Malcolm Dorson

Malcolm Dorson Paul Dmitriev

Paul DmitrievWe continue to see India as the best structural growth opportunity in emerging markets (EM), if not the world. Our recent due diligence trip to Mumbai consisted of over 40 meetings with management teams, local investors, political experts, sector consultants, and economists. We worked closely with our affiliate, Mirae Asset’s, 14 person on-the-ground investment team and walked away enthusiastic on India’s near- and long-term investment prospects. As a sign of momentum, on the eve of our arrival in Mumbai, JPMorgan announced it would begin including India in its widely tracked JPMorgan Chase Government Bond Index – Emerging Markets from June 28, 2024, on. If the same move is replicated by FTSE and Bloomberg, we estimate that the potential U.S. dollar (USD) inflow to India could add up to USD 45bln over the next two years. This would likely support the currency, keep inflation in check, and provide additional liquidity to boost the ongoing capex cycle. To us, this is a clear signal that capital markets are deepening, investment will likely continue, wages are apt to grow, and consumption could increase exponentially. With over 15 years on the ground, we were also encouraged to see Mirae Asset and Global X’s brand maintain a leadership position in the Indian asset management landscape.

Key Takeaways

- Our recent trip to Mumbai, which consisted of over 40 meetings with management teams, local investors, political experts, sector consultants, and economists, left us with an optimistic view on India’s near- and long-term investment prospects.

- Attractive demographics, unique supply & demand dynamics, high barriers to entry, and a stable democracy are a few of the structural underpinnings that make India such an intriguing investment opportunity.

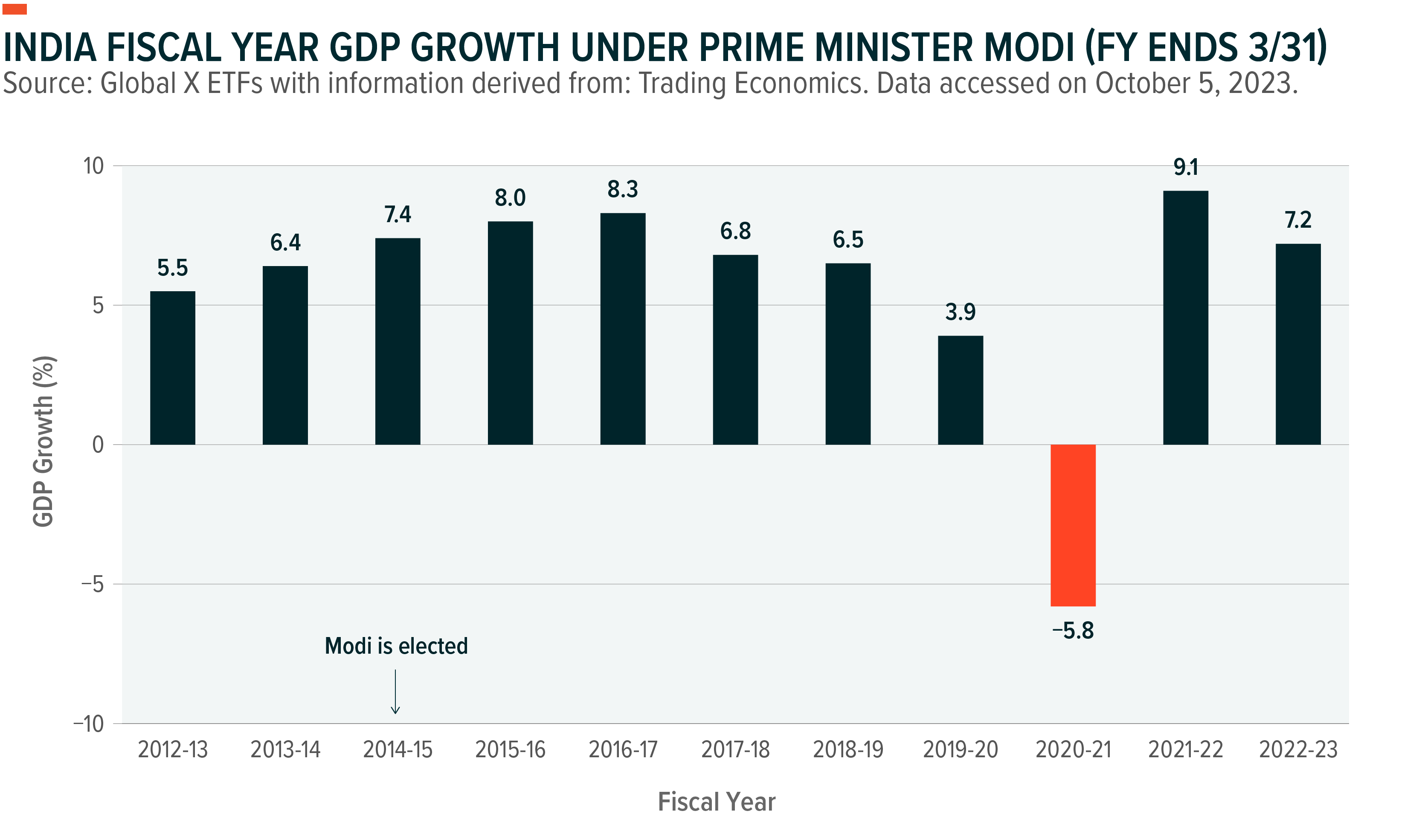

- In our view, Prime Minister Modi has delivered a number of tangible benefits for India. We would view a Modi victory in the April 2024 election, which appears likely, as a positive for markets.

A Structural Opportunity

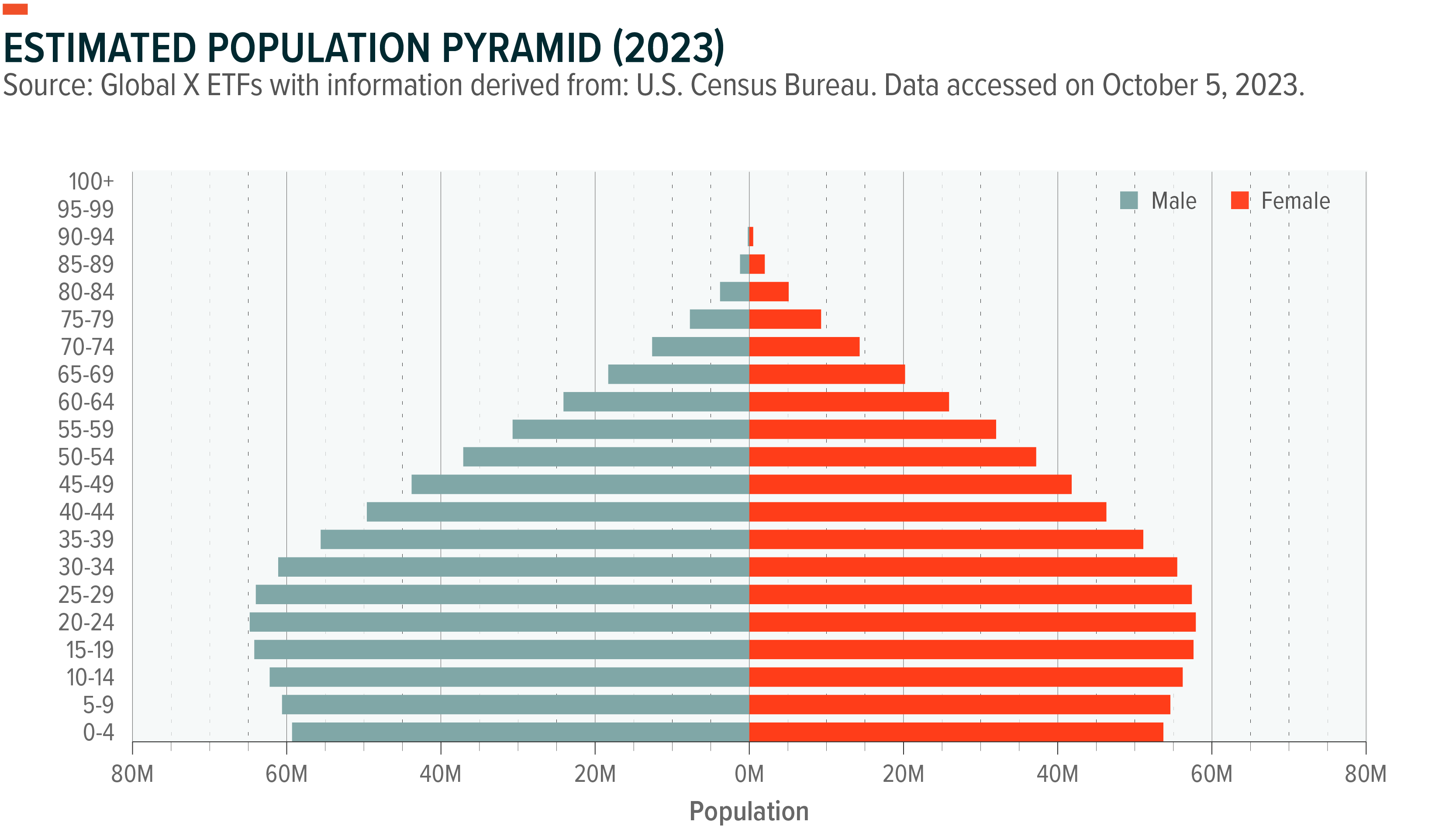

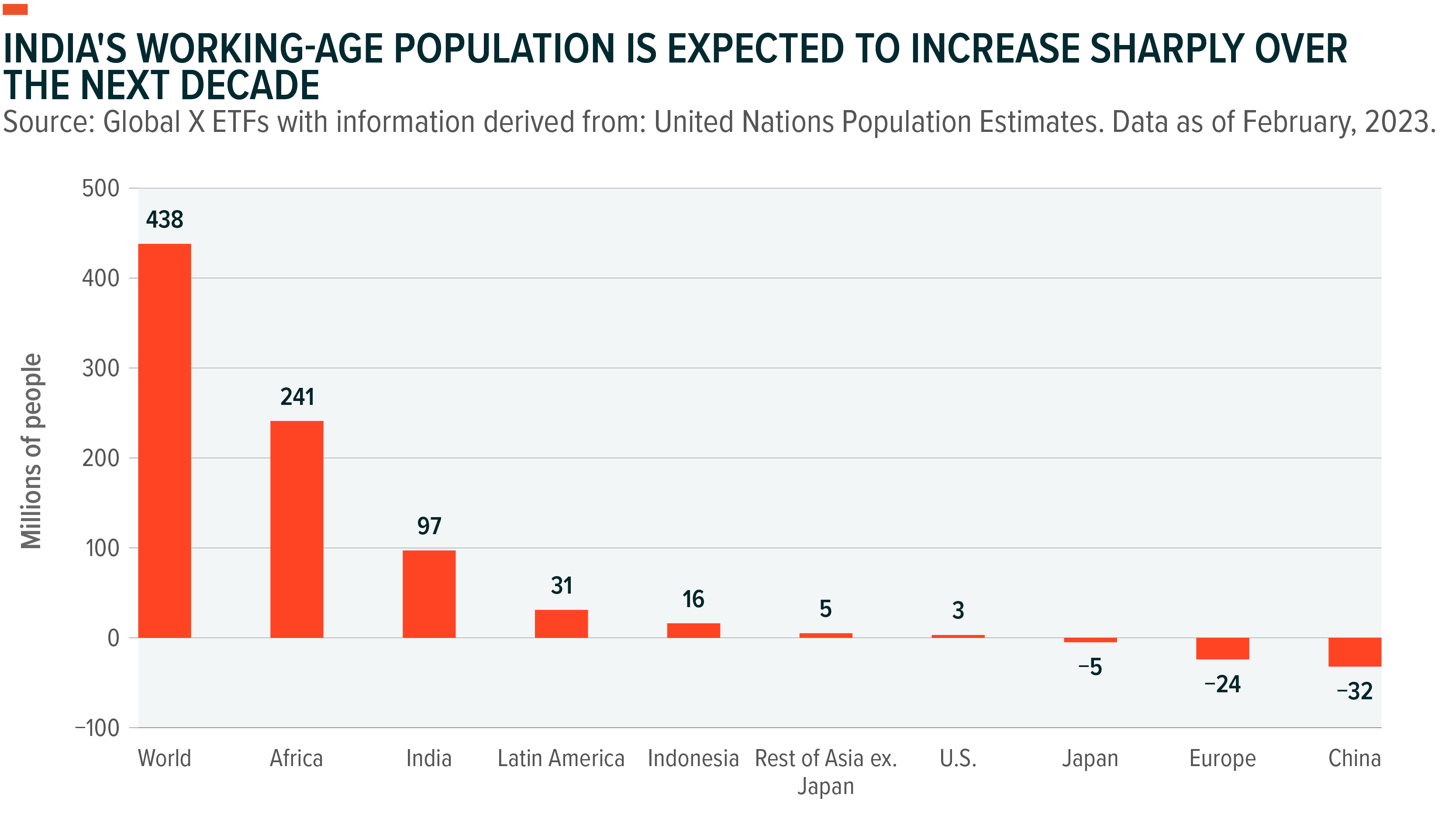

With a combination of attractive demographics, unique supply & demand dynamics, high barriers to entry, and a stable democracy, India appears well positioned to benefit from steady long-term tailwinds. Regarding demographic dividends, India has shifted into “position A”. Not only does India now boast the largest population in the world (surpassing China this year), but it also has the largest youth population in the world, with 65% of the population below 35 years old.1 This young population is broadly educated, with India’s youth literacy rate standing at roughly 90%.2 The country is expected to deliver the most university graduates in the world this year and also boasts the third largest group of scientists and technicians in the world.3 India is young, educated, and ready to deliver across services, manufacturing, and consumption.

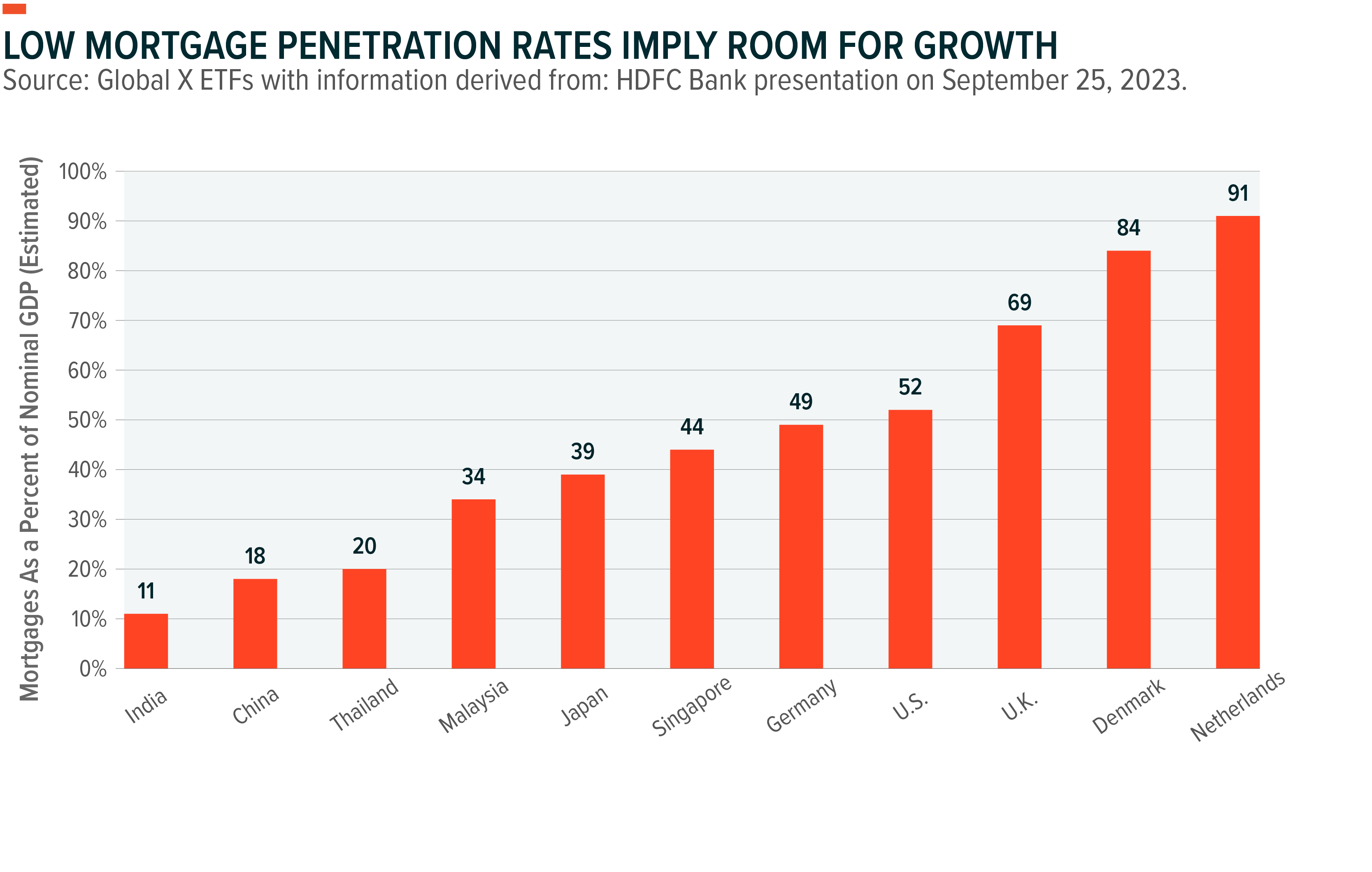

Equally important, we see the opportunity for India to solve the “mystery of capital”, which has historically plagued EM countries, by aiming to increase home ownership. The combination of low penetration rates (India’s mortgage to GDP rate stands at 11%), improving affordability, and recent government subsidies to boost home ownership, could lead to the growth of collateral, credit, investment, and consumption.4

All the above sets the stage for both growth and profitability. There are three structural reasons why India carries an elevated return profile, in our view. First, India’s market is heavily weighted towards consumption. Financials, Information Technology, Consumer Discretionary, and Healthcare combine to make up roughly 65% of the country’s market capitalization.5 Asset heavy, cyclical sectors such as Energy and Materials only account for roughly 20% of the market.6 Second, with 22 official languages (and home to 121 official and unofficial tongues), India is a challenging market to navigate. In addition to diverse cultures within the country, India is known for a significant amount of bureaucracy, high tariffs, and a national push for self-reliance. As a result, the Indian market boasts high barriers to entry, which means that market leaders often carry pricing power and other advantages versus their competition. Third, in various areas, we noticed that India has historically waited for a buildup of demand ahead of creating supply. Real estate is a good example. Most of India is privately owned. To develop projects, the government often must pay roughly 4x the market rate to purchase agricultural land. Thus, urbanization becomes a two-stage process. Step 1 is a migration of people and a buildup of informal housing. Step 2 is local politicians seeing a growing health problem and then creating housing. Putting demand ahead of supply increases capacity utilization rates, diminishes the need for leverage, and improves return profiles.

As investors, we are comforted not only by the above powerful tailwinds, but also by the fact that India relies on a democratically elected government. As Prime Minister Modi likes to say, India is the world’s largest democracy. While development across India has happened unevenly amongst the different states, which has raised political concerns, we believe that India will ultimately resist centralizing power like neighboring China and remain democratic, as it is likely the best way to maintain a unified India due to the massive diversity across languages, religions, and caste distinctions. Furthermore, current election polls suggest continuity, given the government’s progress and success with economic reforms and social welfare schemes.

The Digital Consumption Opportunity

Though Indian GDP continues to benefit from increasing manufacturing, exporting, government spending, and private investment, we are most encouraged by the long-term prospects of the country’s domestic consumption opportunity. Given the aforementioned fact that 65% of Indians are below 35 years old, we see a massive multi-decade window for companies to take advantage of hundreds of millions of people hitting their peak years of spending. Along with this “sweet spot,” digital connectivity is providing both a drive for social media-led aspirational spending and increased reach via e-commerce. This combination suggests that consumer companies could have a larger, wealthier, and more incentivized client base than they ever have before.

Consumer discretionary companies are likely to receive most of the benefits from the above. Per-capita GDP has already crossed the US$2,000 mark, which globally has historically translated into a dramatic pickup in consumer spending.7 We see discretionary income increasing at a compound annual growth rate (CAGR) over 6% for the next five years.

Every company we met mentioned India’s digital opportunity. Whether it was HDFC Bank touching upon the cost efficiencies of digital banking or Zomato speaking about the opportunities it sees in both advertising and e-commerce, this topic is at the forefront of every management team we spoke with in India. Digital banking is improving as companies can biometrically open new accounts, use video for know your client (KYC) processes, and cross sell products more efficiently than ever before. Outside of financials, we see direct to consumer (D2C) brands also disrupting the market. United Payments Interface (UPI), the national digital payment system, has facilitated digital transactions, Adhaar has allowed for unique customer identification, and the Goods and Services Tax (GST) has helped companies build credit profiles, lend to customers, and simplify cross-state shipping – allowing e-commerce competition to flourish across all income groups. We even came across ice cream companies that only exist on delivery apps. We were impressed to learn that e-commerce delivery drivers earn 15% above the national average, which is more than a first-year engineer in India.8,9 Despite the increased competition, we note that the big are getting bigger and see room for many players to flourish, given still low penetration rates and a rapidly growing market. Our meeting with a local beauty and personal care consultant (BPC) highlighted that digital-first brands are the fastest growing players in the Indian BPC market, growing at 2x the speed of their traditional peers. It is likely they will dominate half of the BPC market. In fact, Indian BPC companies are the fastest growing in the world, with a penetration rate of ~15%, which is nearly double e-commerce penetration in the country of 7-8%. This was according to a beauty and personal care consultant we met with from the advisory firm Redseer. We were also encouraged to hear from Redseer that at least 50% of gross merchandise value (GMV) growth was coming from tier 2 cities or lower, showing this is not just driven by the wealthiest tip of the population. Our meeting with Redseer also highlighted the online grocery industry, another interesting category that is forecast to reach a $930bn market by 2027, as online penetration looks set to grow from only 1% to 3%, implying a 36% CAGR over the next four years – more than doubling its revenues.

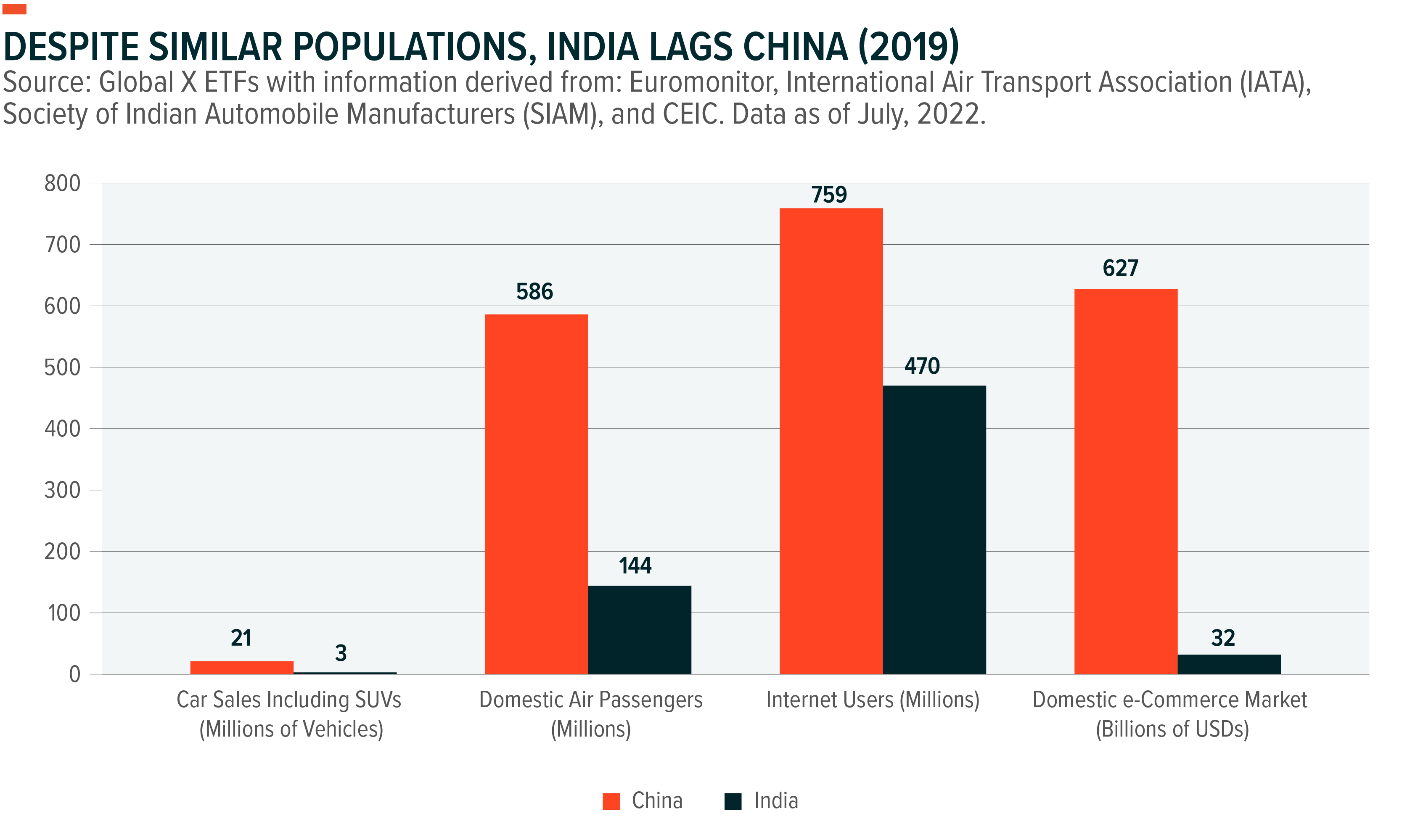

The China Alternative

More than 30 years ago, China’s and India’s economies were similar. Since then, China has grown significantly ahead of India, with the average citizen earning almost $13,000/yr compared to less than $2,500/yr in India.10 Now, as China’s growth slows, India is well positioned to pick up the mantle and continue driving emerging market growth while closing the income gap. In addition to GDP expectations moving up higher for longer, we see many reasons why India can become an investment alternative to China. First, India can probably still replicate China’s manufacturing driven growth model, given its economy is currently more than 50% service-based. We believe this is possible due to India’s status as a China+1 country, benefitting from re-shoring trends, improving know-how, international corporate support (e.g., Apple setting up new manufacturing facilities), manufacturing labor costs that are roughly 40% of China’s, and government driven programs based on production-linked incentive schemes.11 Second, education in India is materially improving. Literacy rates have climbed from ~20% after colonial rule towards 80%, and the country is now seeing more female than male enrollment in primary schools.12 The new National Education Policy (NEP) seeks to have 100% enrollment by 2030 and has a strong focus on Socially and Economically Disadvantaged Groups (SEDG).13 Furthermore, India has around 1.5mn engineering graduates every year and growing.14 Third, India, as a democratic country, has natural safeguards that prevent unfair practices and provide dispute resolution mechanisms. Fourth, India has recently surpassed China in terms of population and is still set to benefit from a demographic dividend, while China must find a way to support a rapidly aging and declining population. Ultimately, while the two countries do compete, it’s important to note that this is not a zero-sum game. India is driving growth across all GDP variables, but with significant momentum in manufacturing and infrastructure, while China’s economy is pivoting towards services and consumption.15

Political Momentum

India’s next election will come in April of 2024, and we see the potential re-election of Prime Minister Modi as a key driver of momentum into the new year. Modi has been in power since 2014 and continues to poll strongly.16 In addition, on the ground, we saw Modi in full campaign mode with the Prime Minister’s face on every other billboard or truck. We see his re-election as likely given the tangible improvements he has delivered for the country – including, but not limited to:

- Increasing Access to Education: The country has seen a spike in universities during the Modi Administration, from 723 in 2014 to 1,113 today.17

- Emphasizing Female Empowerment: In addition to other measures during his nine-year term, India took a major step forward for gender equality this September, when Modi announced a bill that would reserve one-third of seats in the more powerful lower house and state legislative assemblies for women.18

- Improving the Healthcare System: Increasing healthcare coverage, introducing a digital health ecosystem, and building new medical colleges and hospitals.19

- Driving a Digital Revolution: Modi has driven a remarkable transformation for the country with rapid strides made in bringing internet connectivity to the remotest corners of the country, helping ensure that the benefits of the digital revolution reach every citizen.20 His government’s Unified Payment Interface (UPI) is seen as a revolutionary leader in digitalizing a major global economy, reducing fraud, cutting inefficiencies, and driving a broader base of people into the financial system.21

- Improving Infrastructure: In the last nine years, urban mobility projects have reached 20 cities. In addition, we’ve seen 74 new airports come online. Further, 111 waterways were declared as National Waterways.22

- Making Indians Wealthier: Income per capita in India has doubled from INR 86.65 in 2015 to 170.62 in 2023.23

Conclusion

We believe that India presents an oasis for investors, driven by growth, profitability, and governance. Regarding growth, we believe that the country’s political incentives, demographic dividends, and beneficiary status of supply chain diversification could lead to consistent 6%+ GDP growth prospects over the next several years. When speaking of profitability, the Indian market’s weights towards asset-light sectors, in addition to the economy’s significant barriers to entry, could translate into elevated return-on-equity profiles. Last, in terms of broad governance, though India shares some of China’s massive structural opportunities, it also boasts the world’s largest democratic system, which we see as a key differentiator to key-man communist rule.