Michelle Cluver

Michelle CluverThis piece is part of a larger whitepaper, Investing in Thematics From a PM Perspective.

In 1996, Bill Gates published an essay entitled “Content is King” in which he detailed how content would capture the lion’s share of profits created by the burgeoning internet. His view hinged on users becoming personally involved with the content that they consume. Gates proved prophetic, as digital experiences grew to influence all walks of life economically, politically, and, of course, socially. As an investment theme, we believe Digital Experiences, including Social Media and Video Games & Esports, offers compelling opportunities because of the ongoing quest to monetize the attention of content consumers as the world becomes increasingly digital.

Key Takeaways

- Social media and video game technology combine to increase user retention and engagement across social and gaming platforms. As competition in the digital economy intensifies, we expect investment in the Digital Experiences theme to grow alongside it.

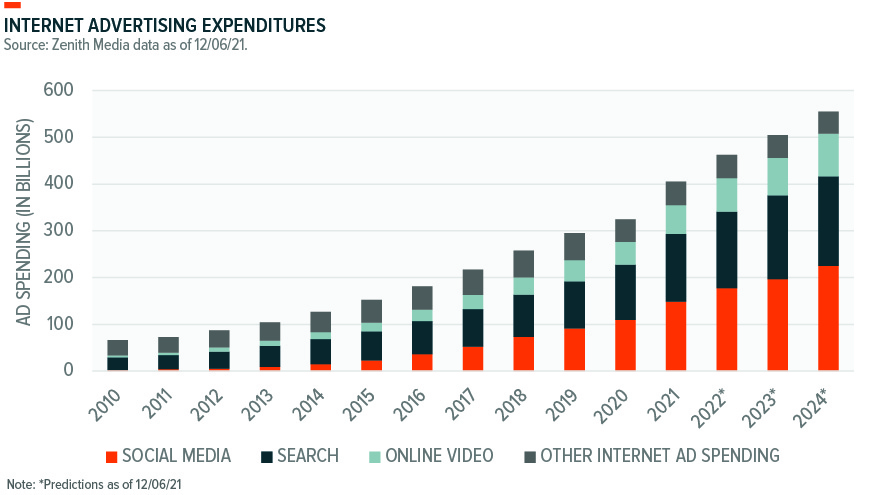

- Total social media advertisement spending is expected to reach $177 billion in 2022, overtaking television as the largest advertising market.1

- Mobile gaming is the largest and fastest growing video game segment, boosted by widespread smartphones adoption and readily accessible casual, free-to-play games. Revenues increased 7.3% in 2021 to reach $93.2 billion2 and is expected to grow to $218.7 billion by 2024.3

Why Social Media and Video Games & Esports are Such Powerful Forces

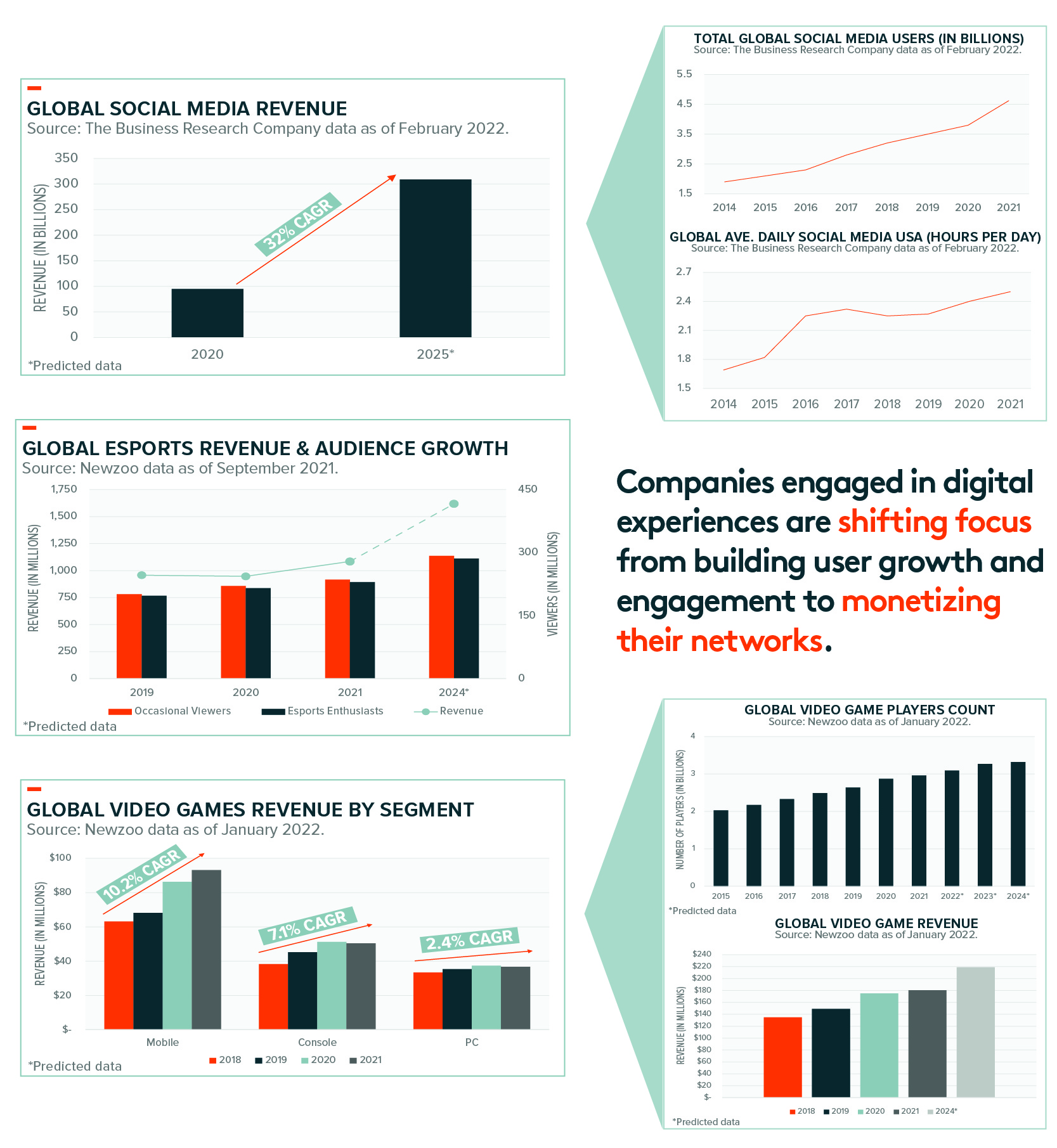

Digital Experience platforms boast large user bases. Today, more than half of the global population (7.87 billion people) use social media.4,5 Video games reach a slightly smaller portion of the global population, with over 40% playing video games in some form.6 Historically, user growth was the main method of expansion for Digital Experience firms, but now they’re shifting towards increased engagement and monetization.

Maximizing monetization

Social media platforms now focus on maximizing the revenue generated from each user. One way they do that is by selling more ads for more dollars. In 2021, global social media advertising revenue reached $148.8 billion, equivalent to 20% of total global ad spending, or about a third of all online ad expenditures.7 Also, platforms are developing innovative new technologies, such as integrating in-app purchases and cash transfers, enabling augmented and virtual reality experiences (AR/VR), and more as they search for additional revenue streams. The metaverse, which is more of an emersion experience, and may eventually become a fully formed digital economy, could be the next digital frontier.

Advertisement services company Zenith Media predicts that social media will be the fastest growing advertising channel between 2021 and 2024. Total social media ad spend is expected to reach $177 billion in 2022, overtaking television as the largest advertising market as brands leverage social media to spur further growth in ecommerce.8

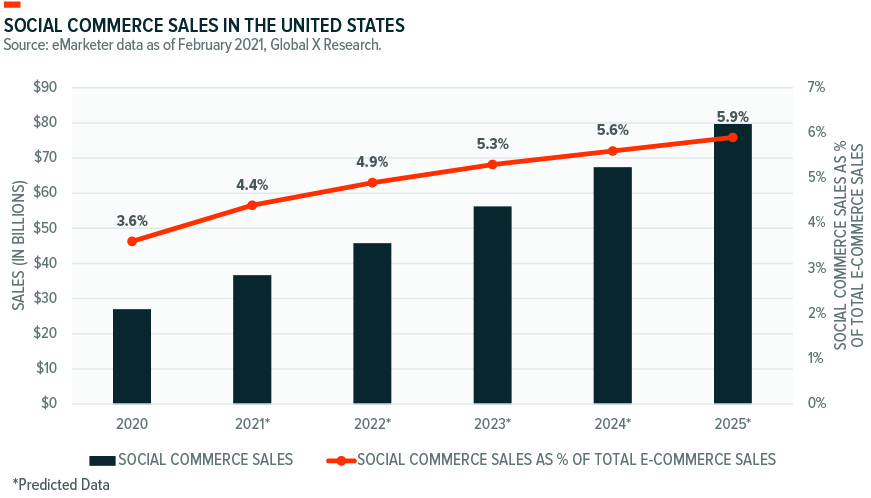

Using social networks for commerce

Combining the visual and curated nature of social media with the ease of in-app purchases, social commerce can help capture customers’ attention and reduce friction in the purchasing process. Eighty-three percent of Instagram users say they discover new products on the platform, indicating the size and scope of the opportunity.9 Social commerce excels alongside influencer partnerships, as adding a known face to marketing efforts can sway consumer purchasing decisions. Among internet users in the U.S. and UK, influencers directly impact the purchases of nearly 1 in 5 social media users.10

Moving into the metaverse

The metaverse, where the virtual world becomes a place to meet, work, and transact, is the next major step for social media. The company formerly known as Facebook, now Meta Platforms, is betting its future on the metaverse. Accessed via virtual reality headsets, such as Meta’s Oculus, the rise of the digital economy within the metaverse is likely to feature new methods of shopping, socializing, and gaming that leverage the latest technologies to create exciting new digital experiences.

Many of today’s metaverse platforms draw inspiration from the video games of the past. Debuting in 2003, Second Life was a virtual world where players could replicate much of their day-to-day lives, designing avatars, communicating, designing virtual objects, and conducting commerce. The game even coined the metaverse’s first millionaire in 2006, an avatar named Anshe Chung belonging to virtual real estate developer Ailin Graef.11 By integrating concepts first explored by video games, the metaverse can optimize features favored by users.

Recurring revenue – downloads, subscriptions and microtransactions

Advancements in graphical technology, such as virtual reality and raytracing, make the digital world richer than ever, enticing more people to become regular consumers of video games. As opportunities for recurring revenue streams attract larger user bases and games reach new levels of emersion, we believe the industry can generate outsized returns over the long run.

In the early 2000s, buying a video game required gamers (or their parents) to go to the nearest retail store. Today, near ubiquitous access to high speed internet means that 83% of total video games sales are digital.12 Digital delivery provides convenient access for consumers with cost benefits to the publisher. Physical distribution requires manufacturing, shipping, packaging, and wholesaling, factors that negatively impact margins. Digital distribution brings the storefront into the living room and puts games just a click away.

Digital distribution also facilitates subscription services. For a low monthly fee, gamers can access hundreds of game titles, ready to play after a quick download. Even though current offerings are largely older intellectual properties, publishers benefit from introducing players to their content.

Just as Netflix disrupted the distribution model for movies and TV shows, cloud gaming could have a similar impact on the video game industry. Cloud games are streamed rather than downloaded locally. The cloud provides access to a broad library of games, playable on a variety of compatible devices, without the need to build out an expensive PC or buy a next-gen console. Newzoo, a games market insights and analytics company, estimates 164.6 million players have already switched to the cloud, paying a collective $1.6 billion to take their games wherever they go. Over 90% of players familiar with cloud gaming have tried it or want to, indicating the size and stickiness of the opportunity.14 The transition to gaming-as-a-service can drive recurring revenue and allow for valuable usage data to be tracked more easily, resulting in targeted ads to big spending players.

For players who want to play games but don’t want to pay, the free-to-play (F2P) video game market is now one of the most popular gaming segments. In F2P, publishers generate revenue via microtransactions that offer players the opportunity to buy skins, weapons, and other digital accoutrements while in the game. By purchasing these aesthetics, players can stand out from their friends and enemies. And these microtransactions add up and are a large revenue driver for the video game industry.

Visualizing the Market Opportunity

Risks to the Digital Experiences Theme

Social media regulation – mental health, data privacy and censorship

Regulatory risk is a consideration for the Social Media theme owing to concerns about children and teens who spend a significant amount of their time online. A large study of Ontario elementary and middle school students reported “poor mental health” in half of respondents who used social media for five or more hours per day. The effects were even stronger among girls, who reported a 29% rate of suicidal ideation.15 At the end of 2021, leaked internal research at Facebook drew similar conclusions. Facebook’s data showed that 32% of teen girls said that when they feel bad about their bodies, the platform made them feel worse. Teens also reported increased rates of anxiety and depression.16

Another risk to platforms is curbs on data privacy. True to their core value of privacy, in April 2021, Apple updated their on-device privacy controls to limit the tracking capabilities of digital advertisers and encourage users to opt out of data sharing.17 The change decreases the accuracy of targeted advertisements while also limiting the ability of advertisers to measure the clickthrough and conversion rates of their campaigns. Consequences of the change were dramatic for social media firms, many of which described substantial negative revenue effects on subsequent earnings calls.

Users generally view online ads as annoying, in that ads get in the way of users and the content that they want to consume. But platforms generate revenue from ads, so finding a balanced level of monetization opportunities is critical. From a video game perspective, games that keep too much content behind paywalls or use microtransactions heavily can frustrate players, and either one can lead to lower platform interaction and revenue generation.

Digital experience platform users keep coming back to these platforms because they enjoy the access to content and the community. As a result, platforms must walk a fine line between monetization and the user experience. Platforms also must consider how censorship, and the perception of censorship, can affect the community and their bottom line. For example, social media websites commonly restrict the reach of unsavory content while while promoting content suitable for general audiences. This practice can particularly affect user perceptions of how platforms present political content.

Pew survey data showed that 73% of adults believe it is likely to somewhat likely that social media sensors objectionable political viewpoints.18 The intended effect of content restriction is a more harmonious experience for users, but it can come at the cost of broader user participation on the platform.

Supply chain disruptions affecting next-gen hardware sales

Historically, the Video Games & Esports theme has been limited by hardware and graphics, or the elements that combine to make a game visually appealing: detail, resolution, and framerate. Today, the video game console space is in transition as a new generation of devices bring enhanced features and more realistic experiences. However, supply of this hardware has yet to meet demand, mainly due to the continuing semiconductor shortage.

Component availability prompted manufactures to reduce sales expectations for the newest consoles while increasing production of last-generation hardware.19,20 These legacy devices use older chip designs and are easier to manufacture, but they lack many of the advanced graphical features that gamers want. The result is extended technological limitations on game developers and new titles. For the newer consoles, the industry continues to be challenged with supply constraints from component shortages and logistics disruptions, which may pose challenges for growth in the near-term.

Thematic intersection with digital experiences

Social Media and Video Games

Video games are now effectively social media platforms that let gamers play and collaborate with one another. Gaming alongside real world and digital friends positively impacts retention rates, especially for max level players who’ve completed a game’s achievement-based content. Higher levels of in-game communication and social relationships are also correlated with player retention levels.21 For companies, social gaming translates into greater engagement and greater monetization opportunities, as peer pressure can prompt additional title purchases.

Video game content can also be a boon for social media companies. Browser-based social network games leverage the communication prowess of social media to prompt users to reach out to their real-world friends for help in the game. Social network games extend a user’s average session duration while directly generating additional revenue by prompting users to view advertisements.

Fintech & Blockchain

The combination of social media and fintech results in new funding solutions that democratize access to capital, such as crowdfunding platforms. Compared to traditional financing methods, crowdfunding, powered by social media network effects, offers a low-fee way to access and raise capital quickly for business ventures or charitable causes. By democratizing access to capital, crowdfunding platforms could help spur innovation and bring disruption to the market.

For video games, the rise in user participation and monetization has been facilitated by digital payments. Using fintech solutions, game titles and microtransactions can be bought with the press of a button, simplifying purchase decisions and increasing sales volumes. Content publishers and platforms will likely reap additional benefit as digital payments become further integrated into virtual worlds. A culmination of fintech integration looks to be non-fungible token (NFT) marketplaces, where blockchain ensures tradable ownership of virtual goods. Such online economies would create earning potential for users, connecting economies and linking digital goods to real-world currency.

Cloud Computing & Data Centers

At the intersection of cloud computing, data centers, and video games is cloud gaming, or the use of remote computing resources to render virtual gaming worlds. Gone are the days when an expensive, high-powered computer or console was necessary for high resolution graphics. With cloud gaming, games can be streamed to a mobile device.

Continued development of cloud computing and the proliferation of data centers will enhance remote gaming experiences. Colocated servers shorten the real-world distance between processing and end users, decreasing latency and lag when split second reactions matter most. Increased compute power enhances the graphical quality available on the go, boosting visual fidelity and user experience. We expect cloud gaming can realize its potential with the continued progression of the Cloud Computing and Data Center themes.

Cybersecurity

As with all digitally focused themes, digital experiences and the platforms hosting such content may be targets for cybercrime. For most websites, a data breach would include personal identifying information such as name, email address, or payment details. Social media is an entirely different animal, as a breach could reveal the most intimate details of a user’s life. A malicious actor gaining access to a user’s files and personal data can have drastic consequences, but add social media access, and that actor can now impersonate the original account. In line with this, robust cybersecurity is essential to moving digital experiences forward, potentially even into the metaverse.

Digital experiences in a portfolio context

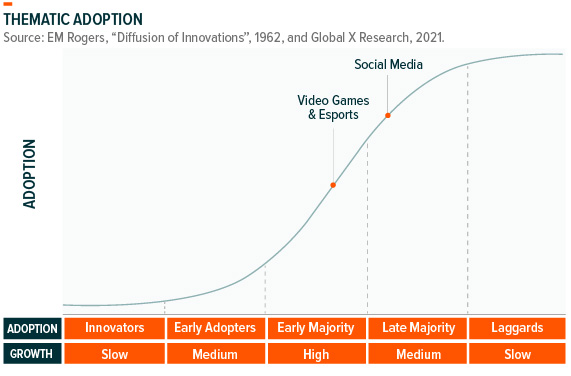

The Digital Experiences theme represents the attention economy and the various forms of new media vying for user engagement. Social Media is the most mature theme within our coverage, as its widescale global adoption places it within the Late Majority phase. Social media’s growth is not at an end stage, rather it’s shifting from account growth to user monetization. Conversely, the Video Games & Esports theme is shifting into the latter half of the Early Majority phase as user adoption increases and consumption of digital experiences deepens.

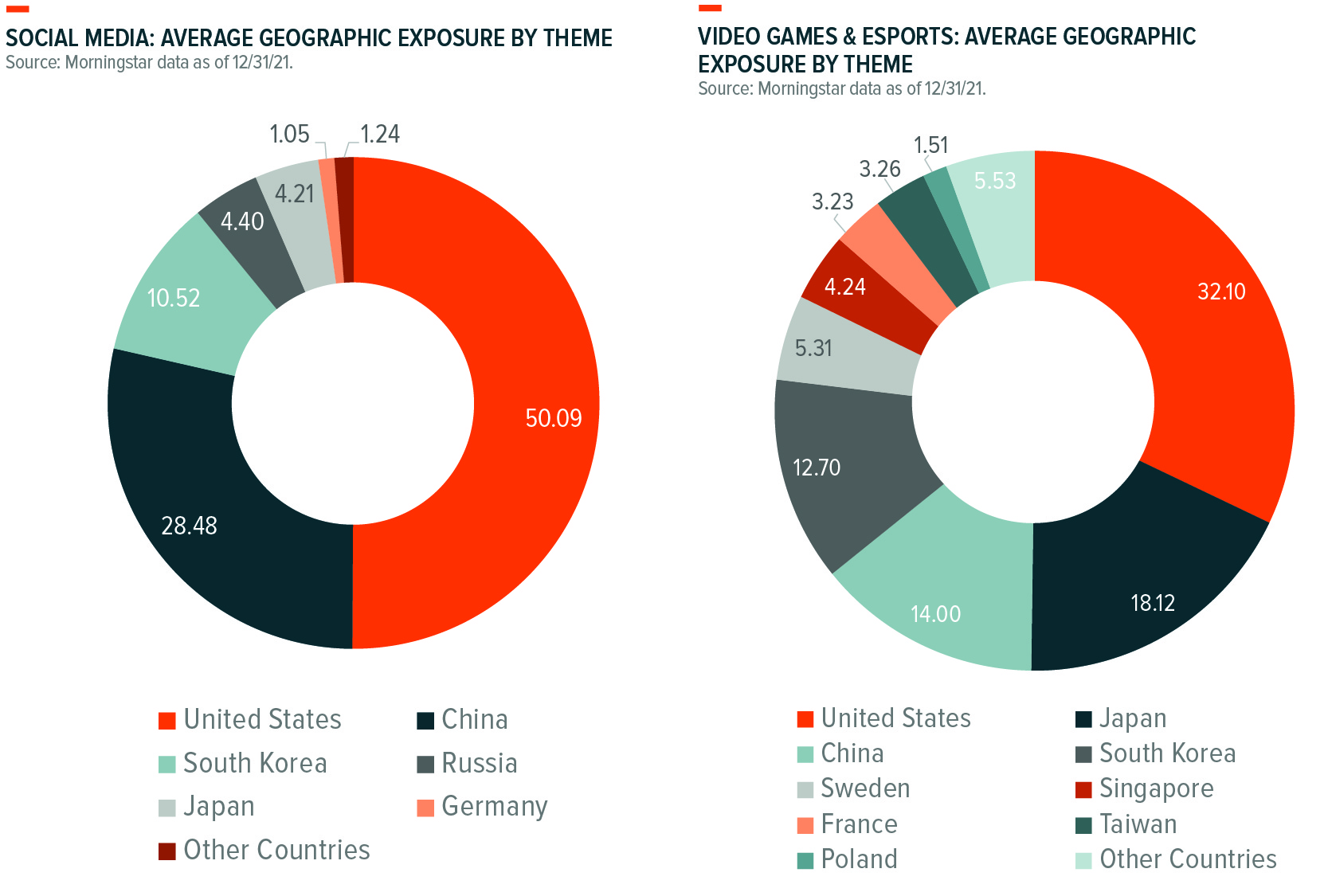

The companies that comprise the Digital Experiences theme are global and positioned to benefit as thematic adoption rises across the world. The charts below break down the geographic exposure of the largest Digital Experiences thematic ETF products. We believe there is ample innovation occurring outside of the U.S. and that limiting exposure to the U.S. will exclude key players, to the detriment of investors over the long term.

In our view, thematic equity should be targeted, using screens to ensure that the underlying companies provide the desired exposure. This pure play focus minimizes overlap between themes while also differentiating the exposure provided by the theme relative to broad beta products.

We conducted an overlap analysis between Digital Experiences thematic ETFs, the S&P 500, MSCI ACWI, and XLC, the Communication Services Select Sector SPDR Fund. We found that overlap by weight for Social Media was 3.6% when compared to the S&P 500, 2.9% vs. the MSCI ACWI, and 21.3% vs. XLC. Higher sector fund overlap levels would be expected for a theme in the Late Majority phase, as Social Media firms have grown to dominate their segment of the economy. Video Games & Esports scored lower on broad beta and sector indexes, 2.4% when compared to the S&P 500, 2.4% vs. the MSCI ACWI, and 8.8% compared to XLC.22 These low levels of overlap with broad indexes reflect the benefits of thematic exposure, as accessing the Video Games & Esports theme requires intentional positioning.

Digital experiences are ubiquitous today. Social media has become a core segment, influencing conversations, culture, politics, and many other facets of society. And video games are mainstream, with more than two-thirds of Americans playing.23 Now that adoption levels are high, Digital Experience-focused companies are targeting monetization, leveraging the network effects of their platforms and communities to maximize their growth potential. They say that “content is king,” and as we expect digital experiences to reign long into the future, we believe that it is important to position portfolios to capture the growing benefit of this maturing theme.

Note: Includes the sole social media ETF and the largest four video games & esports ETFs according to our thematic classification. All Thematic ETFs weighted the same.

How To Access Digital experiences

The graphic below identifies U.S. listed ETFs that provide direct exposure to the Digital Experiences theme through Social Media and Video Games & Esports technology. There is only one U.S. listed ETF that provides direct exposure through Social Media technology. Pure play ETF exposure to Social Media is unique due to large overlap with the Communication Services sector.

Read the next section of the Thematic Investing Whitepaper on the Fintech (FinTech & Blockchain) theme.