Paul Dmitriev

Paul DmitrievOur team’s “Views From the Ground” series continues with our recent visit to the Middle East & North Africa (MENA) region, where we met with 15 corporates (including several of our holdings) from Turkey, India, Saudi Arabia, Abu Dhabi, and Dubai; local capital market authorities; analysts; and economists. We also took a real estate tour to see developments in Dubai with our own eyes and tested several local quick serve restaurant (QSR) brands for delivery and quality.

Key Takeaways

- The MENA region is often overlooked by investors, but we see numerous avenues for potential structural growth.

- A regional transformation is underway, as countries look to diversify their economies beyond oil and gas and enact business-friendly structural reforms.

- In addition to the region’s favorable growth prospects and economic stability, we believe that equity market valuations are attractive.

“If a tree falls in a forest and no one is around to hear it, does it make a sound?”: A Secular Growth Story if You Are Listening

We are not the first to compare the growth of an overlooked and nascent market to this common philosophical question, but we are pounding the drums over the structural growth that we see ahead in the MENA region at roughly 4% ex-oil gross domestic product (GDP) growth, and we hope that others are also listening!1 The market has grown to nearly 7.5% of the MSCI Emerging Markets Index and 34% of the MSCI Emerging Markets ex-Asia Index, and one analyst we spoke with sees positive drivers creating the potential for another $10bn in passive flows that could drive the region to represent more than 10% of MSCI EM, which would overtake Latin America (LatAm) as a region.2

However, the average active global emerging markets (GEM) fund manager is over 50% underweight the MENA region relative to the benchmark, according to an analyst we met with. Moreover, we were told that it’s estimated that the average active GEM fund owns ~3.6x more LatAm than MENA, despite expected GDP growth in the MENA region of ~4.2% versus only ~2.5% for LatAm by 2025!3 This means that most are missing the regional transformation that is underway, which includes:

- An Under-Owned Region: MENA’s weight in the MSCI Emerging Markets Index stands at ~7.5%, compared to MENA equities’ allocation in active GEM funds at only ~2.9% (based on the top 200 funds as of January 24, 2024), pointing to a material underweight position relative to the benchmark.4,5

- MENA is Overdelivering: The International Monetary Fund (IMF) projects 2.9% and 4.2% GDP growth for the MENA region in 2024 and 2025, compared to 1.9% and 2.5% for LatAm.6 Comparing the largest country in each region, the difference is even starker, as Saudi Arabia is forecast to grow 2.7% and 5.5% in 2024 and 2025, compared to 1.7% and 1.9% for Brazil.7

- Potential to Reach 10% of MSCI EM: The region is bustling with equity capital markets activity. There have been over 114 deals announced over the last 12 months in the MENA region worth over $11bn, and we see clear appetite for more.8 Our meeting with the Tadawul Group (Saudi Exchange) confirmed a pipeline of at least 56 IPOs in Saudi Arabia alone for 2024 and over 100 for the medium term, while meetings with several companies related to energy giant ADNOC corroborated a desire to increase free-floats above 10% eventually in order to be considered for MSCI inclusion.9 Saudi Aramco is also considering another 10-20% secondary placement from the Kingdom’s Public Investment Fund (PIF).10 The Dubai Supervisory Committee also wants to see an increase in total volume and listings on the Dubai stock exchange. Regulatory reforms, such as potential foreign ownership limit changes in Saudi Arabia, similar to what already occurred in Qatar and the UAE, could also drive additional passive flows to the market.

- A China Alternative and an India Connection: The MENA region sits between the East and West, and many countries are trying to position themselves as another China alternative in the region. In our view, the growth of the India-MENA connection has been underappreciated, as trade between the two has gradually moved from one primarily based on oil in exchange for food towards an exchange of high-skill manufacturing, with India selling pharmaceuticals, electric vehicles, and metals to the MENA region in exchange for aeronautical products, plastics, and chemicals. Bilateral non-oil trade with the UAE was up around 6% in the first 12 months since the signing of the Comprehensive Economic Partnership Agreement with India, as it reached $50.5bn, with a target of $100bn in trade by 2030.11 India and MENA share both a long history and similar values, and given the India-China rivalry, India has avoided Chinese foreign direct investment (FDI), which has opened the door for countries in the MENA region to step in.

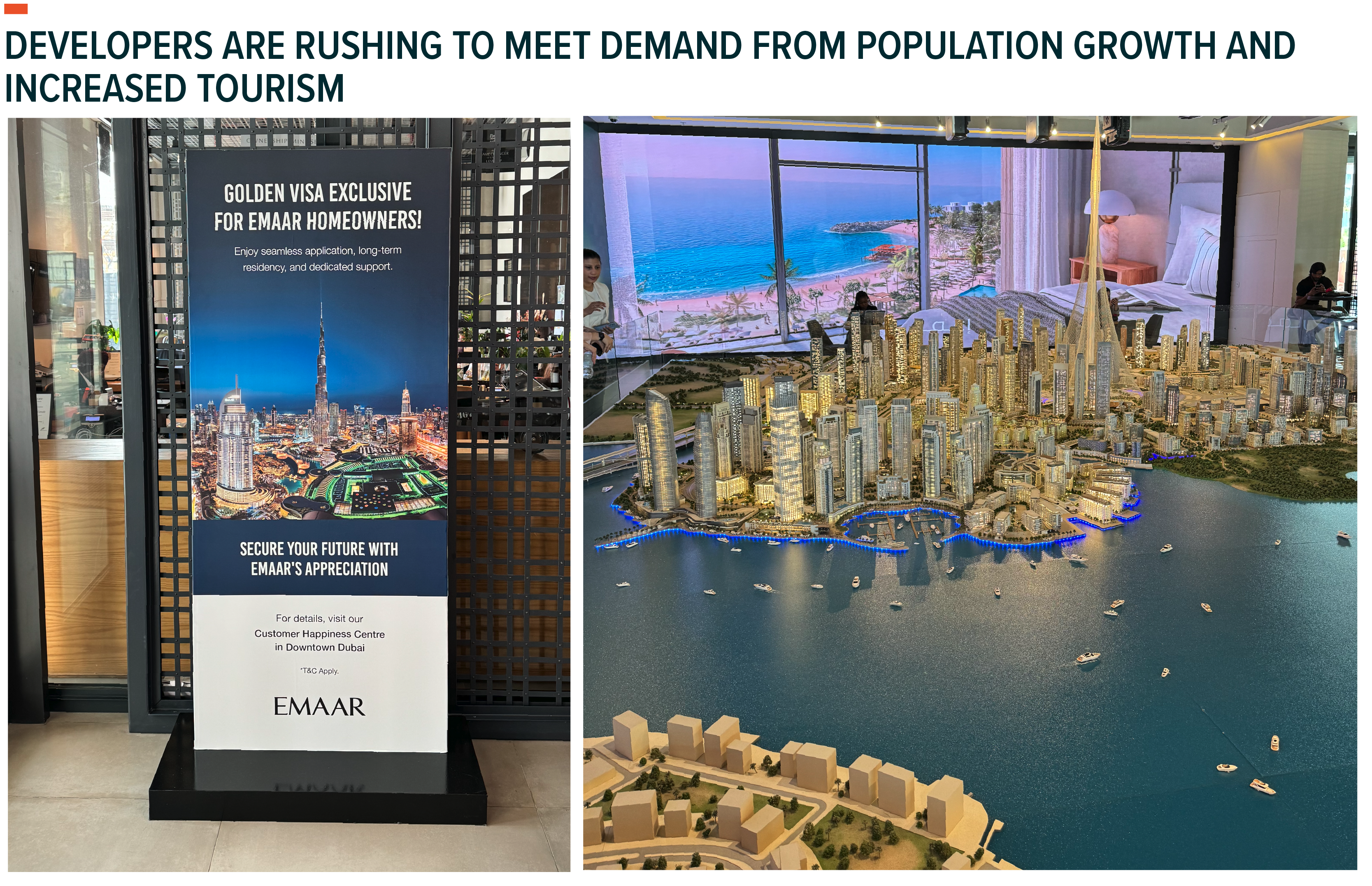

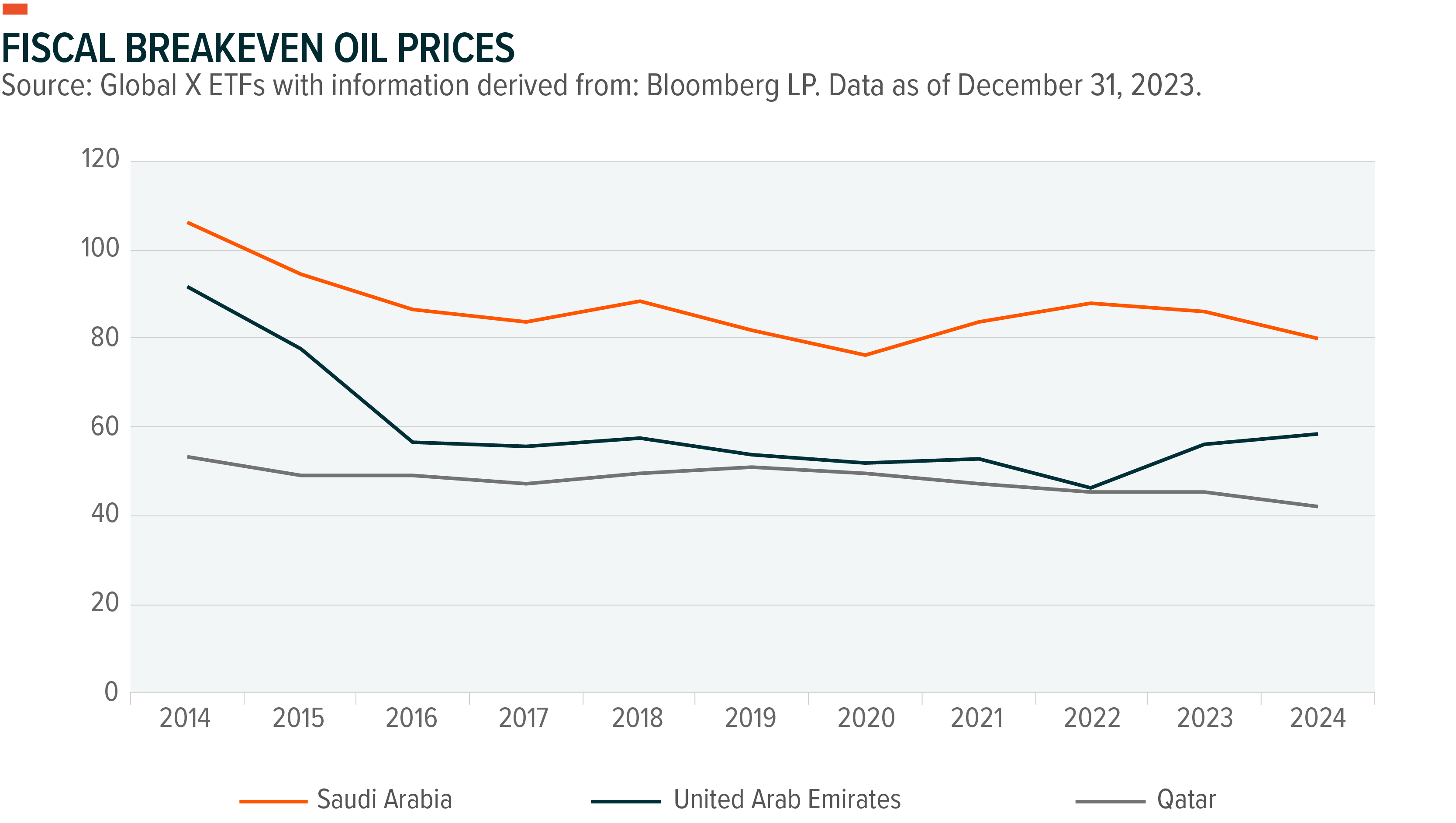

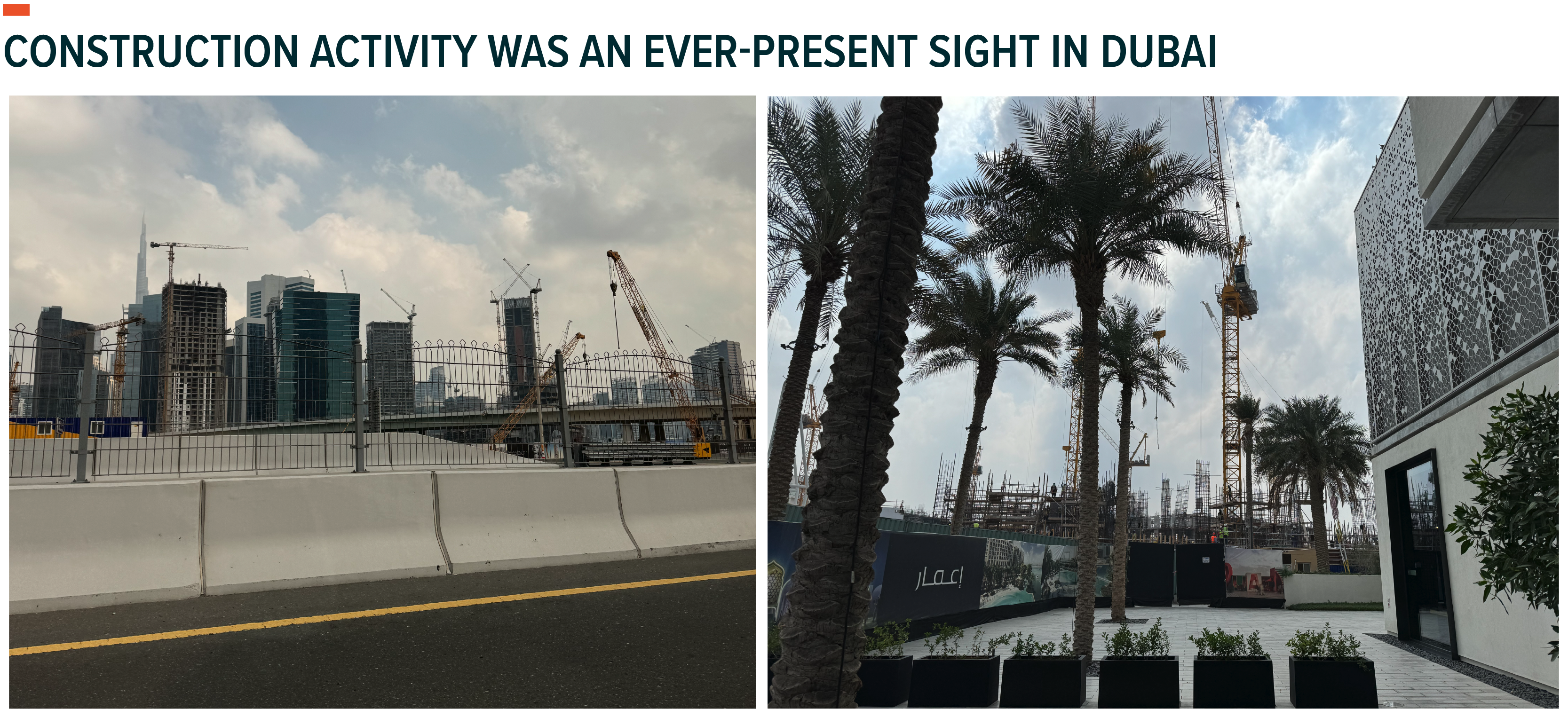

- More Than an Oil Play: Since the oil price plunge in 2014-16, Gulf Cooperation Council (GCC) countries have looked to accelerate their economic diversification and decrease their reliance on oil-related revenues. In 2016, all GCC countries pledged to introduce a common VAT rate, but the tax environment remains favorable. Corporate income tax rates are still well below average OECD (Organization for Economic Co-operation and Development) levels, many industries still have exemptions, and personal income taxes are still not in place. Spending on “Giga” projects will be largely handled by the sovereign wealth fund PIF Saudi Arabia and will make up a large part of public capex spending, but not a part of the Kingdom’s budget. Although recent events like the Covid-19 pandemic and short-term increases in spending on public projects have impacted fiscal breakeven oil prices in the near term, we sense a strong desire to continue diversifying MENA economies from their reliance on oil prices to support fiscal needs and expect OPEC+ to keep an eye on oil market tightness, prices, and budget needs. The region is also seeing transformational infrastructure and housing growth as the population booms. In fact, it was harder to find parts of Dubai that didn’t have any construction cranes than those that did! In some cases, reforms like golden visas (long-term residence visas for foreigners) have helped expedite growth further, and it was not uncommon to see queues at sales offices for new properties.

- Racing Towards Reforms: In 2010, the UAE launched Vision 2021, focusing on economic diversification and sustainable development, which was followed by the country’s “Next 50” strategy, which was launched in 2020. Meanwhile, Saudi Arabia launched its Vision 2030 strategy in 2016. These broad reform strategies touch upon key areas, including economic diversification (e.g., developing non-oil sectors and FDI); fiscal sustainability (reducing government spending, improving financial management); human capital development (education and training, “Saudization” of workforces, empowering women via participation in the work force and leadership roles, golden visas, etc.); social reforms; and governance reforms at the corporate level. We are also encouraged by the aforementioned potential for changes in foreign ownership limits in Saudi Arabia. Finally, we continue to hear the positive benefits from the move towards a Monday-Friday work week in the UAE and believe Saudi Arabia may look to eventually follow. This seemingly minor change could bring big benefits as trading volumes are ~20% lower on Sundays versus Monday-Thursday (~$1.9bn average daily trading volume versus ~$2.4bn), which could help bring more trading, liquidity, and a further deepening of these still retail dominated markets.12

- Stability and U.S. Dollar (USD) Peg: Most countries in the region maintain some form of a USD peg (Kuwait is pegged to a basket of currencies), which began in the 1970-80s to provide predictability for trade, investment, and to help manage oil revenues. A secondary benefit has been a historically low inflation environment.

We continue to see the MENA region as an attractive long-term investment opportunity. Not only do we anticipate GDP growth to remain above the developed market average, supported by long-term structural reforms, but we see potential catalysts for passive flows into the market, as well. Equity capital market activity will likely remain elevated. A weighted average return of +86% and +35% from IPOs in the last twelve months in Saudi Arabia and the UAE, as well as Modern Mill’s recent IPO being 127x covered, create a paradox of opportunity for us, as the region remains massively under-owned versus the benchmark.13 Furthermore, the region still trades at attractive valuations, with the MSCI Saudi Arabia Index, MSCI UAE Index, and MSCI Qatar Index trading at 6.0%, 17.4%, and 23.9% discounts to their five-year historical price-to-earnings averages, respectively.14

Company Spotlights

- Americana: Americana Restaurants is the largest QSR and OOHD (out of home dining) restaurant operator in the MENA region. We believe it offers a combination of fast growth, improving profitability, strong cash generation, and a return on equity (ROE) that is ahead of international peers (above 60%).15 Management’s focus is on growing its core “Power Brands” and plans +200 store openings per year to increase penetration of global brands, launch new brands, and enter new segments, with mid-single digit like-for-like growth expected. Structurally, the company is exposed to positive tailwinds from a growing and tech-savvy population that has a growing preference for international brands and is increasing its frequency of OOHD and food delivery. We also believe there is an opportunity for further growth in segments Americana does not operate in (e.g., sandwiches and salads).

- ADNOC Drilling: ADNOC Drilling is a unique and leading drilling services operator in the MENA region (and sole operator in Abu Dhabi) that has offered consistent 5% dividend growth on a dividend-per-share basis, while also offering growth potential, driven by the UAE’s desire to increase oil production capacity from 4.5 to 5mboe/day.16,17 The company has a rapidly growing oil field services business and is just beginning to expand into adjacent markets. ADNOC has 15-year contracts with minimum guaranteed internal rates of return (IRRs) of 10-13% regardless of inflation or market volatility, so it does not need to take price risk like some of its regional peers.18 Furthermore, the company has a young asset base with long-dated and predictable cash flows.

- Jahez: Jahez is a unique regional play on food delivery in the MENA region, with a focus on Saudi Arabia (KSA). Unlike peers in other countries, Jahez is already profitable despite being the number two player (after Delivery Hero). Furthermore, its position in KSA benefits it, as food delivery penetration is only about half that (~18%) of nearby GCC countries, as well as the U.S./U.K. (~30%), despite higher mobile phone penetration.19 The young, mobile savvy population is also undergoing tremendous social change, which includes more women joining the labor force. These changes are impacting how people consume food within the Kingdom, in addition to the typical tailwinds seen in other markets on the back of the Covid-19 pandemic (i.e., move to online, e-commerce, etc.). We also think Jahez has room to increase take rates, as the company is charging lower rates versus peers in the country. Management plans to continue growing domestically by expanding into additional regions, while medium-term growth will likely come from regional expansion in the GCC.

- Al Rajhi: KSA-based Al Rajhi is the number one Islamic bank in the world, commanding approximately 15% domestic market share in assets, 18% in deposits, 40-50% in consumer segments, and 30% in mortgages.20 It also has the largest domestic network of around 500 branches, over 4,600 ATMs, and over 550,000 points of sale.21 The bank is fully Shariah compliant, which provides a very strong brand due to its customers’ cultural attitudes. It also has a low cost of funding (>90% of its deposits are zero priced and it has no wholesale debt) which, along with its public sector relationships and extensive network throughout Saudi Arabia, provides a structural advantage.22 Over 70% of its loan book is retail, and that segment does not generally come with high risk, given the salary account backing.23 At 64% credit penetration, KSA is one of the more underbanked economies entering EM, suggesting a potentially long runway for growth.24,25

Conclusion

Overall, we left the Middle East with strong conviction about the region’s growth prospects. Signs of growth and development were ubiquitous on our trip, and we are optimistic about the impact structural changes will have as these countries look beyond the energy sector for economic growth. When combined with attractive equity valuations and investors’ underweight positions, we think there is an exciting opportunity for investors in the region.