise in the discount rate, which doesn’t seem significant, revalued the company from $42 to $30, a drop of 28.6%. That’s significant and can help shed light on why January has been such a tough month for equity markets.

Astute investors are likely thinking of what happens to equities that don’t pay a dividend. Like many companies that are in their growth stage, these companies reinvest their earnings back into their business. As mentioned earlier, the DDM values a company as the sum of all its future dividends discounted back to the present. So, a large portion of the value of these growth focused companies comes from a distant future, which carries a lot more unknown than a company that is currently generating positive cash flow. As the saying goes, ‘a bird in the hand is worth two in the bush,’ a dividend today is worth more than the promise of more dividends tomorrow. This is why the growthier technology related names are called ‘long duration’, and similar to fixed income, assets with long durations are more sensitive to higher interest rates.

That brings us to today, where investors are faced with the economic landscape of higher policy rate expectations from the Federal Reserve (Fed) which translates to higher discount rates, which leads to lower valuations. If company growth remains stable, then the expectation could be that value focused sectors and companies will lead in performance while their growth counterparts could flounder.

For our current views please reference the sector table below.