Global X Research Team

Global X Research TeamAlong with Turkey, Greece represents another, yet arguably less hairy, election-year story within emerging markets (EMs). After a recent visit to Athens for management meetings, channel checks, and to prepare our strategies for various scenarios, we left with the view that Greek companies are well positioned for 2023.

Key Takeaways

- After years of volatility, Greek equities showed resilience in 2022 and seem well positioned for the remainder of 2023.

- Unlike many other countries, Greece appears to have its foot on the gas, driven by a rebound in tourism, years of underinvestment, and Recovery & Resilience Funds from the European Union.

- Politics will likely play a key role this year, given upcoming presidential elections. Victory for the incumbent New Democracy party could boost investor sentiment and potentially lead to an upgrade in the country’s credit rating to investment grade.

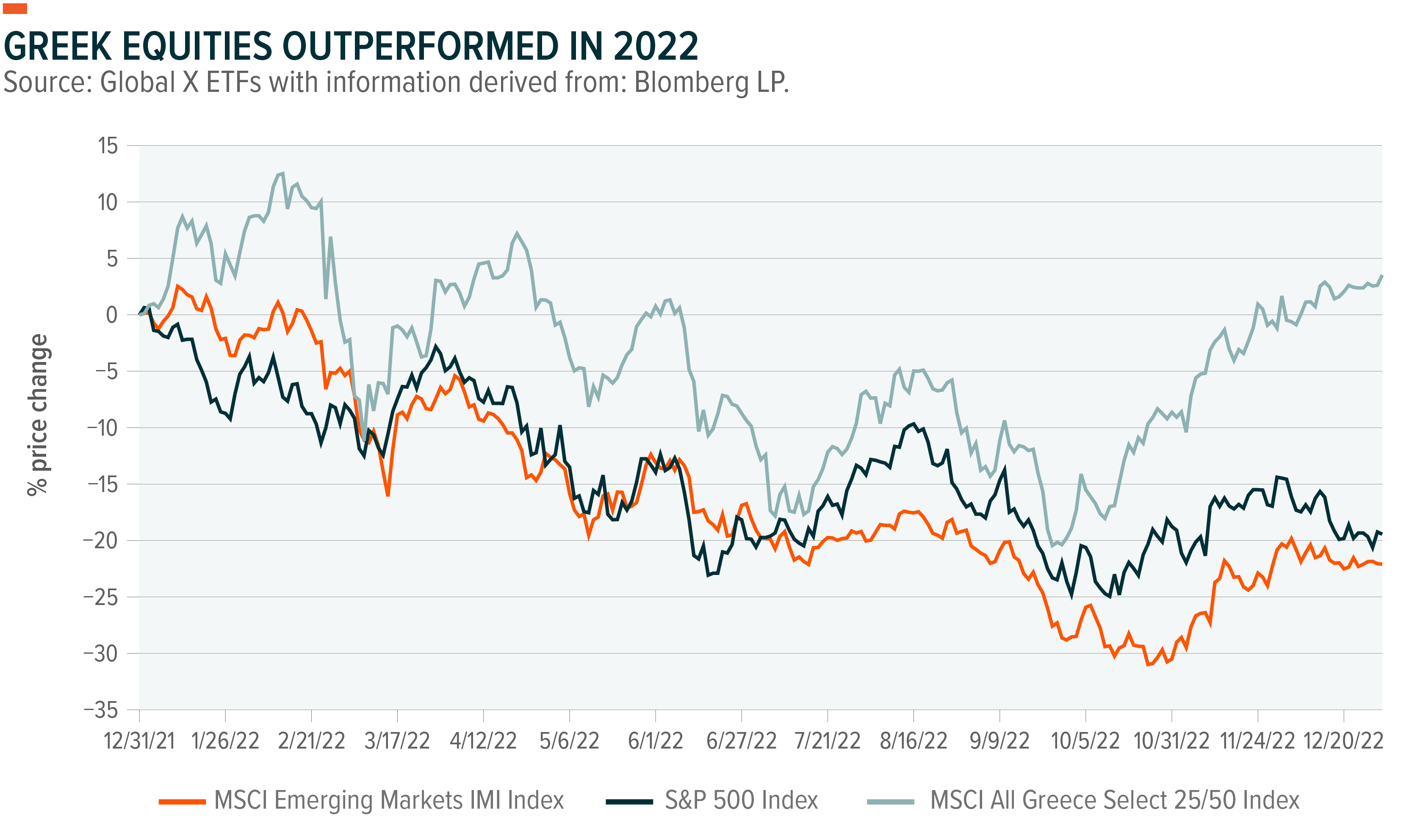

From Volatility to Outperformance in 2022

Once thought of as volatile, Greek equities showed resilience in a difficult 2022, with the MSCI All Greece Select 25/50 Index returning 3.53%, versus -19.81% for the MSCI Emerging Markets IMI Index, and an 18.13% loss for the S&P 500 Index.1

Past performance is not a guarantee of future results.

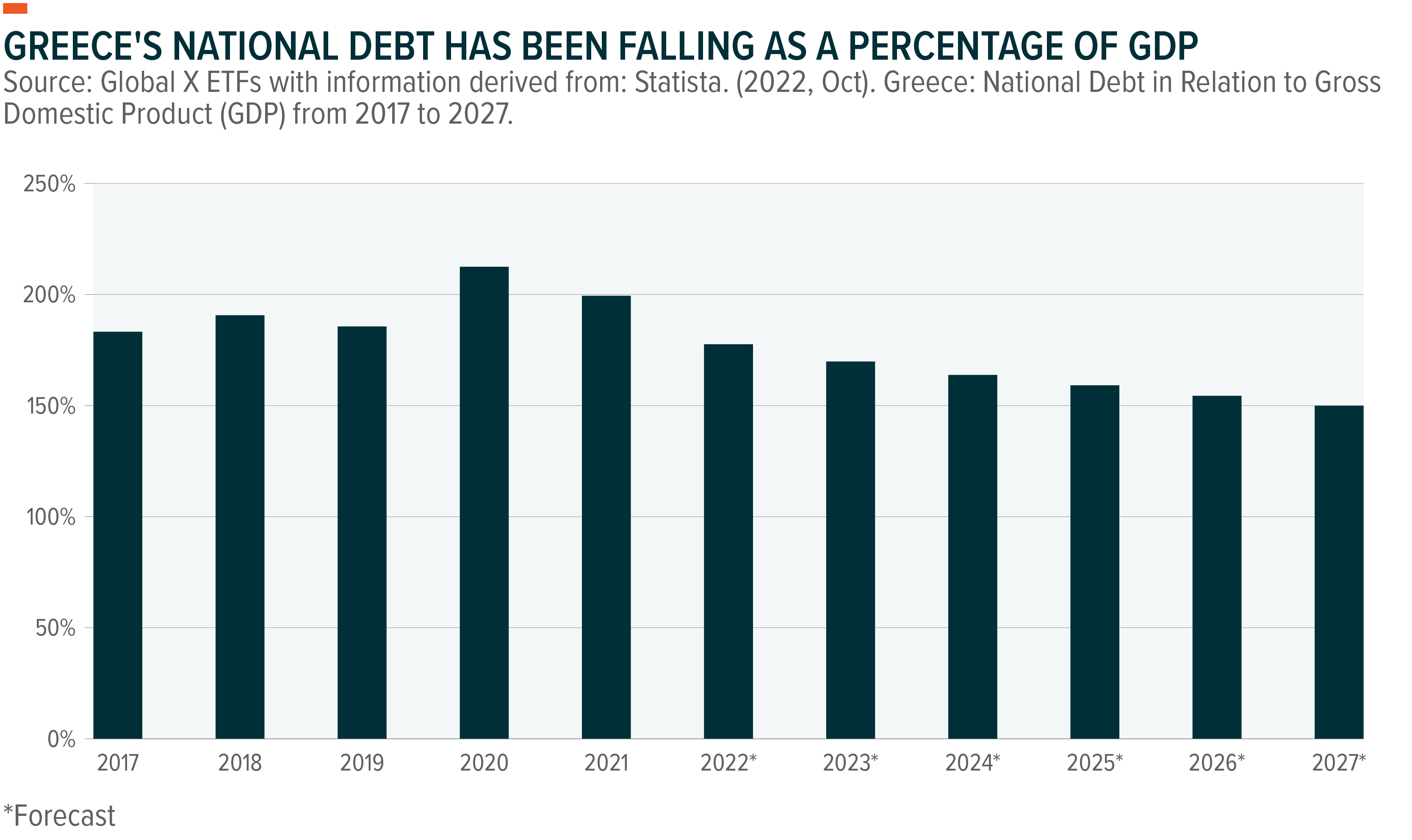

Gross domestic product (GDP) outperformed the eurozone average by over 300bps last year and is expected to continue growing faster than the group.2 Marginal GDP revisions have been positive, as well.3 Government officials highlighted that economic growth has consistently outperformed expectations over the last three years: unemployment has dropped to 12%, the lowest reading since 2010 and well below 2019 levels, and the country boasts perhaps the most aggressive fiscal consolidation since the pandemic among EU-27.4 Additionally, debt-to-GDP has been falling, approaching 170%.5 Looking forward, the combination of a recovering tourist sector, Recovery & Resilience Funds (RRFs), and the prospect of a market friendly election outcome all bode well for Greek asset prices.

A New Investment Cycle and Rebound in Tourism

While many countries need to tap the brakes on growth in the face of inflation, Greece is entering a capital expenditure (capex) cycle aided by 1. Years of underinvestment and 2. Recovery & Resilience Funds (RRF) seeping into the economy. RRF is the centerpiece of the EU’s recovery plan. It supports a way out of the COVID-19 crisis and aims at preparing Europe for digital and sustainable transitions. In order to receive financing, EU Member States have to prepare plans that set out the reforms and investments to be funded with the RRF. Such plans, called “national recovery and resilience plans,” have to be assessed by the European Commission and approved by the Council. Greece has been a first mover in this program and expects over EUR 30bln (roughly 15% of GDP) through 2025.6 Greece has already taken roughly EUR 10bln and the government has already approved over EUR 3bln in projects.7 The banks we met assured us that corporations across all sectors have been active applying for loans (part subsidized loans and part equity) to fund projects. Most of these projects are centered on digitization, energy efficiency, green energy transition, tourism, and exports. The bottom line is that while the rest of the world is seeing projects delayed because of higher interest rates and lower growth, Greece appears to be putting its foot on the gas.

Tourism represents roughly 20% of Greek GDP.8 Officials are expecting a return to 2019 levels this year, driven by a strong US dollar and significant pent-up demand coming from a re-opened China. We were in Athens mid-week off-season and saw at least seven daily flights from the US.

Politics

As mentioned, 2023 is an election year in Greece. The incumbent New Democracy (center right) will once again face the SYRIZA party (left), which could have dramatic implications for Greece’s market outlook. The first round of voting is set for May, and recent opinion polls show the incumbent, New Democracy, ahead by three or more percentage points, versus a previous six-seven point lead.9 At current levels, the party could lead through a coalition government, but if they extend the lead, they could form a government on their own. A coalition would most likely come with the PASOK party, which is center left (despite being the official socialist party). PASOK ruled before SYRIZA and does not carry a radical agenda. We expect New Democracy to present positive news in the coming weeks to boost polling numbers (possibly raising the minimum wage). Unemployment hovered around 20% under SYRIZA rule, meaning there is little positive memory or legacy drawing voters back .10 The incumbent party has not only reduced unemployment, but it has also increased the minimum wage by 20% since 2019.11 This resonates well with voters. A New Democracy victory and a continuation of its economic policies could be a key driver for a potential sovereign upgrade to Investment Grade.

Highlighting Some Potential Risks

On February 28th, Greece saw a head-on collision between two trains south of the Tempe Valley. The collision killed 57 people, many of which were students returning from Greek Orthodox Lent celebrations with their families.12 This was the deadliest rail disaster in Greek history and resulted from one of the trains being allowed to pass on the wrong track.13 Police clashes and protests followed the accident, as people saw it reflecting poor management from the current administration. We were privy to a strike in the center of Athens that started off peacefully and ended with Molotov Cocktails and gas masks. Though locals assured us that this is relatively normal for Greece, it portrayed a frustrated population that may be looking for change. However, polls showed the New Democracy maintaining a lead of three or more points (though down from a recent six-seven points).14 SYRIZA, their direct opposition, also lost about 1.5 percentage points in the last poll, showing an overall disapproval of the whole political system.15

Conclusion: An Overall Optimistic View on Greece

Despite the strikes and protests, we left Greece with a sense of optimism for its market. There is a transparent blueprint for potential asset appreciation based on both near-term structural drivers (a new capex cycle, a strong tourism season) and a roadmap of catalysts based on elections and a continuation of economic policy in the next four months; a potential sovereign upgrade before the end of 2023; and a possible reclassification from emerging to developed market within the next three years. Combining this top down, valuations look attractive, with the MSCI All Greece Select 25/50 Index recently trading at 6.61x forward earnings and 0.90x book value, versus 11.80x and 1.57x, respectively, for the MSCI Emerging Markets IMI Index16 Combined with strong bottom-up stories, we left with an optimistic near- and long-term view on the Greek market.

Related ETFs

GREK – Global X MSCI Greece ETF

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.